Bearish short-term views on base metals and RMB stay intact

Xi’s economics team recently emphasised the “accelerating the construction of a modern industrial system” and “supporting Chinese-style modernization with high-quality population development”. These are clearly longer-term objectives, but they are still relevant to short-term sentiment as China gets back to work after the May 1 holiday. So far, William Hess’s short-term views on base metals and the currency from recent pieces remain intact. He notes that onshore positioning in copper, for example, has turned decisively in this direction after the Politburo Q1 meeting. The latest update to his cyclical indicator for China continues to show a loss of recovery momentum.

Colombia: Brace for a credit rating cut

Marcos Alberdi retains his pessimistic scenario of a scant 0.6% real GDP expansion in 2023. High core inflation coupled with sticky inflation expectations saw the central bank tighten the policy rate by 25bp, and Marcos expects them to be the last LatAm inflation targeter to start easing rates. In his latest report, he discusses estimates for the future trajectory of Colombia’s credit rating, given the current deterioration of the country’s institutional foundations. Even under relatively benign assumptions on the trajectory of macroeconomic aggregates, Marcos sees an inevitable credit downgrade.

Israel: Next political crisis will arrive at the end of May

Netanyahu is locked in a three-front battle with the opposition, his own coalition, and his corruption trial, and none will end soon. After a month-long parliamentary break, hundreds of thousands of Israelis continue to take to the streets regularly to rally for and against Netanyahu. While his efforts to give parliament a stronger voice on judicial appointments have lost some of the urgency they had in March, his coalition’s popularity is plummeting, and it is growing more restless with his leadership. Because Israel’s political chasm is so deep, it is increasingly hard to imagine when stability will return to Israeli politics, and hard to imagine it will occur under Netanyahu’s leadership.

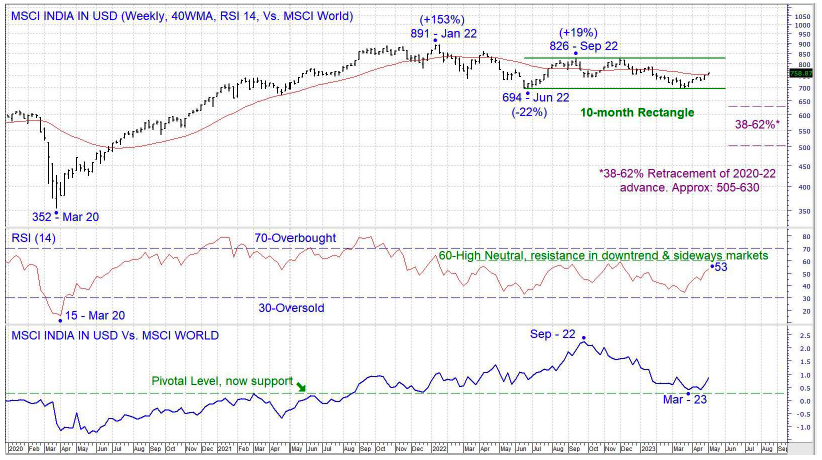

Will investors return to India soon?

The MSCI India in USD has been rangebound for 10 months, following a very shallow retracement of the 2020-22 bull market. The shallow correction, combined with the relative performance vs the MSCI World, show what an investor favourite this market was post the Covid-19 bear market lows. An upside breakout from the 10-month range would likely trigger investment flows from global investors again.

Thailand’s elections

Thailand heads to the polls on May 14 against a mixed economic backdrop. The return of tourism has strengthened the currency and bolstered consumption and services, but weakening global demand is starting to hurt the export sector. The populist Pheu Thai party looks set to win the popular vote decisively. The military’s preferred candidate is likely to emerge as prime minister, maintaining political continuity. Niall Ferguson believes monetary and fiscal easing is coming, supported by normalisation in tourist arrivals from China, and is therefore OVERWEIGHT Thai assets against EM peers.

Asian insider trading in April

Smart Insider’s monthly report covers insider trading activity in 13 Asian countries and corporate buyback activity in 12 Asian countries. In their latest report, insider trading evaporated in April in India, which isn’t unusual due to trading restrictions. Based on March’s ratio (Sell/Buy Ratio 1.54), sentiment is bullish with 8 positive ranks and 3 negative ranks. Thailand saw insider sentiment improve again, and sentiment is bullish with 7 positive ranks and 0 negative ranks. China’s insider buying remained flat vs. March, and sentiment is neutral (S/B Ratio 2.63 vs 5.63 in March). Light buying and average selling in Malaysia has led insider sentiment to deteriorate from Bullish to Neutral.