Company & Sector Research

Europe

Vision Research

European & US short ideas

Since Vision pitched their short thesis on Vidrala, Verallia and O-I Glass at our Equity Shorting Conference in mid-Mar the stocks have underperformed the Stoxx600 by ~8%. In the last couple of months they have also initiated 3 new European shorts, 3 new US shorts, and has readied a new $7bn+ European short (trades ~$20m/day and has short interest of <1%) for initiation next week. Please join Vision for a meeting while members of their team are in Paris (Jun 5th-6th), Zurich (Jun 7th) and London (Jun 8th-12th).

In the last 24 months, Vision has closed several shorts including: Allegro, AutoStore, Boohoo, Burlington, Colruyt, De'Longhi, Electrolux, Gerresheimer, H&M, Hargreaves Lansdown, Inditex, New Relic, Nokian Tyres, Peloton, Similarweb, Thule, Trex, TSMC, UiPath and Whirlpool.

Iron Blue Financials

An Iron Blue score of 31/60 (+1 Y/Y) is top quartile (fertile ground for shorting). Red flags include: 1) High and expanding levels of stripped out restructuring, share based payment, legal and other one-off costs. 2) Increased gap between headline net debt and Iron Blue’s preferred calculation. 3) A rising interest burden with expensive debt replacing cheap debt. 4) Increased legal liabilities. 5) Sub-optimal governance, including a non-independent board and unusual executive remuneration incentives. 6) Additional risks from inflation, litigation, interest rates and Ukraine.

the IDEA!

High inflation is leading to downtrading, both reflecting in consumers buying cheaper products and turning to cheaper supermarkets. AD has been a beneficiary. In Europe, its private label products account for over 50% of sales. With its ‘Price Favourites’ and other innovations (multi-channel strategy, personalised offers for loyalty programme users, etc.), its Dutch subsidiary Albert Heijn has hit the bull’s eye in its attempt to keep its customers coming to its stores. This strategy is increasingly being rolled out into other countries as well. This is one of the main reasons why the IDEA! has maintained their positive stance on AD despite reservations towards other consumer sensitive stocks.

ResearchGreece

ResearchGreece raises their 2023/2024/2025 net income estimates by +35%/+15%/+26% on lower deposit costs, higher income from securities and higher ECB deposit rates. They expect the bank to raise its 2023 RoTE guidance closer to their 13.5% estimate. It will be interesting to see if management changes its 2025 RoTE guidance as well (now at >12%). ResearchGreece’s RoTE 2025 stands at 11% as they assume ECB rates go down by 50bps within 2025, impacting loan rates and Eurosystem income. Their TP increases from €5.76 to €7.25.

Shephard Media

Defence Insight: European security of supply

War in Ukraine has provided Europe, specifically the EU, with a much-needed reality check and opportunity to reform how it handles defence, starting with cooperation. While one of its weaknesses is integrating a group of 27 individual member-states into a coherent entity, it also represents a strength that it should capitalise on. This should start with further integration of Nordic states into EU projects to pool greater resources together and help improve supply chain resilience. However, to do this, the EU must do better - moving away from solely financial-based incentives and enhancing the value of its initiatives to enhancing the value of its initiatives to member states and other partners.

North America

Trivariate Research

Where should a CIO hunt for alpha?

Having previously written about areas where quants fail and fundamental investors should focus their efforts, Trivariate's latest report examines alpha-generative resources using other metrics, including evaluating the level and changes of company-specific risk, valuation dispersion, pairwise correlation, and opportunity set for each sub-industry in the market. Their report concludes with a useful summary table which ranks the 24 industry groups 1 through 24 on each metric. 1) Food, Beverage & Tobacco, 2) Discretionary Distrib. & Retail, 3) Pharma, Biotech & Life Sciences, and 4) Capital Goods are currently of most interest for alpha generation. Energy and REITs are more “group calls”.

Boyar Research

The shares have faced pressure as investors have been focused on slowing broadband net additions, which were strong during Covid as demand was pulled forward. However, at current levels, investors are acquiring a top-notch cable business at a heavily discounted valuation and are receiving an extra ~$25 a share in additional value, representing the company’s NBCU and Sky businesses, for free. CMCSA has recently reached its targeted leverage levels (net debt/EBITDA) of ~2.3x and Jonathan Boyar expects returns to shareholders to continue to be robust (2022 saw a record amount of capital returned to shareholders; dividend increased for 15 straight years). 100%+ upside.

Gordon Haskett Research Advisors

Robert Mollins upgrades the stock to Buy - key factors behind his bullish stance include: 1) Investor uncertainty surrounding the tech stack migration is overblown. 2) EXPE will more than offset a slowdown in vacation rentals through its traditional lodging offerings. 3) The upcoming launch of “One Key” will drive share gains in the US in the near-term and internationally over coming years. 4) EXPE's valuation discount is overdone with the company expected to see fundamentals that are relatively in line with online travel peers. Robert’s $130 TP equates to 6.5x his 2024E adjusted EBITDA.

Two Rivers Analytics

This furniture manufacturer faces weakening end markets, high debt levels (post Knoll acquisition) and excess inventory. Price increases have masked declining volumes. MLKN’s sales have fallen ~40% in past downturns, yet current forecasts expect a mere 12% peak to trough drop. Eric Fernandez believes a min. 25% decline is more realistic. Furthermore, the secular trends working against office leasing will dampen a sales recovery. Eric expects EBITDA margins to also come under pressure (fell from 15% to 9% in both previous downturns). However, the financial leverage today is much worse than before. That will have a disproportion impact on EPS and net cash flows after interest.

Verbatim Advisory Group

Verbatim's latest channel survey reveals weaker same-store sales trends at Taco Bell in Apr (vs. both Mar and 1Q23 trends) despite promotional menu options. The current Y/Y comparison is harder than the previous quarter on a Y/Y basis and on a multi-year basis. In Q1, Verbatim applied a bias factor of positive 200bps. Due to the tougher multi-year comparison and weaker trends, they are applying a bias of positive 200bps in Apr as well. With an Apr Raw Comp of +3%, their Apr Comp Estimate is +5% (vs. 1Q23 Actual Comp of +8%). Click here for the full report.

Off Wall Street

CNMD is an undersized, competitively disadvantaged seller of commodity general surgery and orthopaedic capital equipment and consumables. OWS previously recommended shorting the stock when it was trading at $135 (Jan 22). They subsequently closed their position (Sep 22) locking in a 30%+ gain. However, the stock has since rallied to over $120 with no clear fundamental driver. CNMD has tried to acquire higher-growth, higher-margin products to transform its business, but this strategy has yet to demonstrate any success. Capacity for further M&A is limited with leverage at ~5.3x. TP of $80, represents ~2.8x their 2024 sales forecast and ~23x their 2024 EPS estimate.

Insight Investment Research

Robert Crimes initiates coverage with a Buy rating and TP of $384 (100% upside) - this follows Insight’s recent work on CN Rail (TP C$341, +120%) and CPKC (TP C$218, +108%). Railroads is now their preferred Infrastructure sub-sector, which is set to benefit from the “New Golden Age of Rail” driven by favourable environmental credentials and increasing cost advantage vs. road. While UNP has underperformed its peers regarding network fluidity, volumes, EBITDA growth and safety, Robert expects its new CEO to improve performance.

As infrastructure specialists, Insight focuses on lifetime free cash flows with detailed DCFs / DDMs and IRR-Ke valuations. Their CN Rail initiation report from earlier this year provides a useful example of a 'typical' Insight report and can be accessed by clicking here.

ERA Research

IFP has the lowest exposure to BC (with its high log costs and exceptionally weak S-P-F prices) of the publicly traded Canadian producers, while 45% of its capacity is in the US south where sawmilling margins will remain healthy courtesy of outperforming SYP prices and consistently low log costs. IFP’s Q1 earnings outperformed peers and ERA expects this to repeat in Q2. As such, they are recommending a short-term trade (TP c.$30), but recommend that investors keep their fingers on the trigger and exit if near-term lumber price appreciation (most likely spurred by further sawmill downtime) isn’t forthcoming. Looking further out, their 9-12-month TP is $34 (60% upside).

BWS Financial

The company experienced a slowdown in its largest business segment, packaging, three quarters ago but is now starting to see an increase in quoting activity. The slowdown did little to pause its tuck-in acquisition strategy, which has expanded the company's size in packaging and aerospace. TRS is on pace to generate earnings growth in 2023 and 33% earnings growth in 2024. The stock is underfollowed and trading near its lows of the last three years even though the business has evolved since then. TP $40 (55% upside).

Inflection Point Research, LLC

China contagion has spread to the US as IPR’s carrier, retail, and supplier checks indicate iPhone 14 sell-through continues to soften, coming in below expected demand for Apr. IPR believes AAPL’s planned test equipment purchases from Keysight, LitePoint and Anritsu were cancelled or delayed, suggesting slower production looking into 2H23. RF component purchases from Qualcomm, Cirrus, Broadcom, Skyworks and Qorvo have been trimmed, reflecting weakening demand. AAPL's Q3 hardware sales typically drop about -9% Q/Q, but IPR believes iPhone 14 could see declines closer to -20%. The iPhone 15 could also prove disappointing.

Japan

Entext

Renesas has been a star performer for Sean Maher (+80% YTD) and he now adds Rohm to his basket of stocks - trades on a sub 14x PER and is targeting sales of 600bn JPY at an operating margin of 20% and an ROE of 6% by FY25. As well as being a play on power efficient materials like SiC, Rohm’s ultra-high-speed Control IC technology maximizes the performance of gallium nitride (GaN), which offers higher breakdown strength, faster switching speed, and higher thermal conductivity - power devices based on GaN significantly outperform silicon-based devices. GaN high-speed switching devices will become more important as AI capex explodes and energy / compute efficiency is a priority.

Emerging Markets

New Street Research

With good ARPU support from post-paid 5G, and in launch phase for pre-paid, New Street are lifting their mid-term estimates for Mexican wireless (worth $2.5/ADR); they think this business, with a globally unique market structure, merits a 9x 24E EBITDA multiple. They have also nudged up regional fixed operations following raised FTTH efforts (<$1). AMX’s competitive position is reinforced by its rock-solid balance sheet (in a region where there is significant balance sheet stress) and which allows for a rising cash return from what is expected to be the 1Q23 buyback trough. Recent MXN and BRL strength have also been supportive, adding another ~$2 per share to their TP of $27.

Copley Fund Research

Ownership has soared to record levels - a consistent unloved stock among Asia Ex-Japan investors between 2010 and 2020, the percentage of funds invested has risen from zero at the end of 2020 to just over 22% today. Over the last 6 months, the percentage of funds invested has risen by 5.8% and a further 9.3% of funds switched to overweight. This wasn’t part of an industry-wide move, with outflows seen in many of its competitors such as Nio, Maruti Suzuki and Hyundai Motor Co. Clearly, investors are growing in confidence that BYD can maintain its leading position in the EV market and further capitalise on the growing global trend towards sustainable transportation.

RedTech Advisors

With its positioning in the low-end and lower tier geographies, PDD has more opportunities to expand in eCommerce than Alibaba and JD.com, and the lowest risk of having somebody encroach on its turf. Douyin and Kuaishou only have niche eCommerce operations and will not focus on the average guy in some rural township. Modest improvements in trust among China’s middle class suggest PDD can steal some growth from its upmarket rivals, but no one believes it will enjoy the kind of success in the mid- and upper-tiers of the market that it does now in low-tier markets, and with ~900m customers that will continue to find value in that for the foreseeable future, that’s just fine.

MYST Advisors

The Brazilian pharmaceutical market has grown at a ~12% CAGR “forever”, with only one down month going back 20+ years (Apr 20 when ALL stores were closed). RD has consistently gained ~50bps of market share every year since 2007 and is bigger than the #2 through #5 players combined. The presenter highlighting the stock at MYST’s Consumer Event envisions considerable upside to earnings, underscoring management’s “phenomenal” track record, “incredible” unit economics with ~35% ROIs on new stores, and while current EBIT margins are ~5%, mature stores are yielding closer to LDD’s. TP R$48 (70% upside).

CHA-AM Advisors

In his latest Strategist Diary, David Scott reiterates his bullish call on his top solar panel pick - despite deflation in the industry, LONGi is still growing rapidly, key metrics are improving, and the industry is consolidating around this market leader. The stock has sold off in the past three months and now trades at a very attractive entry point (11x next year’s earnings). David also reiterates his Sell on Nutrien. The share price has already dropped more than 20% since he turned bearish (Feb 22), but David argues that NTR (and the entire fertiliser group) is in a classic early-stage bear market.

Silk Road Research

China Construction: Activity remains weak

SRR's channel checks indicate sluggish starts activity in both property and infrastructure end-markets are largely to blame. SRR had called out persistent funding issues as likely to lead to a slower pick up in new starts activity in Mar (despite strong credit data), and thus, they have not been entirely surprised by the weakness to-date. Encouragingly, their checks indicate that infrastructure starts have started to pick up in May and industry contacts say visibility is decent for new project activity in Q3 (particularly Energy / Power). On the other hand, most said there have been no signs of an improvement in property starts yet, which is clouding the outlook and weighing on industry sentiment.

Macro Research

Developed Markets

Belkin Report

The name’s Bond

The Fed and other central banks got away with murder by holding short-term interest rates at zero, exclaims Michael Belkin, and financial markets are now in the adjustment phase of that fiasco. Forward short-term rates have built in expectations of Fed interest rate cuts, but those hopes are likely to be dashed. Michael is adding shorts in December contracts for SOFR and the equivalent contracts in the UK, Canada, Australia and Hong Kong. He is also adding more bond futures shorts in Germany, France, Spain and Canada, preparing for the global sell-off in bonds that is developing.

Greenmantle

Europe: Fiscal policy and sanctions

Negotiations have begun over the revision of the EU’s fiscal rules, known as the Stability and Growth Pact (SGP). As Niall Ferguson anticipated in February, the European Commission (EC) has proposed a tailored set of standards that would allow indebted member states to run marginally looser fiscal policies. Berlin is somewhat against the new standards, but the coalition of frugal member states it heads within the EU is weaker. Niall therefore expects SGP reform to pass by end-2023. Meanwhile, the EC has recently tabled another package of sanctions on Russia, including a proposal on how to tackle sanctions circumvention by third countries. Even if it ultimately passes the package, Niall expects the compliance tools to be largely symbolic.

Talking Heads Macro

US: Preparing for a hard landing

Manoj Pradhan is going against the US consumer, but he’s also not fighting the Fed. Much like the immovable object and the unstoppable force, one of them will have to give, and every meeting the Fed stays on hold will deepen the damage to the economy. As a hard landing gets priced in (Manoj’s long-standing expectation), policy rates will have to go below neutral. US yields and the USD will start acting like automatic stabilisers. Pay July + September vs Receive 2y1y and 10y. Short S&P vs Japan equities, and move long USD vs CNH, NZD and SEK.

Portales Partners

US: Are the banks really sound and resilient?

There are still a number of banks that are surviving thanks to the largesse of the Fed. They won’t be able to wean themselves off this crack cocaine without severely shrinking their asset bases, resulting in less lending for Main Street USA and an inevitable recession. The last two months have shaken out the banks that took on too much duration risk in their investment security and real estate loan portfolios, but we have yet to have a shake out from the over-reaching on the credit side. Expect bank stocks to trade sideways or even have a relief rally before the credit cycle rears its ugly head this summer. Whatever the near term holds in store for bank stocks, there’s probably another leg lower into the inevitable recession.

Asymmetric Advisors

Japan stocks back in vogue, prefer domestic plays

Tim Morse reiterates his view of why he believes Japan’s inflation rate is likely to surprise the market on the upside, forcing the BOJ's hand into dramatically tweaking its yield curve control which will strengthen the yen this year. This in turn should lead to a major divergence in the relative performance of domestic-related stocks versus multinationals and exporters. In particular, Tim is positive financial names, deep value cyclical and inbound tourism plays. Potential upside in JGB yields will remain fairly limited as domestic institutional investors are waiting in the wings to raise their exposure if the ten-year benchmark rate is allowed to move freely above the bank's current 0.5% ceiling.

Harlyn Research

Only high conviction ideas should be actioned

Simon Goodfellow comments that there are more negative, than positive, high-conviction ideas as of late. These include topping signals in many Eurozone countries. Simon has high-conviction negative signals in Financials across all regions, apart from China, and other pre-recession signals in sectors like US Industrials and UK Materials. The positive signal in asset allocation is for US equities, but the level of conviction is lower than the negative call on the Eurozone and is heavily dependent on the positive view of US Communications going forward. He likes Europe, ex Eurozone, particularly Switzerland and Denmark, and detects signs that India may be bottoming, though the rest of EM Equities are highly unattractive.

Emerging Markets

Vermilion Research

Opportunities in the EM landscape

MSCI EM (EEM-US) has continued to hold above Vermilion Research’s $37-$37.50 line-in-the-sand, meaning they are constructive from a price perspective. That being said, RS has been neutral at best, and they have maintained an underweight to emerging markets. There are still plenty of attractive countries and sectors within the EM landscape. Top country overweights continue to be Taiwan (TAIEX), India (S&P BSE SENSEX), South Africa (FTSE JSE All Share) and Mexico (S&P/BMV IPC). MSCI EM Technology continues to be an overweight, and MSCI EM Energy and Financials have been upgraded to overweight too.

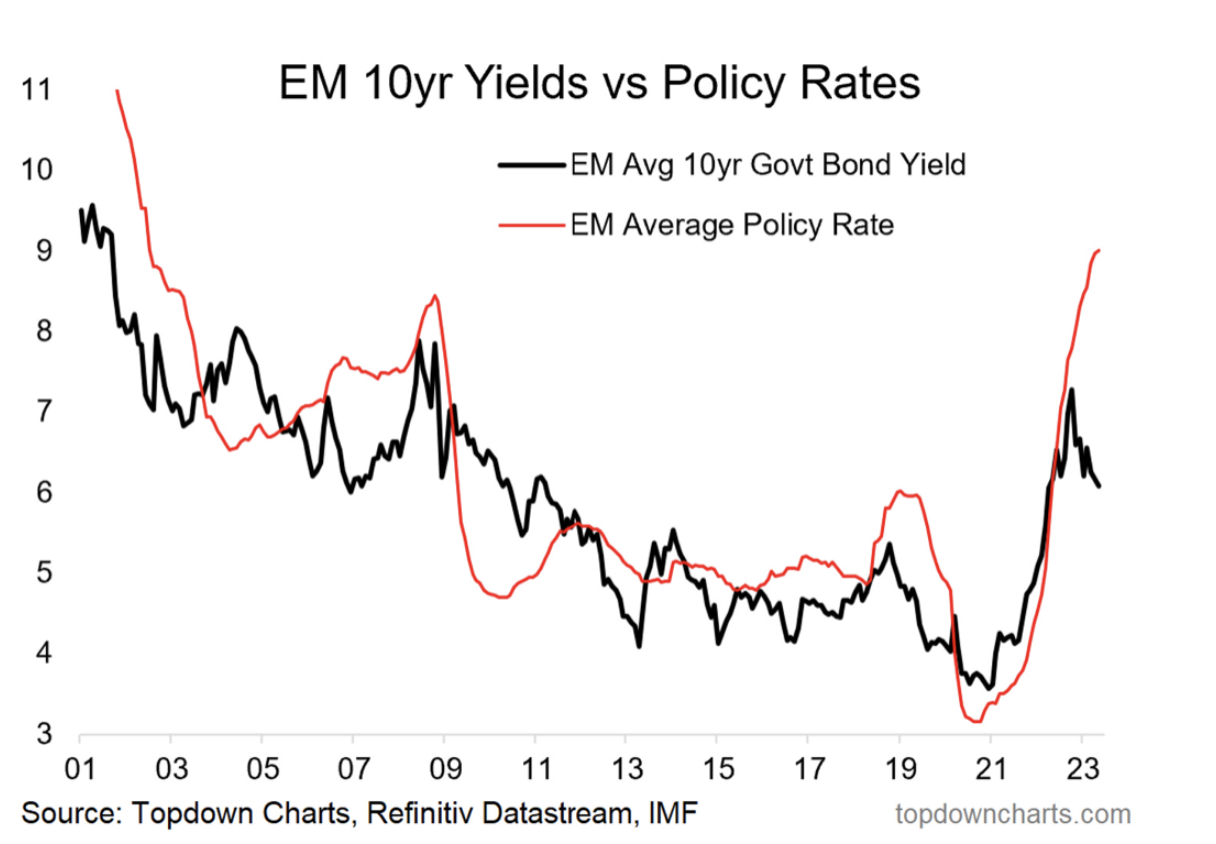

Topdown Charts

Stay the course on EM sovereign

EM sovereign 10-year yields have seen a clear shift in momentum under the surface with country breadth indicators moving steadily lower, and average yields looking to be putting in a possible head and shoulders top. On valuation, Callum Thomas sees EM sovereign as cheap – a key part of that is the divergence of yields vs nominal GDP based valuation model. It’s only a matter of time before policy rates peak across EM, a key piece of the puzzle for sovereign bonds to find sustainable performance. Remain bullish.

PRC Macro

China: Balance sheet impairments plague property

The current official and market consensus view on China is that macro weakness is a function of inadequate demand. William Hess disagrees, believing that this mistakes outcomes for underlying causes. The latter are a function of ongoing balance sheet repair in large segments of the economy. He continues to expect Beijing to introduce more easing measures in Q2, including steps to lower debt burdens for households and local governments in the form of 15 bp cuts to 5-year LPR in both May and August. However, this alone will not resolve systemic balance sheet problems, and until policymakers address them, the effectiveness of conventional demand side policy measures will remain subdued.

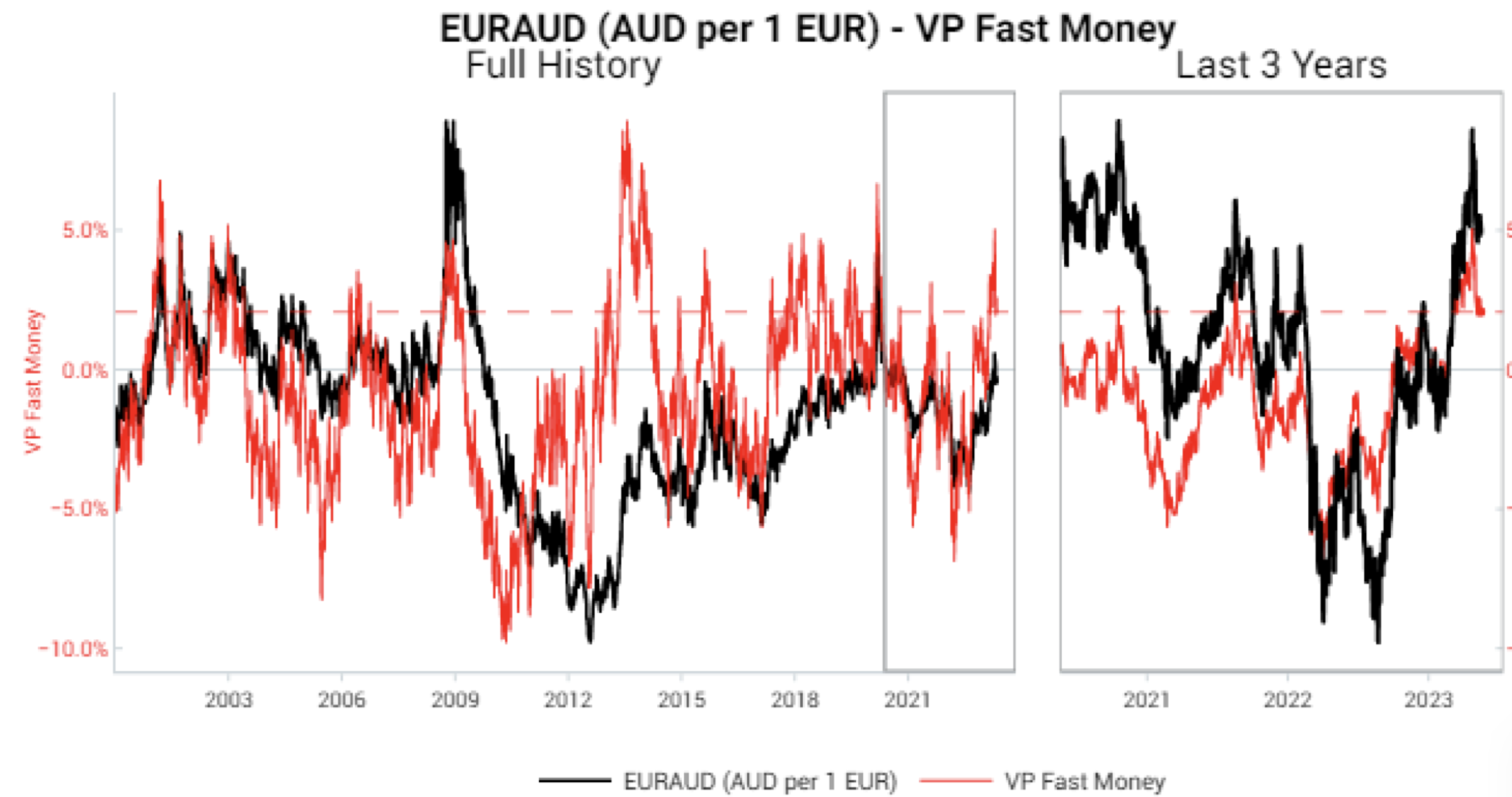

Variant Perception

Playing the China growth theme

The China recession is over, but sentiment towards China remains extremely negative and there is material idiosyncratic risk in direct China assets. Whilst recession risks remain elevated for the US and the Eurozone, recession probability in China has collapsed to zero, providing a catalyst for a relief-rally in beaten-up China-linked assets. If you want exposure to the China growth theme without a high level of political risk, look to SHORT EUR/AUD, taking advantage of the Eurozone’s weakness and Australia’s direct exposure to a recovering China. There’s quite a lot to suggest EUR/AUD downside in coming months, including Variant Perception’s main speculative flow proxy, VP Fast Money (see chart).

Emerging Advisors Group

Ghana: Not giving up yet

Ghana was pushed into sovereign default by a virulent market strike and currency run last year, exacerbated by wide fiscal imbalances and a very high public debt burden. At the same time, however, Ghana also has a favourable external position, with relatively strong exports, a balanced basic BOP, no net funding gaps and an external debt/export ratio that is visibly lower than in other frontier high-stress/default cases. If Ghana is successful in adopting a fiscal consolidation program and external investors remain cautious, we could well see dollar debt become an attractive prospect, similar to what Jonathan Anderson recently concluded on Ecuador. Stay tuned.

Totem Macro

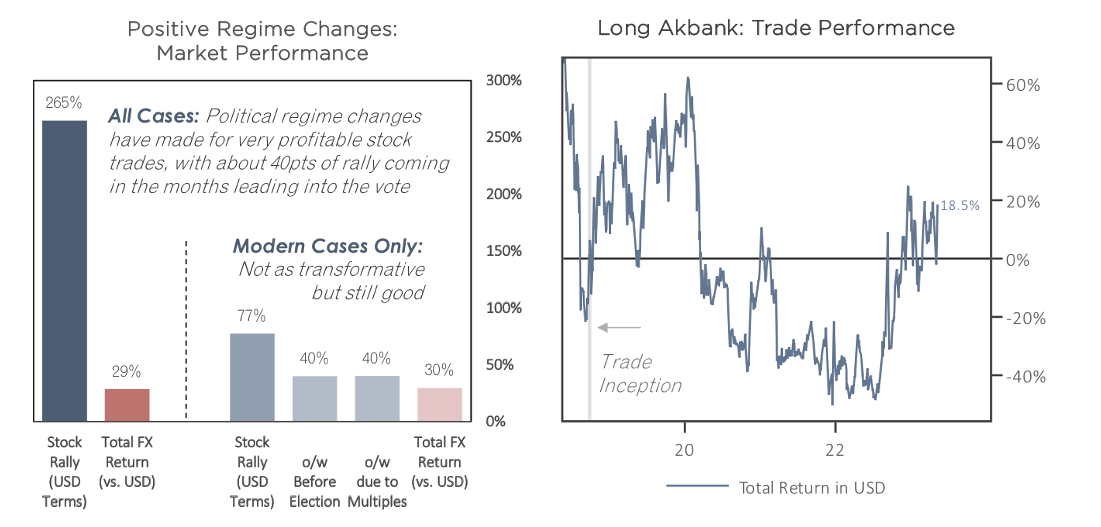

Turkish elections

Whitney Baker held her Turk bank equity position through all sorts of headaches and badly-managed macro shocks, and then it doubled last year. She has tactically exited her Akbank position to lock in gains and will sit out the political volatility during and after the elections, believing any subsequent initial rally will fall victim to the ensuing recession and local selling. But once that’s absorbed, there’s so much upside that Whitney expects to re-enter then. Regime changes often bring about very profitable stock trades, with equities the better way to play it than FX. Once the dust settles, buy back lower and enjoy the upside.

ESG

Sustainable Market Strategies

Sustainable plays in a diverging world

Diverging economic activity between EMs and DMs suggests that investors should look for opportunities in EM companies with credible sustainability characteristics. If most of USD strength is behind us, then EM companies with exposure to global markets could benefit from weak exchange rates before they start appreciating against the USD over the medium term – and those with exposure to India’s secular growth story should continue to perform well in the current environment. From a tactical perspective, holding a diversified basket of EM sustainable companies in various industries and countries could offer interesting upside for investors looking to gain exposure outside of traditional DM sustainability plays. In this context, SMS believes that companies such as Hero Motorcorp, Suzano and Klabin offer good value at a reasonable price.

Saltmarsh Economics

Ranking sovereigns on climate change risk

The Saltmarsh Economic Climate Index (SECI) is a newly launched measure that quantifies the sustainability of economic output, scoring and ranking individual economies on their ability to absorb climate change risks. The SECI combines four sets of variables the Saltmarsh team believe are important to help quantify a country’s ability to absorb climate change risks: 1) exposure to physical climate change risk; 2) emissions and energy usage; 3) macro capacity to deal with the climate change challenge; 4) human capital and institutional strength. Please contact us to find out more.

Commodities

Grey Investment

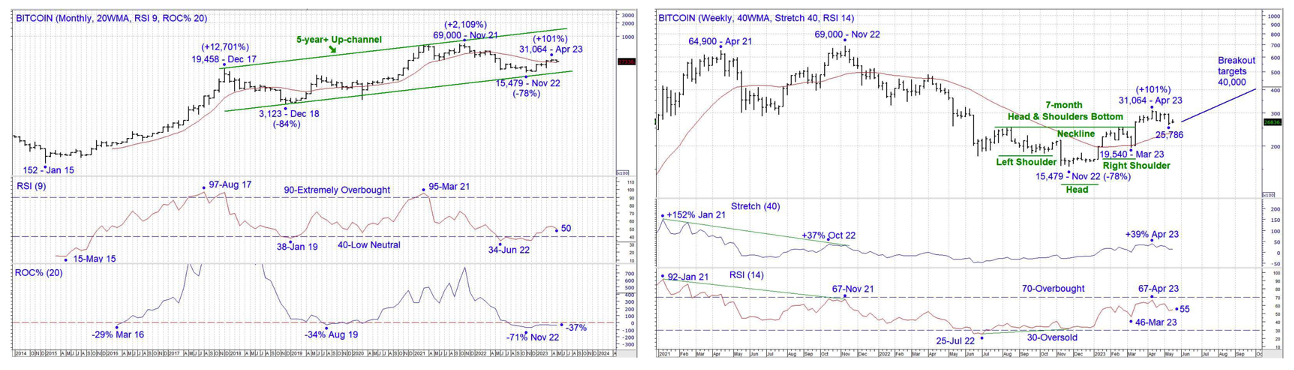

Bitcoin: Climbing higher

Bitcoin’s monthly chart shows price advancing in a 5-year+Up-channel (chart 1). Chris Roberts’ base case is that 2022 saw another cyclical low within that channel, and an advance towards the top end of that channel is now unfolding (USD$100,000+). The weekly chart (chart 2) shows a breakout from a 7-month Head & Shoulders Bottom, targeting an advance to USD$40,000. The area of the 40-week WMA should act as support, and Chris expects RSI to be restricted to a test of the Neutral Zone at 40-50. Watch out for buying opportunities soon.

Vanda Insights

Crude lacks support beyond a bump from US debt ceiling deal

While the stalemate on the US debt ceiling is a headwind for crude, the deal is not going to turn into a strong tailwind once finalised. Vandana Hari expects crude to enjoy a relief rally as the debt ceiling shadow lifts, but the gains that stick will likely be modest. For the oil complex, there is added bearish pressure from the drip-feed of evidence that Russia has not cut output by anywhere near the 500,000 b/d it has announced. Vandana doesn’t expect OPEC+ energy ministers to agree to more production cuts in their June 4th meeting, but Russia’s non-compliance poses some tough challenges for the group going forward.

Meridian Macro Research

Gold and Silver: Recovery ahead

The Meridian Macro team expect more volatility in gold and silver prices over the next couple of weeks as the debt ceiling debacle remains front and centre, however the message from the Fed is clear: they are set to pause (if they haven't done so already). The outlook for Gold remains very positive, and the team expect a recovery past $2000 (and past $24 for Silver) before long. There is clearly a big effort to prevent a precious metals breakout, but these efforts will ultimately fail. While volatility may continue in the near term, any further sell-off episodes will be shallow and recoveries swift.

TenViz

Energy boost

TenViz offers AI-powered tools for investment advisors and fund managers. Lately, their key bullish theme has been to BUY energy. For crude, we are seeing pre-Ukraine war levels and prices in backwardation, a bullish sign. Investors should also look to BUY Uranium – the world will need a lot of it – and gasoline. Consider snapping up oversold energy indices too as they are poised to bounce back, with suggestions including BUYs in energy exploration and production, including a fresh BUY on EQT Corp; another fresh BUY in the Oil Services Index, including a BUY on Halliburton.