Company & Sector Research

Europe

New Street Research

Telcos: Ignore the negative sentiment

The overall picture for European telcos in 1Q23 was actually pretty good, according to analysts at New Street - service revenue trends remained at their highs and were stable at +0.9% y/y; EBITDA remained positive, and given the phasing of energy and wage drags, and given that price increases are yet to kick-in in earnest, New Street expects trends to improve in the latter part of this year. They would single out Telenor as a key Buy recommendation with Norway as one of the fastest growing markets and are also encouraged to see Spanish service revenue growth turning positive for the first time since 4Q19 which is supportive of their Buy recommendation on Telefonica.

Sandalwood Advisors

Sandalwood estimates Hermes APAC ex Japan revenue (EUR) y/y to accelerate to high-end of consensus in 2Q23, outperforming other luxury players with consistent strength. Hermes shows solid performance in Greater China at high double-digits on yo2y basis, partly due to easy comps, but mainly thanks to its brand positioning as an ultra-luxury brand targeting the wealthiest consumers whose spending has remained robust. HK and Macau also saw strong sales, nearly double 2019’s pre-Covid level, driven by wealthy travellers and inflation.

Willis Welby

Expectations analysis for European Apparel & Branded Goods

Revisions for stocks in this sector continue to improve with the median move in consensus Y2 EBIT over the last three months now an upgrade of 3.7%. These good revisions alongside recent share price weakness mean the implied to Y3 EBITM ratio has fallen back to 97. Moreover, consensus Y3 revenue growth of 7.5% is still a big premium and for most stocks should compound well for shareholders. In this report, Willis Welby focuses on the opportunity at Richemont, but also likes Inditex which has had very strong revisions post recent results as well as Moncler.

TobaccoIntelligence

The tobacco giant will petition Belgium’s highest administrative court, the Council of State, to annul a royal decree banning the sale of nicotine pouches. The company says Belgian health minister Frank Vandenbroucke announced the coming ban - due to come into force on 1st Oct - without taking into account either recent science or the opinion of the country’s Superior Health Council.

Gradient Analytics

The FY23 consensus gross margin estimate implies a relatively modest 72bps y/y contraction - given that inventory levels: a) appear outsized relative to both trailing and forward sales, and b) may be ageing unfavourably, Gradient believes there is a heightened risk of LONN’s margin performance falling short of this target. Additional concerns flagged include how revenue quality appears to have declined as receivables growth handily outpaced sales growth in 2022 while past-due receivables nearly doubled and surging CapEx / construction in progress could signal that depreciation expense was unsustainably low last year.

Insight Investment Research

Recently launched its first logistics real estate development project at Madrid as part of its Airport City concept in its Strategic Plan 2022-26. Robert Crimes values the group’s real estate at €3.1bn (>4x Sell Side consensus) - existing assets are valued at €1bn and the pipeline at €2.1bn (or €14/share) - mostly from developing buildings at Madrid and Barcelona in 2023-49E, ideal locations to capitalise on strong demand for logistics space, primarily driven by e-commerce. Robert raises his SOTP based TP from €321 to €337 (130% upside) and AENA moves up to 3rd (of 25) on his Stock Ranking System.

Entext

Sean Maher adds NEX his green grid infrastructure basket (includes Rolls-Royce, Cummins, Ming Yang) after unjustified YTD weakness on a 14x PER, a 3-point discount to Italian rival Prysmian. Sean highlights NEX’s recent agreement with TenneT (largest in its history) and successful testing of the first 525 kV DC cable which enables a substantial increase in transmission capacity. Furthermore, as digital decoupling from China extends to subsea data infrastructure, what was already a very strong growth market driven by international data volumes in providing highly sophisticated multi-layer cables now has a further tailwind from national security led duplication and redundancy.

ROCGA Research

Appears on ROCGA’s list of undervalued ideas - using their proprietary Cash Flow Returns On Investments based valuation tools, they have started a new product to identify companies on the spectrum ranging from undervalued to overvalued. This list can be easily modified to cover specific geographies, industries, M/Cap... ROCGA currently covers c.2000 companies across Europe and the US. More details on their systematic and interactive valuation tools can be found here. A trial can be arranged on request.

North America

Housing Research Center

Alex Barron upgrades the stock to Buy and increases his EPS estimate for FY23 from $9.92 to $12.50 (vs. consensus at $10.02) following an impressive 2Q23 - beat on top and bottom line; efforts to improve its SG&A ratio seem to be paying off and guidance on orders / deliveries was better than expected. For FY24, Alex’s EPS estimate increases from $11.69 to $16.00 (vs. consensus at $10.83). Based on his 2023 adjusted tangible book value estimate, the P/B for LEN trades at 1.49x vs. 1.56x for the rest of the group. TP increases from $117 to $142.

JJK Research Associates

JJK continues to worry that FY24 guidance is back-end-weighted, with 1H -MSD revenue guidance expected to rebound to +M to +HSD in 2H, despite Vans’ ongoing underperformance and a challenging macro backdrop. Further, at TNF, JJK has noticed heavy promotional activity recently. They see this as a negative for the brand given its traditional staunch full price stance and an indication that inventory reduction remains a challenge (forecasts for margin expansion are unrealistic). It is going to be a steep learning curve for newly appointed President & CEO, Bracken Darrell, especially given his lack of direct experience in the sector, pushing VFC’s turnaround into 2H25.

Holland Advisors

Andrew Hollingworth previously thought WRB was an interesting business, now he thinks it could be a compelling long-term investment - its valuation has come down from over 3x book value to c.2.1x. Were it to start making ROE’s of 20% again this valuation equates to a look through PE of 10.7x. Andrew notes that the last time the insurance industry had a hard pricing market (2001-07) and interest rates were this level, WRB made some very impressive y/y returns. During that period, its book value per share rose from a rebased $1 level in 2001, to $3.85 by 2007 (+285% in 6 years, an IRR of 25% per annum).

Thompson Research Group

Shareholders vote to shift primary listing to the US as management seeks to capitalise on a golden era for construction - TRG is the first US analyst firm to cover CRH and their initiation report focuses on why the building materials firm is ideally placed to benefit from key secular trends including 1) reshoring / near shoring; 2) US population shift to “smile states”; 3) increased environmental investment; and 4) govt financial support. ~11% EBITDA CAGR since FY13 and CRH expects to generate $30bn in financial capacity over the next five years (vs. $20bn from FY17-21). With ~75% of EBITDA focused on the America’s market, TRG views CRH as a sleeping giant. 12-month TP $86 (60% upside).

Lynx Equity Strategies

As and when pricing of Gen AI applications become transparent to end users, standard ROI metrics will kick into place. Cost-down efforts will become inevitable in order to scale up the user base. NVDA’s ~$30k/chip pricing will not last into the next year, according to KC Rajkumar. He thinks once the novelty of the idea of Gen AI wears off and investors get familiar with alternatives to NVDA, there is powerful downside risks to the stock. KC models the data centre business in FY25 up 10% (vs. consensus up 25%) and overall GM/OM at 65%/45% (vs. consensus at 70%/52%). Even at a 50x multiple he gets a TP of $360 (vs. Street targets closer to $500).

Behind the Numbers

One cannot begin a discussion of OKTA without bringing up the ever-changing definitions of non-GAAP results. The items that are being added back continue to grow and are helping to boost earnings. Despite reporting beats in each of the last three quarters, BTN argues that without some short-lived cuts in expenses OKTA would have missed each one. The company is still unprofitable and FCF negative if it cannot pay employees with stock compensation at >30% of sales. The retention rate is falling due to decreasing upsell rates and a lack of expanding the number of seats, macro headwinds are getting worse and deals are taking longer to close.

Paragon Intel

Evidence suggests new CEO Carl Eschenbach will profitably scale WDAY to over $10bn in sales - a legendary enterprise software leader, he will boost the group’s go-to-market capabilities, driving greater cross selling of Financial Management software, accelerating international growth, optimising organisational effectiveness and driving margin expansion. Eschenbach is one of the most strongly endorsed CEOs that Paragon Intel has analysed, with all sources uniformly praising him, including all six former colleagues protesting when asked if he had any weaknesses, a first in Paragon’s research process.

Inflection Point Research, LLC

As if the cyber threat wasn’t substantial enough, this week cybersecurity experts demonstrated that ChatGPT can be used to create mutating malware that evades detection by EDR. The urgency to implement AI capability into cyber defence products just increased exponentially. It also dramatically increases the need for companies to either initiate or accelerate their zero trust implementation plans. IPR believes ZS will be one of the winners because its solution is cloud native, fully integrated, globally distributed and covers all the bases. Further, its Zero Trust Exchange is a key differentiator that is unique in the industry.

Veritas Investment Research

A troubled past and near-term risk are imposing a significant discount on ALA, offering equity investors an impressive FFO yield of ~17%. The firm’s recapitalisation efforts, including divestitures, now reveals a lower-risk business model with a stronger balance sheet. Its risk-reward proposition is fortified by regulated utility assets accounting for ~60% of EBITDA. ALA reaching its debt service targets in the near term will alter its allocation of capital, shifting away from debt repayments and focusing on shareholder distributions (sees potential for an industry-leading dividend growth rate of 5-7% p.a.) and reinvestment in midstream organic growth. TP $33 (40% upside).

Emerging Markets

Copley Fund Research

China Consumer Staples: Conviction overweight

Steven Holden reports how active MSCI China funds are positioned for the outperformance of the Consumer Staples sector - overweights are near record levels at +3.97% above the benchmark. Today’s 7 most widely held stocks in the sector join a prized group of just 15 companies that have ever been owned by more than 20% of funds at any one time. Dubbed the 20% Club, 8 of these stocks have since left, with Luzhou Laojiao the most recent entrant. The remaining 6 stocks are Kweichow Moutai (the highest conviction holding), China Mengniu Dairy, China Resources Beer, Wuliangye Yibin, Inner Mongolia Yibin and Tsingtao Brewery.

India Independent Insight

India: Affordable housing market attracts a surge of finance companies

The Pradhan Mantri Awas Yojana (PMAY) has provided opportunities for low-income individuals to own homes in urban areas through the Credit Linked Subsidy Scheme. The scheme has benefited both home borrowers and real estate developers, as the government bears a substantial subsidy burden. The affordable housing market is thriving, especially in Tier 2 and Tier 3 locations, attracting a surge of finance companies. However, there are risks associated with above-average growth and credit decisions. Attrition rates are high and employee behaviour can impact loan disbursal. The market could be at a cyclical peak.

Companies covered include Aptus Value Housing, Aavas Financiers, Home First Finance, Capri Global, Mahindra Finance, AU Small Finance Bank, IIFL, Piramal Enterprises and Five-Star Business Finance.

Horizon Insights

Top picks in China Healthcare Services

Hygeia (6078 HK): As China continues to implement the DRG payment model, hospitals with low operational efficiency will be eliminated. This bodes well for Hygeia, as it continues to grow its bargaining power with drug suppliers will only strengthen.

Gushengtang (2273 HK): FY22 revenue grew 18.4% and net income was up 28.1%. In 2023, the company will continue its expansion through self-built establishments and acquisitions. It is expected to add 10 new clinics in 2023.

Sinocare (300298 CH): According to Horizon Insights latest industry surveys, the CGM industry grew c.20-30% (Jan-May) with the annual growth rate expected to reach c.40%. Since introducing new CGM products, Sinocare ranks No.1 in sales on major e-commerce platforms.

Smart Insider

Xiuguo Tang (Non-Executive since 2014) purchases more than 1m shares, spending ~US$1.3m and increasing his holding by 29%. Tang has a good record as a buyer and Smart Insider previously ranked the stock twice based on his purchases: in May 2018, when he bought at HKD 2.69 and in Mar 2021 at HKD 8.53, both proved to be very well-timed. It's encouraging to see him buying again at this higher price level with the stock close to a multi-year high. Stock Rank +1 (highest rating).

Global Mining Research

GMR examines how much Vale Base Metals is worth - this includes the former Inco assets predominantly in Canada, and two copper and one nickel mine in Brazil. They forecast attributable ~325kt copper and ~160kt nickel in 2023, with 30% growth long term. GMR estimates a value of $14bn or ~$3.00/share, based on DCFs, or 23% of the miner's M/Cap. However, with typical premiums Base Metals could see ~$4.00/share, representing a significant hidden option value. A partial sale would allow investors to see more clearly what the assets are worth, and by difference, see how cheaply the iron ore and pellet side of the business is trading (at 0.6x P/NPV10).

AceCamp International

AceCamp’s industry surveys show that TSMC has not decided to adopt TCB for the packaging of interposer on substrate in CoWoS for 3nm chips due to a relatively low yield rate and throughput. Similarly, Hynix is reviewing TCB but has not decided to adopt it for HBM3.5 in 2025/26. AceCamp expects ASMPT's orders to decline 33-50% q/q in 2Q23 due to weakening demand for industrial, automotive, and smartphones. The stock is trading at 25.7x/24.7x/22.2x 2023-25 PE, but sees the stock falling to 15-16x 2023/24 PE given -49%/+4%/+11% y/y EPS in 2023-25. Negative catalysts flagged include substantial order declines, market share loss and the shift to hybrid bonding.

Macro Research

Developed Markets

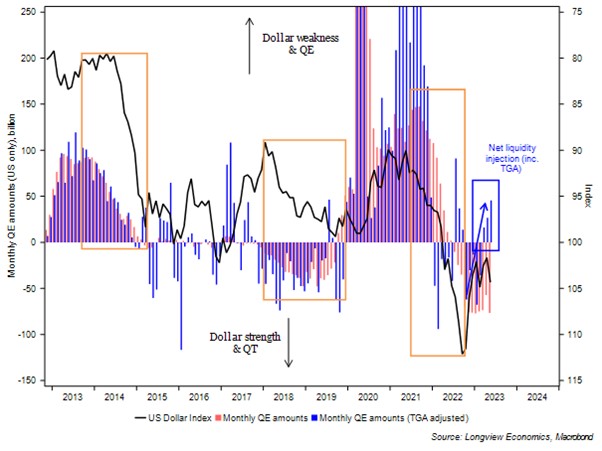

Longview Economics

Stay Defensive - Global macro stress rising

Evidence increasingly suggests that markets are about to start pricing the early stages of a US / Western recession. Weakness in the US and global economy is broadening from cyclically sensitive sectors and towards consumption and services. Normally, when that happens, it’s not long before recession starts. Now the debt ceiling issue has been resolved, the Fed will rebuild its account. That should suck liquidity from markets and enhance, not reverse, the impact of QT. As the chart shows, phases of QT (or tapering) typically result in US dollar strength / risk aversion in global markets.

Minack Advisors

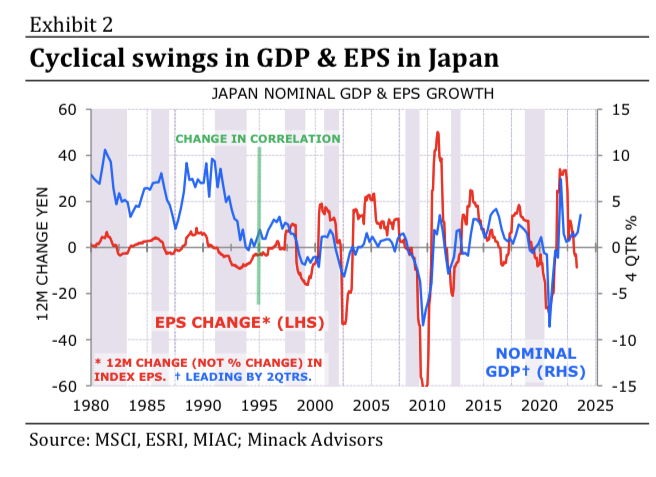

Japan outperforms China despite massive GDP gap

Equity markets and earnings do respond to changes in the economic cycle. However, over the medium term there’s little or no correlation between economic growth and equity returns. Gerard Minack points out that what drives equity returns is the ability of corporates to generate a return on equity through the cycle. Japanese corporates used to be terrible at that, but now are good. Chinese corporates remain terrible. The graph above shows the correlation between nominal GDP growth and the change in index-level earnings in Japan. While fluctuations in GDP always correlate with changes in EPS, the relationship has clearly changed: prior to the mid-1990s EPS would typically rise only when nominal GDP growth exceeded 5%; since 2000 EPS tends to rise when GDP growth is above zero.

Steno Research

More US bank failures are inevitable

Sticky core inflation, a bounce in housing and AI mayhem are all reasons for higher for longer rates. Banks have no way of competing against the rates at money market funds, leading to a slow withdrawal of deposits. To meet outflows banks will sell their underwater assets. Smaller banks are likely to suffer, as confidence will remain stronger at bigger banks. Taking a deeper dive into the core of US banks’ balance sheets and income statements, Andreas Steno find multiple reasons why you should worry about more banking failures in H2. Banking crises always come on the back of either: 1) Horrible loan demand or 2) Extreme deposit flights, which ultimately end in quick collapses. But at the moment, neither of the conditions can be checked off, as we are only witnessing moderately weakening loan demand and a slow withdrawal of deposits - a combination of money destruction and deposit transfers from one bank to another.

Aitken Advisors

The British experiment

Where’s the hurting, are rate hikes working? For twenty years monetary policy was the only game in town, because fiscal policy could not be turned on. Central banks were thus compelled to do things that central banks were never designed to do. Once again monetary policy is the only game in town, but this time it is because fiscal policy cannot be turned off. Yesterday's fifty-basis point hike could restore the BoE’s credibility. The panic selling of UK property exposure continues. As has been the case since last September, global patient capital continues to offer liquidity (bids) for those desperate to exit UK property at any price. That global patient capital inflow is part of the reason sterling has been strong. The HNWI bid for short-dated gilts continues.

Belkin Report

Depressed cyclicals coming to life

The model forecast for US, European and Japanese sector rotation has changed dramatically over the past two weeks. Depressed cyclicals are coming to life and this development could throttle the bubble in AI stocks and provide welcome relief to portfolio managers who have resisted the NYFANG stock bubble. Those are very crowded trades that are vulnerable to liquidation.

Asymmetric Advisors

Yen derating and BOJ policy errors continue

With the latest BOJ decision leaving its monetary policy unchanged and more out of sync with other major economies, Asymmetric thinks the yen plunge will continue towards last year's October lows and force MOF to intervene once again. Without a BOJ policy change, the MOF can't defend the yen alone. The currency market and possibly the JGB market will eventually force the central bank's hand. For now the BOJ's policies look increasingly politically motivated; to appease MOF in its attempt to keep government financing costs from surging.

Behind the Balance Sheet

Into the Minefield - Will private equity blow up in 2024?

Stephen Clapham has taken a look at private equity as he thinks that its meteoric rise over the last 20 years has largely been a product of falling rates and rising valuations. The next 10-15 years will prove a very different environment. He expects that there will be some big blow-ups in the PE space in the next 18-24 months, with mark to market becoming a contentious issue. As a result, private equity will find the going much tougher and pension funds with high allocations will suffer remorse.

Eurizon SLJ Capital

The Long & Short - Global monetary divergence favours a weaker USD vs EUR

The ECB hiked rates by 25bps and effectively pledged to do the same in July (absent a material change in the economic backdrop). Eurizon SLJ sees interesting inferences from analysis of the forecast revisions. The ECB forecasts increased Core CPI projections significantly for 2023 and 2024 with very minor amendments to the growth trajectory. Hence the ECB believes that it can continue to raise rates further without pushing the eurozone economy into recession. The eurozone continues to have a more hawkish inflation trajectory and thus likely a tighter monetary reaction function relative to the Fed in the near term. Eurizon SLJ sees this weighing on the USD relative to the EUR.

Emerging Markets

Totem Macro

Synchronised EM easing

Most EMs across all regions are seeing quite substantial inflationary relief this year. It started with Latam but previously constrained parts of Asia (Korea, India) as well as Eastern Europe are now seeing relief and pricing easing. All major EM economies bar South Africa are now priced for earlier rate peaks & faster rate cuts than they were just three months ago. That was when Whitney Baker first started discussing the prospects of divergent rates across EM vs. DM and especially the US. US terminal Fed Funds has gone back up, and impending EM easing cycles are getting baked in appropriately. That’s especially interesting in the context of disappointing and re-accelerating timely core CPI data across most DMs over the last four-to-six weeks. What this all means is we’re about to see a broad, synchronised EM easing cycle, with the (hawkish) Latam yielders leading the charge, followed next by Eastern Europe.

Trivium China

China: May’s data shows stimulus must target consumption

Reopening has not unleashed the hoped-for recovery in consumption. This, in turn, has limited a critical source of demand for the manufacturing sector, amplifying the pain for Chinese factories from the downturn in overseas purchases. Key to reviving economic activity, then, is boosting consumer spending. This would help bolster confidence in the corporate sector, particularly among private firms. The high level of household savings suggests that a major barrier to this is a lack of confidence: Households have excess savings, but they need to be confident enough in the country’s economic prospects to draw them down. In this sense, the economy is trapped in something of a downward spiral. Households won’t increase spending until the economy has recovered, but weak consumption levels are depressing growth. The economy needs an exogenous intervention to drive faster economic growth, unlocking more household spending.

Horizon Insights

China A-share Market: Buy in June

With monetary tightening, the weakness in global demand will continue for a while. Meanwhile, company destocking behaviour in the US and China amplifies the pain of softening demand in the downtrend. Unlike China's old recovery road in the past decade (property-driven investment economy), Horizon Insights sees opportunities in Chinese recovery with cyclical forces that stem from real business cycle. With company inventory bottoming out, the demand of the real economy will start to edge up from Q3 of 2023. Companies' earnings, as a result, will turn around. With global demand moving up from the bottom in the second half of 2023, company capital expenditures will increase, which in turn adds more support for demand. Broader improvements will be seen in terms of inventory and prosperity cycles.

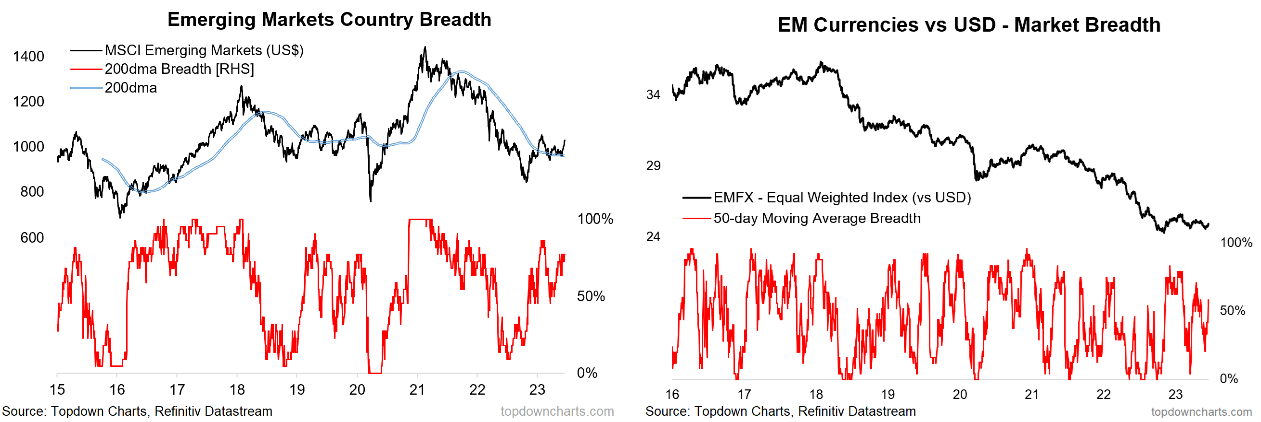

Topdown Charts

China stimulus jump-start for EM?

EM equities ticked higher off support last week on China stimulus hopes. EMFX also rebounded as Fed pause / USD weakness assisted. The macro / fundamental catalysts (China stimulus, USD peak) come as EM equities sit at a key technical point on the longer-term charts. Overall the tactical case for EM equities is improving.

Oxford Analytica

Prospects for South-east Asia to end-2023

The region faces a range of political, economic and security challenges. Many South-east Asian countries will be preoccupied with political transitions in the second half of 2023: Thailand is expected to see the formation of a new government following last month’s general election, while Cambodia will hold parliamentary polls and Indonesia will intensify preparations for the elections set to take place early next year. Regional players will meanwhile work hard to sustain robust economic growth and affirm ASEAN ‘centrality’.

Emerging Advisors Group

Sri Lanka: Sure enough, LKR has rebounded

After the massive 2022 devaluation, the rupee has appreciated smartly over the past few months following the IMF programme announcement. The good news is that external gaps are closed. The country is now running current account surpluses and has IMF funding support. With annualised short-term bill yields still at 25%-plus, we continue to see support for the FX carry trade for now. The bad news is that fiscal gaps are still wide open. The main problem is the budget, where deficits are still at the double-digit levels. There's not a lot of monetisation at present, but if the government can't rein in imbalances it's only a matter of time before it resorts to printing presses, putting renewed pressure on the rupee.

Edge Research & Consulting

Bangladesh: Adopts a market-based exchange rate regime

A contractionary monetary policy for FY24 was announced recently, with the major focus being placed on managing inflation. Bangladesh Bank finally removed the interest rate cap and replaced it with a market-driven reference rate to be regulated by the average 182-day treasury bill rate. According to the new formula, the reference rate will be calculated as the six-month moving average rate of the 182 T-bill with a margin of up to 3% for banks and 4% for NBFIs. Lending to CMSMEs and consumers may be subject to an additional fee of up to 1%. The MOS also announced that the central bank will be adopting a market-based exchange rate, and will no longer be quoting specific rates.

Commodities

Queen Anne's Gate Capital

Chinese stimulus measures may not be enough

Last week global data and policy diverged. The immediate reaction was a reassessment of fundamentals and de-risking of consensus views across rates, forex and commodities. The Metals rally across the complex shows that the “go to” China recession trade has been expressed via short metals. Positioning is cleaner (less bearish). It is not obvious that recent stimulus talk is anywhere sufficient to stabilise the weak property market, and thus meaningfully tighten metals supply and demand balances. Additionally, the old school massive property and infrastructure stimulus seemingly contradicts top leadership's stated “high quality growth” model.

Marex

Oil markets distilled

The potential for stimulus in China should work to support oil demand, which is already at record levels based on refinery processing data. Any weakness in China’s demand has been focused around the property sector, so a pick-up in construction activity would be quite supportive for oil prices in 2H23. The pick-up in demand would also coincide with the OPEC+ cuts taking hold, the US SPR refill, and the potential rebuilding of oil positions by large money managers.

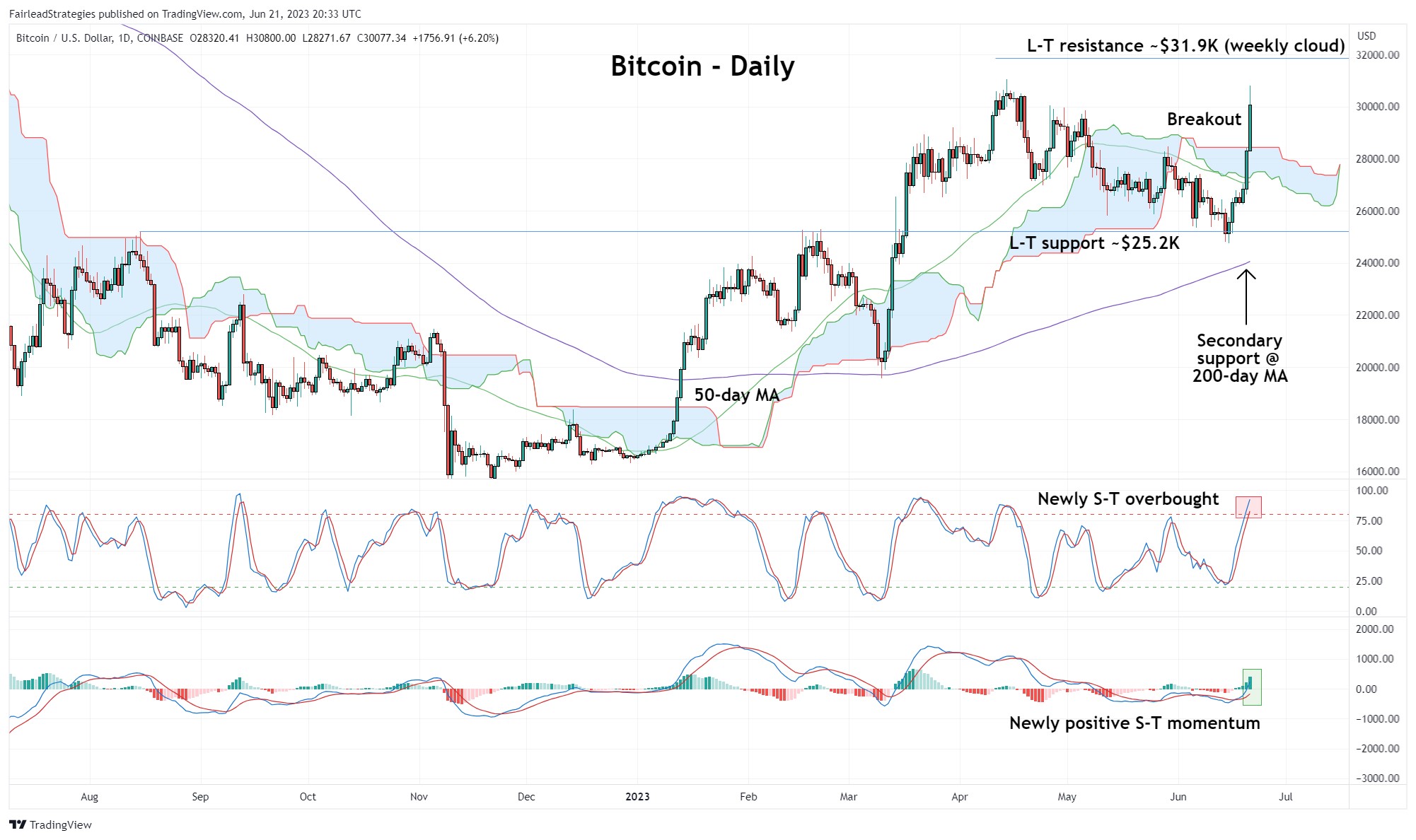

Fairlead Strategies

Bitcoin rallies through cloud resistance

Bitcoin has rallied roughly 12% over the past two days, generating a decisive breakout above initial resistance from the daily cloud model, shown in the attached chart. The breakout suggests the corrective phase that had been in place since mid-April has lost its hold, allowing for the intermediate-term uptrend to resume. Newly positive short-term momentum supports upside follow-through to long-term resistance from the weekly cloud model (~$31.9K). Initial support is now at the 50-day MA ($27.1K).

Veritas Investment Research

Outlook for Natural Gas - We might see higher prices yet

Despite near-term expectations of weak natural gas prices, the longer-term outlook looks promising due to a significant increase in US LNG export capacity and growing demand for natural gas in electricity generation. Furthermore, supply dynamics are showing signs of response from producers, with declining rig counts in the Haynesville basin and indications of production plateauing in the Marcellus and Permian regions. We might see higher prices yet.

ERA Research

Lumber demand remains tepid

Lumber prices moved higher last week for most species as the ongoing threat of wildfires and news of curtailments in western Canada drove increased activity in the market. SYP 2x4s were one of the few products to post w/w declines, with prices slipping by $11 to $385. In Western Canada, S-P-F 2x4s finished the week up $30 at $380, with news of West Fraser’s 33MMbf curtailment (all BC mills except for Quesnel are down for two weeks as of June 19) spurring increased buyer interest. Demand remains tepid and ERA does not anticipate modestly curtailed supply to be the catalyst for a sustained run on prices.