Company & Sector Research

Europe

Paragon Intel

Evidence suggests new CEO Bill Anderson will use R&D, M&A and transformation to grow earnings - Paragon interviewed former colleagues who worked with Anderson at Genentech and Roche for over 75 years combined. Sources were unanimously positive, citing his knowledge, leadership abilities, management style and ability to drive results at both companies. Following his appointment, all but one source would consider investing in BAYN with the one hold out citing concerns about the cultural differences between a traditional German company and a new CEO with an informal, “Californian” management style.

Starling Advisors

Massive overreaction as the share price plunges nearly 40% following a profit warning in the Siemens Gamesa division - the drop erased €7bn in ENR’s market value vs. restructuring costs estimated at ~€1bn. While Alex Dwek thinks it probably means break-even for SGRE is delayed by a year or so, the trend towards cleaner energy is accelerating and ENR is entering a new phase of growth with a good-quality record-high backlog in Gas Services, Grid Technology, and Transformation of Industry, which should convert into high revenue growth, margin expansion and profitability. On Aug 7th management will provide Q3 results and give more visibility on costs, which should act as a catalyst to restore credibility. TP €24.00 (60% upside).

Iron Blue Financials

SPX’s Iron Blue score increases by +5 y/y to 21/60. This reflects: 1) A decade high (10% PBT adj) in stripped out one-off costs. 2) Balance sheet contract assets rising to £12m from £3m. 3) PPE capex exceeding depreciation by 19% PBT adj, a decade high. 4) Lengthened expected life for plant and machinery (from 8-10 years to 10-15, above Capital Goods peers). 5) Likely higher net finance charge post €225m debt refinancing (Sep 23). 6) Additional accounting policies disclosure highlighting management discretion when accounting for cost of inventories. 7) Bad debtor provisioning at a decade low but debtors overdue by >90 days and not provisioned up to 9% of receivables (2021: 5%, 2020: 3%).

Woozle Research

Woozle upgrades the stock to Buy based on findings from their latest surveys - 33% of respondents suggested they would beat 2Q22 sales targets (50% reported they were in line). Expects quarterly sales to increase by 8.3% y/y vs. consensus estimates of 7.9% for software growth at constant currency. Performance also improved q/q with fewer delays and improved sentiment among customers, alongside some pull-forward effects with the looming pricing increases from Jul 1st. 3DX continues to grow and now accounts for c.15% of sales (vs. c.5% in 4Q22). Forward guidance was either neutral or bullish for the next 6 months.

Woozle interviewed 23 resellers and channel partners. Regional sample mix: 57% from N.America, 39% Europe and 4% S.America.

ResearchGreece

Greek Equities: Impressive gains YTD

ResearchGreece’s base case scenario is materialising - Mitsotakis administration renewing its mandate and Greece avoiding a recession. With Greek equities +c.35% YTD they provide an update on the investment case for all the stocks under their coverage including:

Jumbo (BELA GA) - Working for the right reasons, namely valuation, balance sheet, management, business model, growth and dividends. The biggest risk: EU-China geopolitical issues affecting the firm's 70% merchandise sourcing.

Mytilineos (MYTIL GA) - Rating seems wrong, but concerns seem right, namely cash flow generation, corporate governance, energy crisis gains, cyclicality and low visibility. TP €17 (50% downside).

Bank of Cyprus (BOCH CY) - The best bank in Greece / Cyprus, worth >1.0x TBV based on RoTE >17% in 2023 (and >13% in 2025) and CoE of 12%. The first bank in the region to resume dividend payments (>8% next year). TP €5.7 (90% upside).

North America

280First

AI driven 10Q / 10K filings analysis

Text discussions within financial filings contain material information - since there are always reasons when companies change their wordings, being alerted to these changes allows investors to realise potential risk factors and opportunities before they are reflected in the market, ideal for idea generation and portfolio monitoring. Recent highlights include Capri (market share fears / no more international expansion), Home Depot (rethinking dividend programme), Keysight Technologies (order cancellation & delays / competitors expand market position), Microchip Technology (ASP concerns) and Monroe (takeover target).

MYST Advisors

Building fibre is a lot more difficult, more expensive and takes longer than “what’s in a spreadsheet” - subscriber penetration rates have been underwhelming and trends are only worsening. Cable stocks have massively derated and now trade at 6-7x EBITDA while FYBR trades at ~5.5x, so the opportunity to expand from a “Copper to a Cable” multiple has disappeared. Expects FYBR to lower guidance when it reports 2Q results in early Aug. TP $8 (50% downside), but longer-term flags bankruptcy risk (leverage is ~4x but will rise to ~5.5x by the time the build is finished. There is no FCF and the company will burn another ~$5bn of cash between now and the end of 2025).

Verbatim Advisory Group

Verbatim's latest channel survey reveals Jun trends significantly weaker than May. Similarly, Q2 trends are considerably weaker than Q1. Traffic has slowed down, and respondents are attributing it to the ongoing customer boycott and price inflation that is causing a slowdown in spending. Popular products include summer items and essential food, with promotions aimed at offsetting weak traffic trends. Inventory levels are mostly just right, but Verbatim is hearing about some shortages of beauty products and toys. Verbatim are incorporating a bias of negative 550 bps in Jun. With a Jun Raw Comp of 0.0%, their Jun Comp Estimate is -5.5%. Their Q2 QTD Comp Estimate is -3.2%.

Off Wall Street

Structurally unprofitable and competitively disadvantaged with aggressive accounting and a history of giving outlandish targets and then failing to deliver - management has made a big bet on transforming into a vertically integrated hydrogen producer, but their long-term targets, on which street analysts are basing their numbers, appear to depend on highly unrealistic assumptions around costs, the availability of critical materials and competition. Cash burn has accelerated and the company has almost used up the capital it raised during the 2021 bubble. OWS thinks PLUG has a few quarters of liquidity remaining and will probably go bankrupt.

Portales Partners

Banks announce capital plans after passing Fed stress test

Charles Peabody believes the banks conducted themselves well in fairly harsh stress tests that indicate an excess of capital in the sector. If regulators don’t panic, the path from crisis to normalisation can proceed even if we confront a mild recession. Charles favours the fundamental strength of JPMorgan but notes the underappreciated capital power of PNC and Wells Fargo. He is attracted to the adjusted yields of Citizens Financial and M&T while commenting that Morgan Stanley and Goldman Sachs also fare well in this category.

Alembic Global Advisors

Recent underperformance and valuation multiple compression vs. Linde are overdone - APD has underperformed the German gas major by a whopping 82% since the two companies hit their Mar 2020 low. Hassan Ahmed points to APD’s attractive end-markets and favourable geographic exposure vs. peers. He also argues that higher exposure to the hydrogen economy and growth projects aren't being fully appreciated. The company has a slew of growth projects coming online over the next five years, which, based on Hassan's calculations, should add >$38 per share to valuation. Finally, APD hasn’t really put a dent in its balance sheet, suggesting ample room for future ventures.

Abacus Research

Abacus has been searching for companies with a very clear Generative AI monetisation roadmap, with a large TAM and revenue growth acceleration implications starting soon. ADBE's recent innovation has been amazing, the speed and quality of Firefly's launch is highly unusual for a company of its size, suggesting a new product cycle is imminent. ADBE is in an industry vertical that is clearly at the cutting edge of workflow adoption, not all verticals will benefit as fast. LLMs are tools, and tools need distribution - SaaS platforms are best positioned to benefit. SaaS growth in general will increase again due to an AI product cycle after the cyclical slowdown.

BWS Financial

The developer of radio frequency identification chips used in RFID tags benefited when companies were facing supply chain issues which resulted in ordering much more inventory than necessary. Hamed Khorsand thinks it is unrealistic for revenue growth to match last year's strong performance especially since PI is heavily dependent on retail apparel and its largest customer is talking about a challenging environment. He argues the stock is priced for perfection - it currently trades at a price to sales multiple of 8.2 times and a forward PE of 44. Hamed’s TP is $45 (50% downside).

AceCamp International

AceCamp now expects NVDA’s DGX server unit shipments to reach 3k in 2023 and 13k in 2024 (vs. previous estimates of 1-2k and 3-5k). They have revised up their EPS forecasts by 7%/20%/21% and now expect non-GAAP EPS to reach $8.9/$16.52/$20.65 in 2023/24/25. AceCamp’s EPS forecasts are 30-40% higher than consensus estimates and they expect the group's datacentre sales may reach $68.9bn in 2024, 50-60% higher than the street. NVDA is currently trading at 49x/26x/21x 2023/24/25 non-GAAP PE, but AceCamp believes the stock could trade at 35x 2024/25, implying 50-60% upside from current levels.

Sales Pulse Research

Field comments on spending on compute, data centre and edge build outs for AI

1) Data centre operators are running out of space, pre-selling new space and in some cases, aggressively looking to purchase space from end users - beneficiaries include Equinix and Digital Realty Trust. 2) Examples of hyperscalers, enterprises and innovative new AIaaS operators rapidly building compute. 3) Cloud optimisation efforts being viewed as “new normal” vs. temporary headwind. 4) After years of hype but slow growth for edge computing there is evidence that use cases are developing and demand is picking up - Crown Castle was mentioned by multiple industry contacts as benefitting from MEC and Lumen from increased demand for fibre connectivity. 5) Some interesting new data centre operators with well-timed AI infrastructure: Denvr Dataworks, Applied Digital and Napatech.

Japan

Asymmetric Advisors

Trading at 2x EV/EBITDA, at book and with tons of cash, Amir Anvarzadeh thinks Subaru remains highly attractive, especially as he sees significant upside to consensus forecasts of ¥330bn OP. As supply issues disappear, strong customer loyalty, low incentives and rising N.American sales can take OP closer to ¥500bn. Subaru's small size also leaves it with better hopes of retaining its customers as we migrate towards EVs. It will have 3 new models by 2025/26 joining the Solterra, adding a dedicated line in Oizumi by 2027 for 200k units to add to another 200k at Yajima by 2026 - unlike Solterra, whilst it will source the batteries from Toyota with 900 mile range, it will build the new models itself.

Emerging Markets

Silk Road Research

China Autos: 2Q23 retail sales close to pre-pandemic peak

Chinese auto demand has seen a strong recovery after a soft start to the year that was marred by headwinds that have now proved transitory. Encouragingly, both May and Jun sales were near or above pre-pandemic peak levels in the absence of new stimulus, a key data point that in SRR’s view challenges the pervasively negative narrative around the health of the Chinese consumer. Their industry contacts now express increased confidence in a positive growth outlook for 2023 (+5% vs. flat for retail sales). SRR’s checks also point to a moderation in the one-off deep discounts that were geared towards reducing excess inventory which drove a lot of the “price war” talk last quarter.

Hemindra Hazari

Hemindra Hazari finds major contradictions in the bank’s public commentary in contrast to the facts in the public domain - Axis Bank has previously commented on how it aspires to be No.1 in terms of customer satisfaction while withholding the information to stakeholders that it was the private sector market leader in customer complaints in FY22 (the RBI will release FY23 data later). Furthermore, its FY23 commentary highlights the importance of employees, but fails to discuss why attrition has been consistently rising in the last 3 years (it was 34.8% last year). With record customer complaints and such a high churn in staff, Hemindra believes the bank’s entire retail strategy maybe in peril.

Galliano's Financials Research

Victor Galliano thinks it is time to take profits (having upgraded the stock to Buy in Jan 23) given NU’s limited potential for positive surprises and its stretched valuation - the bank faces several challenges including 1) The NPL ratio is set to increase further, given NU’s heavy exposure to credit cards and unsecured lending. 2) The high rates of asset growth have eroded its capital adequacy ratio, from a CET1 ratio of 21.8% in 2021 to 13.7% at the end of Mar 23. 3) The expansion in Mexico and Colombia, where NU is not the dominant neobank, could result in an acceleration of opex, resulting in a reversal of the very impressive efficiency ratio going forward.

Copley Fund Research

Return of the king - after a brief flirt with underweight in late 2022, active Asia Ex-Japan managers have rotated back into Samsung, pushing allocations towards record highs. It captured the largest increase in average holding weight and the largest increase in net overweight over the last 6 months. It also saw the joint 4th largest increase in the percentage of funds with outright ownership (was eclipsed by Meituan, Trip.com and BYD). Samsung has cemented itself as one of the highest conviction holdings in the Asia Ex-Japan region right now.

J Capital Research

China’s laser giants are in a price war

Anne Stevenson-Yang thinks a shakeout is likely as c.20% of Chinese laser companies are losing money - all the leading firms are seeing margins squeezed. Prices fell by c.40% last year. Industry growth has dropped into negative territory: laser companies are hoping that LIDAR and applications in communications and medical technology will save the industry. Lower profits are driving differentiation: optical communications tend to be good territory for sales, printed circuit boards bad. But even in areas of high demand companies are being hammered on price.

Macro Research

Developed Markets

Steno Research

Sticky is the new transitory

In the Steno Research “out of the box” series, Andreas Steno aims at being ahead of the current consensus narrative and think of the next theme that could drive price action before anyone else has given it any noteworthy attention. In the latest edition, Andreas takes a look at the inflation in necessities and whether it is fair to assume that sticky inflation has become the new transitory. Will 2023/2024 prove to be 2021/2022 in reverse? According to Andreas, the fear of a price/wage spiral is in his opinion unwarranted as necessity inflation is already normalising, which will feed through to the wage formation.

Deep Macro

Why central banks will hike even though inflation is falling

The BoE’s recent rate hike tells us that global rates are still going up. This may confuse some people; after all, inflation is falling. However, explains Jeffrey Young, CPI remains stubbornly high versus early pipeline press pressures, with the gap between US CPI and PPI at a historically high level. Central Banks’ current behaviour isn’t particularly odd: Jeffrey looks at Fed behaviour over the past 20 years, noting that they tend to look backward and hike rates at the end of inflation cycles. It makes sense: if the Fed had reacted sooner, the economy may have drifted back into an inflation state.

Longview Economics

US: Feeling bearish

Price action was encouraging for the bears on July 5th, with US equity markets heading lower, led by cyclical/high beta indices. With that, and despite a strong rally last month, upward momentum appears to have stalled in a number of indices. In the US, for example, the DJ Transportation index is struggling at its February high, as is the Philly SOX. Signs of tighter liquidity have continued to build. Short-term models continue to point to a near-term downside in markets. 1-2 week equity trading recommendation: stay 1/3rd SHORT S&P500 September futures, and retain unchanged stop 2.5% above entry (4,593.50).

Markets Policy Partners

German consumer sentiment backslides

June’s PMIs and Ifo Business Climate indicators were worse than consensus expectations, with the latter sinking to the lowest reading since December. Most ominously, the decline was concentrated in the forward-looking component. Futures markets are reflecting expectations that the ECB will get in another 50bps of tightening before year-end. The Markets Policy team believe that growth will deteriorate and inflation will cool in the coming months to a degree that prevents more than 25bps getting done, with the July 27th rate the last in the cycle.

Greenmantle

Japan: YCC remains, for now

The BoJ voted to uphold ultra-loose monetary policy, including yield curve control (YCC). However, some members believe it will soon be time to abandon YCC, with consumption and inflation overshooting expectations. The board clearly thinks that inflation has peaked, and that disinflation risks are skewed to the downside as global demand slows. Niall Ferguson retains his view that Governor Ueda has a dovish bias and will not tighten policy until he sees more evidence of rising household inflation expectations and wage increases for non-unionised workers. Niall remains SHORT yen and LONG Japanese equities.

Radio Free Mobile

Artificial intelligence: Countdown to winter

The current exuberance around AI is simply not going to last, exclaims Richard Windsor. We’re in the 4th AI hype cycle, with the others occurring in the 1960s, 1980s and 2017-19, with each cycle represented by unrealistic expectations, FOMO, and the eventual collapsing valuations. Money is being thrown at start-ups with valuation and fundamentals being an afterthought. LLM models are popping up all over the place, which will put current services such as Chat-GPT under relentless pressure when it comes to their pricing models. Richard only has one AI investment in Palantir, and won’t touch anything else.

Emerging Markets

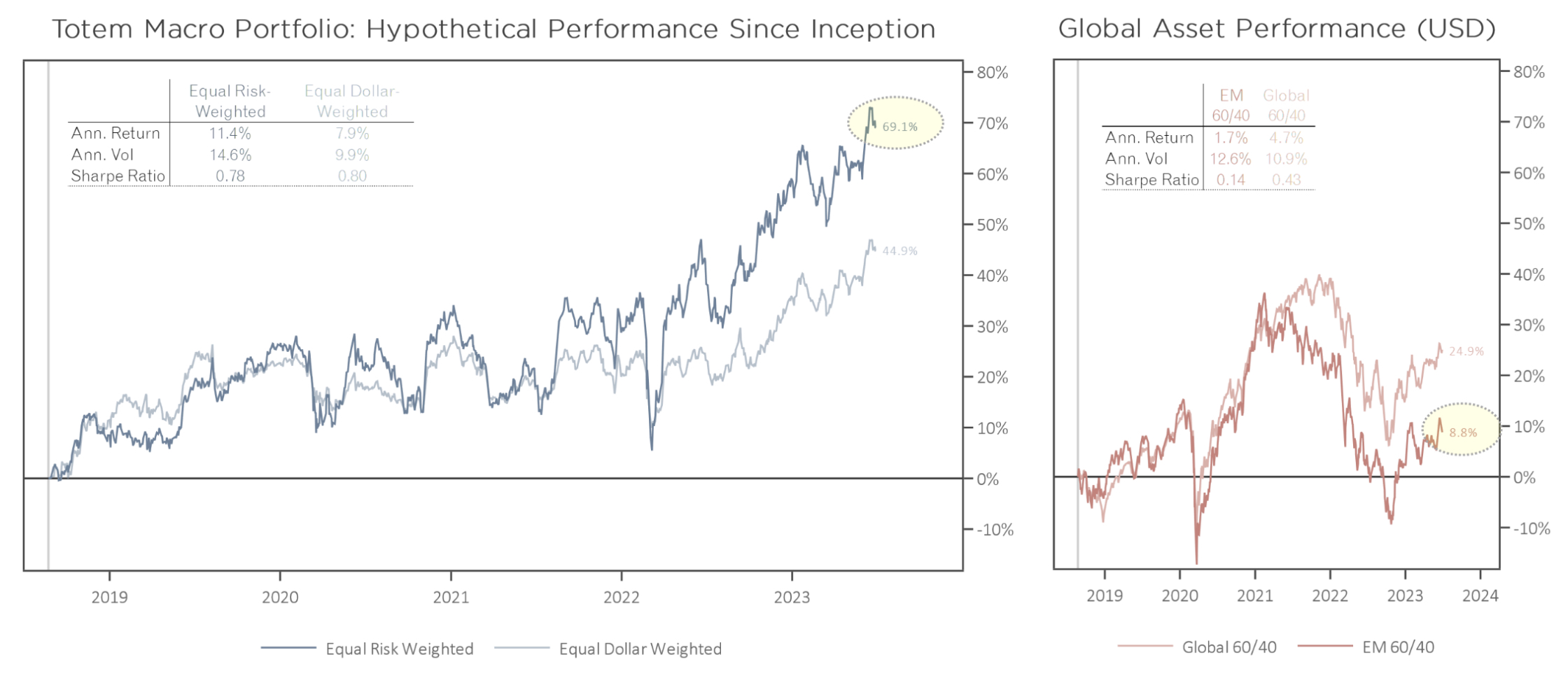

Totem Macro

Excelling in EM trades

After 5 years of launching a as an advisory, Whitney Baker examines her cumulative trade performance since inception. The chart shows the cumulative gross dollar returns of a hypothetical book of her active trades, in two flavours: equal risk-weighted (dark blue) and equal dollar-weighted (light blue). The cumulative gross returns of Whitney’s equal risk-weighted book were 69.1% since inception, over 7.5x the 8.8% total cumulative dollar returns of EM assets over the same period.

Eurizon SLJ Capital

The dollar avalanche building in China

The total stock of dollars held by Chinese entities continues to rise. The dollar’s high carry may at present seem enticing to Chinese entities, but the Eurizon team argue that this configuration is fundamentally unstable. Prospective cuts by the Fed and/or an economic reacceleration in China could lead to a precipitous fall in USD/CNY, as corporate treasurers in China scramble to sell the dollars they don’t need to have. The team see this as a major risk for H2/2023.

Musha Research

From China to India

Ryoji Musha claims China’s economic slump has become conspicuous, evidenced clearly by ailing stock prices (see chart). Unemployment and prices have become particularly serious, with the jobless youth rate reaching concerning levels, and the possibility of a liquidity trap has intensified. Interestingly, Ryoji claims that China will fall into the trap of being a middle-income country and will never surpass the US in terms of economic scale. The growth centre will shift from China to India, with companies already moving or building production lines in the region. The industrialisation of India has begun.

Capital Alpha Partners

China: Cut off

China recently announced export restrictions on gallium and germanium, two materials used in semiconductors, infra-red sensors and fibre optic devices. These moves won’t add additional supply bottlenecks for US defense primes, but they will spur more efforts to develop alternative sources of these metals. However, China’s move poses a longer-term risk for companies that are major defence contractors and who are also major exports of aerospace products to the country; why would China continue to buy products from companies that develop defence products aimed at deterring and defeating China’s military?

TenViz

The case for Brazil

A cyclical upswing is underway in Brazil, with exports soaring, tourism recovering to new heights and an acceleration in money supply all helping to expand GDP by 4% in Q1/23. Now that investors are shunning China and Russia, money is flowing in from EM investors and from US carry funds into the Brazilian real. Investors should take advantage and BUY Brazilian real, BUY sovereign Brazilian bonds yielding 10-12%, and BUY the Bovespa Equity index 12% dividend yield.

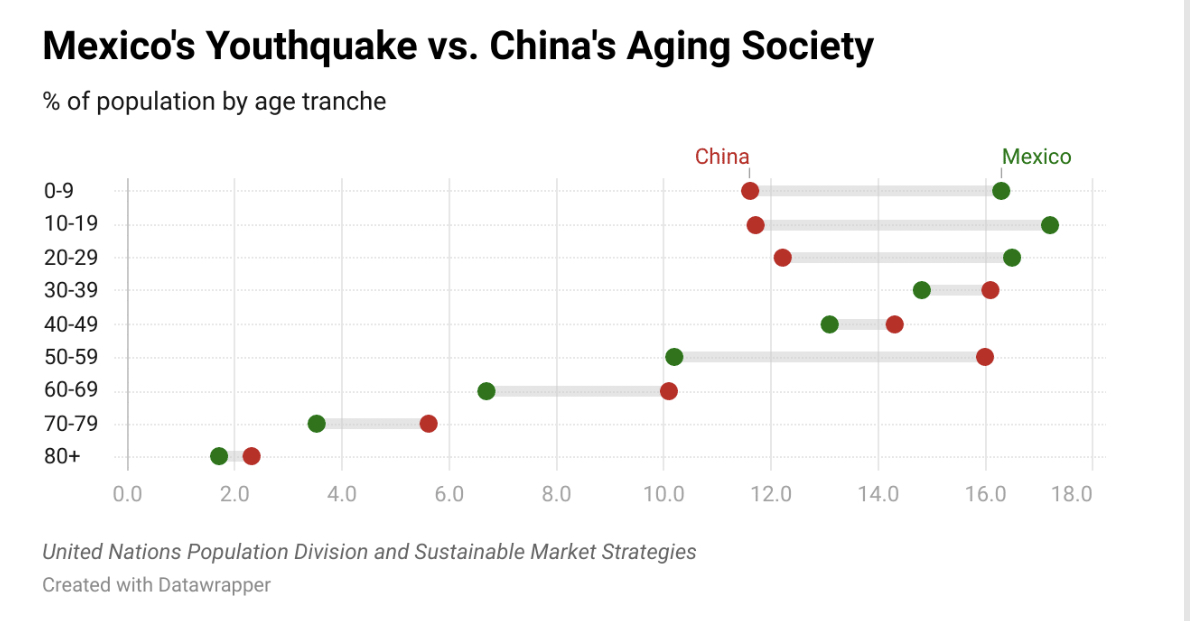

Sustainable Market Strategies

Mexico’s youthquake vs China’s aging society

Mexico is a potential winner from the US’s ongoing desire to de-link strategic supply chains from China. Demography, geography and trade policy all favour a shift towards Mexico, with a more youthful population, a shared border with the US and the USMCA free trade agreement. Sectors associated with building a manufacturing infrastructure in Mexico are well positioned to benefit even if crime and domestic politics remain impediments.

Emerging Advisors Group

Nigeria’s big move

The new administration has come through with a big naira devaluation, taking the currency all the way down to the black market rate, a serious and aggressive move. Jonathan Anderson sees this as enough for short-term tactical NGN positioning, as he sees the naira taking a pause at current levels, providing meaningful near-term carry gains for those in local currency markets. However, higher local rates are needed for a stabilisation trade. Jonathan is more interested in Nigerian dollar debt, as devaluation directly helps bolster budgetary revenues and should spur a rebound in oil production.

Teneo

Peru: Provisional stability carries democratic costs and faces July tests

Seven months into Boluarte's accidental presidency, a new power alignment has formed, bringing relative political calm but eroding democratic safeguards. Congress and the executive have entered a de facto co-existence pact to avoid early elections and secure impunity. However, stability remains fragile. Anti-government protests and a change in congressional leadership in July will test the power balance and Boluarte's political strength. Both Boluarte and Congress face extreme unpopularity. The upcoming protests and leadership election will determine their resilience and the potential for early elections.

Commodities

ERA Research

Falling pulp prices will drive down chip revenues for lumber producers

With pulp prices declining, the usual ones will win: low-cost lumber producers who have relied less on by-product revenues for sawmill profitability. This includes the fleet in the US South, where chips and thinnings have been abundant relative to demand for a long time. The ones that will lose are the lumber producers that were already stretched before the pulp-fibre price collapse, including producers in BC. However, rising S-P-F lumber prices will support BC mills in the near-term. Interfor remains the preferred route to lumber exposure; although they see long-term value in the name, they do not foresee a sustainable upcycle until later this year.

Veritas Investment Research

Copper: Pain before gain

During the last 20 years, copper prices increased meaningfully at a CAGR of 8.4%, albeit with substantial volatility. The market believes copper is under-supplied and prices must go up. However, copper prices are driven by China’s real estate completions, and weakness will have an impact on prices in the short-term. Growth in the copper consumption of EVs and electric generation may not be enough to offset this. Watch out for a surplus in the next 2-3 years, with prices remaining at the current level until 2025.

CPM Group

Expect higher silver prices and plenty of available metal

In his latest video, Jeffrey Christian discusses the recent political unrest in Russia, spotlighting the conflict between President Putin and Yevgeny Prigozhin, the commander of the Wagner Group. After discussing Russia’s standing as a global economic power, he concludes by contemplating how these factors could impact the markets for gold, silver, platinum and palladium.

Click here to watch.