Company & Sector Research

Europe

Willis Welby

Consumer Discretionary & Industrials

Both these stocks look seriously cheap and both have seen upgrades over recent results. Jet2 comes with very strong finances and a lot of market share growth. Of course, travel can be cyclical and lots of the cash is not really theirs, but Willis Welby’s adjusted implied to Y3 EBITM ratio is just 25, which is really low. BAE’s share price responded well before giving part of the gains up on the announcement of the Ball acquisition. Willis Welby considers BAE to be a first-rate international defence company and the expectations ratio of 57 is at a major discount to its largely US peers.

ROCGA Research

ROCGA has recently launched a product that ranks companies using their own CFROI based DCF valuation modelling tools. The list contains the UK’s largest companies ranked according to warranted value, the most undervalued to the most overvalued. CWK appears in the top part of the list, along with Sainsbury, Imperial Brands and ITV. Among others, Sage and Ocado appear at the bottom. ROCGA also covers the US and European markets, with over 2,150 companies in total.

the IDEA!

Assuming a FY23 dividend of EUR 804m and when adding the EUR 250m share buyback, the company is returning EUR 1,054m in cash to its shareholders. Relative to NN’s market cap of EUR 9.852m, this translates into a cash return of 10.7%. Based upon the firm's healthy financial position on the one hand and the fact that approx. 78% of the recurring EUR 250m share buyback has been completed already, the IDEA! believes there is still room for additional cash returns. All in all, the NN equity story is still very much intact as is the IDEA!’s positive stance.

Starling Advisors

The company's new strategy is starting to bear fruit. The pipeline has improved and a new wave of promising drug candidates is helping NOVN re-gain its lost momentum. It has recently reported good news on the product side - with the extension in the EU for Entresto, the positive readout for NATALEE, as well as the approved new site of production for Pluvicto - and now showing strong growth and margin expansion. As NOVN continues to deliver good results, the stock should re-rate.

Iron Blue Financials

Following publication of its 2022 annual report, Iron Blue increase their SAND score to 24/60 from 22/60 to reflect higher stripped out one-off costs (restructuring and wind-down of Russian operations) and changed DB pension liabilities assumptions (higher discount rate, lower salary increase expectations vs. peers). Regarding governance, Iron Blue continues to flag that half of the board could be deemed non-independent and non-audit payments made to PwC are above average.

North America

Hedgeye

Why is the Company buying back stock at this price? Wingstop announced that its board of directors approved a new share repurchase program with authorization to purchase up to $250M of its outstanding shares of common stock, effective immediately. WING lapped the easiest comp of 2022 at -3.3%. The 10-12% guidance on the same-store sales implies low to mid-single digits SSS for the year's back half.

Abacus Research

Private equity credit is in the early innings for a structural shift, taking share from the troubled regional banks and positioned for a substantial increase in investor allocation. There are excess returns available and one would assume the ability to raise even more AUM. With a history of attractive returns in private credit alternative asset managers like ARES have proven they are excellent businesses. The bet is AUM growth beating expectations and Abacus believe this is the perfect environment for this to happen.

The Edge

One of eight global companies in October performing a Spinoff, splitting into two listed entities. Spearheaded by the Rales brothers who have a history of wealth creation, DHR will Spinoff Veralto (VLTO), a pure-play water infrastructure company, on October 2. This will be DHR’s sixth carve-out and its third Spinoff. For insights and opportunities, reach out to the Edge Group ahead of the break-up!

Valens Research

MRK's flagship cancer treatment, Keytruda, is under patent until 2028, and as a biological, has a stronger economic moat than the market recognises. Valens believe the market appears to be understating Keytruda’s total market opportunity as the number of approved indications continues to increase. New indications have the potential to grow Keytruda’s target market substantially, which could boost revenues 10%-25%+ annually. It’s currently used in several collaborations with pharma and biotech companies like Moderna. These combination therapies add to Keytruda’s competitive moat, as they mean any potential generic would need to get approval for the same combination therapies to be disruptive.

Singular Research

AEHR offers a compelling investment opportunity for sustained growth. Their earnings call highlighted outstanding performance, with $65 million in revenue, $17.3 million in non-GAAP profit, a 62% YoY growth, driven by demand for innovative wafer level test and burn-in systems. The thriving silicon carbide semiconductor sector for electric vehicles and photonics has contributed significantly. Singular's Buy rating stands with significant potential upside - $75 target price.

Off Wall Street

HPQ's 3Q23 revenue of $13.2B fell $180M short due to weak PC and printing sales. Earlier, management's $3.5B FCF projection for FY23 was skeptical. Now they have revised it to $3.0B, requiring a challenging $1.8B 4Q23 FCF. Management's explanations were perplexing. Reasons for the EPS and FCF cut included weak Chinese demand, falling printer sales, cautious enterprise spending, and high PC inventory pressuring prices, hinting at future margin issues. Despite this, management claimed 4Q23 margins would be high due to cost reductions. The call lacked AI emphasis, and management admitted a lasting 20% Y/Y printer sales drop's impact.

Arete Research

Despite FY23's difficulties, Qualcomm appears poised for positive growth, improved margins, and a favorable risk/reward scenario, supported by a $149 price target and 34% implied upside. The anticipated Nuvia-based CPUs launching in FY24 could drive expansion into new markets. Restructuring possibilities, IoT and Auto division growth, and AI strategy enhancement also offer real growth potential.

Trivariate Research

What is your exposure to AI?

In their 2023 outlooks last November, the top four equity firms overlooked AI in US equity investing. Yet, Nvidia's unprecedented forecasted revenue surge from 10% to 64% growth in May, the biggest ever for a mega cap stock, surprised due to AI's impact. AI's comparable significance to the 2000 internet boom makes it a pivotal market driver. Monitoring AI exposure is crucial for CIOs and CROs. From analyzing 180,000+ earnings transcripts, Trivariate identified AI keywords, forming a top 50 AI stock basket and a "Ex-AI" basket for comparison.

Australia

Rimor Equity Research

Australian carbon risk

The Australian government has made numerous steps to drive a constraint on carbon. The safeguard mechanism was amended on 1 July-23 and other changes to drive decarbonisation are coming. There are also market pressures, both domestic and offshore. Rimor believe very few companies and investors are stress-testing the impact of an elevated carbon price. Rimor deemed carbon risk faced by Ampol, Cleanaway, Incitec Pivot, Qantas and Orica as requiring further analysis.

Japan

Azabu Research

Nihon M&A Center’s stock peaked in Nov 2021, plagued by accounting scandals, the stock has underperformed in 23 of the last 33 months. The most recent quarterly results saw a 52% decline in operating profit on a 9% decline in sales. Before peaking though, the company grew sales and operating profits at a compounded average annual rate of more than 20% for 13 years and routinely earned a return on equity more than 3x the Topix average. They have also hired new senior staff and completely revamped their internal controls. Azabu believes the company is about to bounce back in a stronger position than ever. Their base-case forecast offers ~30% upside.

Emerging Markets

New Street Research

New Street Research remains bullish on Axiata as they reported underlying revenue ahead of its mid-single digit FY23 guidance, driven across the board except for Ncell and ADA again. Year-to-date EBIT improved as well, tracking in line with FY23’s HSD guidance. However, reported PATAMI came in at a loss, driven by impairments in its Nepal business.

Silk Road Research

The pre-sale price of the Leopard 5 has dropped to below 400,000 yuan and BYD's FangChengBao brand General Manager Xiong Tianbo mentioned that they plan to introduce 1 to 2 new car models every year in the future: During the 2023 Chengdu Auto Show, BYD's FangchengBao brand and its first mass-produced model, Leopard 5, were showcased. Fangcheng Leopard focuses on the 600,000 to 800,000 yuan specialised personalised market, a key layout for BYD's comprehensive coverage from household to luxury segments. Leopard 5's pre-sale price range of 300,000 to 400,000 yuan differs from the earlier disclosed 400,000 to 600,000 yuan due to various factors.

Horizon Insights

Closer to Chinese Markets

Horizon recently met with investors and exchanged views on China consumer trends. The primary focus of this analysis revolves around Chinese brands "domestic substitution strategy". This strategic approach adopted by local brands involves a calculated penetration into diverse consumer sectors within China, with the exception of luxury markets. Noteworthy achievements by certain companies across various sectors, such as Luckin Coffee, Gambol Pet, Miniso, Anjoy Food, Flyco, etc. These companies have effectively tapped into the lower-tier markets, offering cost-effective products in areas that international brands tend to overlook. Following the acquisition of substantial market shares and the establishment of brand recognition, these local companies subsequently enhance their product offerings and services, thereby cementing their competitive stance.

Trivium China

A health kick

Premier Li Qiang approved two new plans for the healthcare sector in the State Council executive meeting. An Action Plan for the High-quality Development of the Pharmaceutical Industry. An Action Plan for the High-quality Development of the Medical Equipment Industry. The meeting readout tells us the plans aim to enhance domestic innovation, support key enterprises, safeguard traditional Chinese medicine, and develop skilled professionals. This is odd as Policymakers already outlined three 14th Five-Year Plans covering the pharmaceutical, just a couple years back. So what's the deal? Likely, due to 2.5 years fighting COVID-19 there is little time for health regulators to achieve five-year goals.

AceCamp International

Xiaomi's AI model is mainly committed to the model of lightweight parameters, and mainly serves the needs of the Xiaomi Group and internal companies, while in the field of mobile phones, IoT products and automobiles will pay more attention to the way of offline end deployment. At present, millet has carried out internal testing of some large models on the voice assistant on the mobile phone side, and carried out internal testing of some customers in some application scenarios, but has not yet carried out large-scale public testing. It is expected that there will be some differences in the size of the number of parameters of the model deployed by each mobile phone factory on the mobile phone side, but in practice, due to the existence of hardware limitations, the gap between the number of parameter sizes may not be very large.

Smart Insider

Jianfeng Liu (Senior Officer) purchased US$272,000 worth of stock on Aug 28th at HKD 62.85. This is his first purchase and a reversal from a timely sale of $88,000 just two months ago at HKD 103. It is unusual for insiders not only to make such a quick reversal but also to spend more buying the shares than what they received in a sale. Yusuo Wang (Chair) purchased 1.5m shares on Aug 26th at HKD 65.54, spending $12.8m and increasing his holdings to 370.7m shares. This is also a reversal for Wang, who made timely sales in 2021 at prices >HKD 121, and last bought in Mar 2020 at HKD 65, which also proved very timely. The stock has had a sharp recent decline, yet these are two interesting purchases and reversals.

Macro Research

Developed Markets

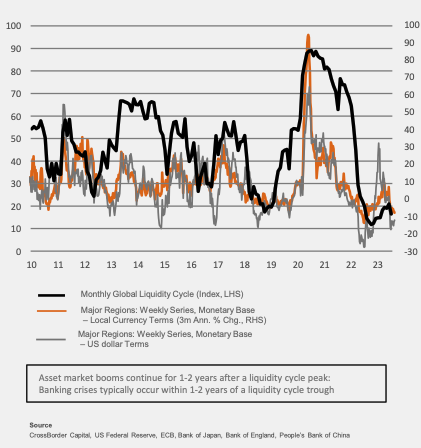

CrossBorder Capital

Global liquidity conditions under pressure from volatile collateral values

Michael Howell examines global liquidity conditions which are under pressure from volatile collateral values and generally restrained Central Banks. Latest data show Fed liquidity edging lower, shrinking -7.7% to $5.39trn. The exception is the People’s Bank of China, which has been increasing liquidity supply, and the Bank of Japan, which has seen liquidity remain flat over the last three months. Michael ‘s risk appetite indicators show that, so far, global risk markets are holding up, but bonds – the bedrock of collateral – are volatile and are undermining liquidity conditions. We are in choppy waters!

Longview Economics

Is the wave 2 relief rally now played out?

Risk on was the theme in markets earlier this week, with the S&P500 rallying sharply and pushing through its 50-day MA. Strength came from the tech/long duration growth area of the market as the megacap tech stocks shrugged off their recent poor price action. With that, S&P500 futures are now just shy of Chris Watling’s stop loss level. With the recent strength, many of Chris’s models have increasingly moved towards SELL. It is clear that markets are at a key juncture, raising the question of whether this is a relief rally that is about to find resistance, or are markets back in a bullish uptrend? For now, Chris recommends remaining staying 1/3rd SHORT S&P500 September futures, keeping the stop loss 3% above entry level (i.e. 4,517.25).

View from the Peak

September blues

The solution for September is to be defensive, claims Paul Krake, but do so within your current strategy's context. If you like owning risky assets because you believe the Fed is at the end of its tightening cycle, stay long but own a few puts to hedge the September drawdown. If you are like Paul and believe that the current yield environment remains compelling, own more two-year bonds over the next month, a little less USDJPY, and a little less credit. The key is to be agile enough to lift these hedges as we head into Q4. If the data hasn’t deteriorated, investors should expect prices to rebound aggressively. Focus on US and UK two-year notes, and Australian three-year bank bills.

Eurointelligence

Europe needs to rethink Africa

The latest coup d’état in Gabon is part of a growing number of military coups in Africa in recent years. This has implications for Europe. First and foremost is a question of responsibility due to the continent’s colonial history and the many links Africa has with European nations. There’s also the growing impact of climate change, a result of Western industrialisation. The coup, along with other possible ones, may impact its supply chains to Europe, including uranium exports being put into doubt due to Niger’s recent coup. Whether threats of disruption of raw material exports come to the fore is not yet known, but it’s clear that the EU needs a strategic rethink on Africa.

AAS Economics

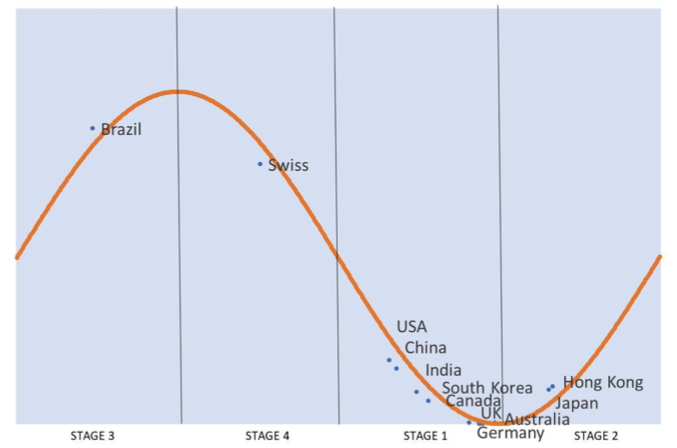

Australia edges up into stage 2

The only changes in the business cycle for the upcoming month is Australia, which now edges into Stage 2 of the cycle (see chart), denoting a more beneficial environment for equities in general. Historically, sectors which perform well in this stage include consumer discretionary, energy, technology, basic materials and industrials. Only Japan, Hong Kong and Brazil feature in a stage conducive to equities, with the remaining countries in the most defensive stage other than Switzerland, which moves into amber territory.

Global Macro Investor

The Everything Code

The Everything Code purports to be able to forecast debasement into the future, which in turn allows Raoul Pal to forecast asset prices. He suggests we are about to see a very rapid expansion in liquidity, which is already driving asset prices. Explaining his thoughts in his latest report, he explains how we should see it play out in Q4 and, if the Everything Code proves to be correct, the period of 2023-2026 will witness one of the most dramatic rises in asset prices ever seen, driven by debasement compounding the secular trends of crypto and technology. We will see the likes of Bitcoin and Ethereum soar. Raoul also dives into the use of AI in the healthcare and pharmacology industry, with staggering implications for humanity.

Emerging Markets

Topdown Charts

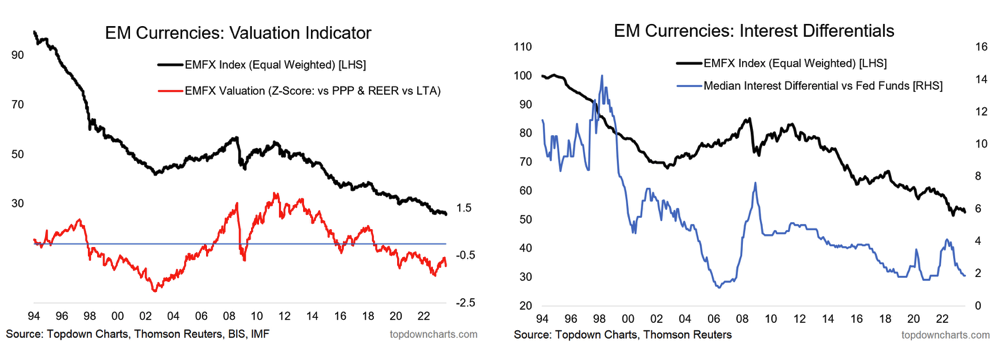

EMFX: Some cause for optimism, but with due caution

EMFX broke down to new lows, mostly thanks to Argentina, but with relatively broad weakness also. But an initial base has been found, and Callum Thomas’s short-term breadth indicators are ticking up from oversold levels. Medium/longer-term signals present cause for optimism. Macro is also somewhat supportive in that EM inflation came down quicker vs US, yet the longer-term technicals still show entrenched downtrend, and longer-term breadth rolling over again. So, to have higher bullish conviction on EMFX, the long-term technicals turnaround is needed. In terms of the USD the overall outlook remains bearish, so the case for EMFX does have promise.

PRC Macro

China: Inflection point

William Hess comments on how the Q2 Politburo meeting marked a policy inflection point, as Beijing’s stance shifted from emphasis on deleveraging to reflation. There will be a natural lag between this shifting stance and a reversal to economic fundamentals, namely manufacturing restocking. However, leading indicators continue to point to late Q3 or early Q4 as the inflation point for the manufacturing inventory cycle. Unlike previous cycles driven by land sales and housing new starts, this one will be supported by the domestic energy transition and demand for durable goods. William believes the beginning of the cycle will confirm a trend reversal for the RMB exchange rate and even A-shares. Expect USD/CNY to return to the 6.9-7 threshold by 2023’s end, and a 20% rebound in A-shares over the next 12 months.

Alberdi Partners

Argentina: Inflationary surges

Food inflation increased 10% after the August 13th PASO, boosted by a sharp rise in meat prices. Several categories, such as home equipment and clothing, also saw a surge following the depreciation of the parallel FX seen after the devaluation. Marcos Buscaglia thus expects core inflation to show a high reading as well. Overall, he expects a sharp rise in headline CPI, above 10% m.o.m in August. Given that the high price shock took place in the second half of the month, he expects it to have a high carry for September, in which inflation will see double digits even if the government keeps the peso at 350. Marcos raises his 2023 inflation forecast from 160% to 182%, in the best case scenario.

IndiaDataHub

India: Coverage of the mutual funds sector

IndiaDataHub’s extensive coverage has now expanded to include their latest dashboard, covering the mutual funds sector. Their dashboards include one that covers the debt market, tracking issuances in the bond, CP and CD market across different sectors; another that covers foreign trade, providing detailed trends in India’s foreign state across over 100 categories and over three dozen countries; and one providing granular data on mutual funds, tracking all key trends from monthly flows across fund categories to composition of AUM across categories, as well as investor type, region and distributor type. Contact us to find out more.

Greenmantle

Mexico’s nearshoring opportunity

Niall Ferguson has discussed Mexico’s strategic positioning in the context of the new Cold War since the Greenmantle Research 2017 Gathering. That is now consensus, and the opportunity is materializing. Foreign direct investment is surging into Mexico. In the first half of 2023, the volume of FDI jumped 41% y-o-y to $29BN, twice as much as the average of the past 15 years, the boom driven by manufacturers diversifying away from China and by new incentives to invest in North America. In addition to industrial real estate, manufacturing, transportation, and financial services have benefited the most. Niall expects these trends to continue, boosted by a relatively benign macroeconomic context for Mexico and a presidential election that will most likely yield a more pro-market president than AMLO.

Emerging Advisors Group

Crunch time looms nearer in South Africa

The public debt ratio is spiralling upwards again, making the country a sharp outlier in the global economy. Jonathan Anderson explains that, as before, this is not a fiscal problem, but rather a central bank problem; rather than using QE support to control funding interest rates, the bank has a bizarrely orthodox stance which is driving the debt ratio through the roof in a uniquely idiosyncratic way. Jonathan expects the situation to the resolved via monetary policy, but he no longer sees the trade as the worsening external balance has brought ZAR risks to the fore and pushed him out of the local fixed income market.

Copley Fund Research

The decline in Turkish investor positioning

Ownership levels in Turkish equities have fallen to new lows among active EM equity funds. The percentage of funds invested in Turkey stands at an all-time low of 31.45%, pushing average holding weights down to just 0.38%. For the first time since 2008, active managers are now running an underweight in Turkey, with just 18.6% of funds positioned ahead of the iShares MSCI Emerging Markets ETF. With both active weights and benchmark weights so small, the risks of not holding a Turkey position are diminishing for the average active manager. Only 16 of the 373 funds in Copley Fund Research’s analysis hold more than a 2% allocation – to bet big on Turkey here is a significant non-consensus call.

ESG

The Political Forum

Is ESG on its last legs?

The remarkable drop in support by BlackRock for ESG proxy proposals clearly shows that ESG is dying a fast and ignominious death… or is it? Stephen Soukup disagrees, illustrating three key reasons why. First, many don’t realise is that ESG isn’t a proxy voting strategy, it’s an engagement strategy, one designed to cultivate sustainable business plans over the long-term. Second, many high-profile advocates of ESG have found that sometimes it’s easier to let government lead the fight and draw heavy fire from opponents. And third, ESG is a tactic that facilitates shareholder activism and maximises investors’ emotional fulfilment. ESG is going underground a little, but it ain’t dying.

Verisk Maplecroft

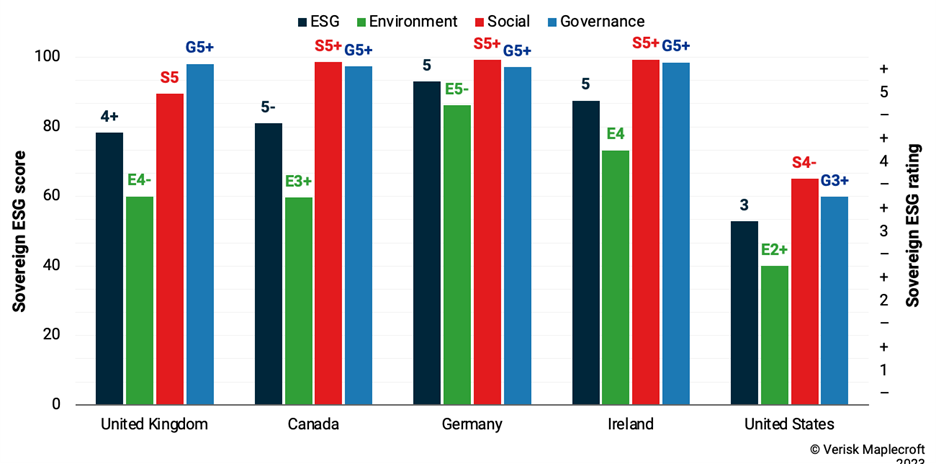

UK sovereign ESG ratings downgrade

The UKs deteriorating performance across a swathe of the Maplecroft’s macroeconomic and sovereign ESG indices has significant implications for the business and investment community. In the last 12 months, the UK’s score dropped 7 points to 78/100, with significant drops in the E and S pillars. It is clear that the UK is simply no longer keeping up with its peers and near-neighbours, with the exception of the US (see chart). The team cite deteriorations in human and labour rights dimensions as reasons for an ailing social score, and declining index scores for environmental regulatory framework, deforestation and waste generation for a poor environment score, with the latter listed as an extreme risk. As one of the leading G7 economies meant to be leading by example post COP26, it’s hardly a good look.

Sustainable Market Strategies

Banking on impact

Despite recent progress, the Sustainable Market Strategies team say there is still room to improve financial inclusion to reduce economic inequalities. It can be a challenging feat to invest in companies who promote financial inclusion, as the most impactful can be accessed in emerging and frontier markets (EMs/FMs). However, companies offering transfer payment services – especially those who are cutting costs associated to FX international transfers – could be considered an impactful way to support financial inclusion in DMs, EMs and FMs. ESG investors should also consider banks with specific outreach programs in EMs/FMs such as microfinance business streams and mobile phone companies that facilitate the availability of their services via digital platforms, due to their contribution in elevating people out of poverty.

Commodities

Metals Focus

Will current momentum in Chinese gold jewellery demand continue?

The Metals Focus team forecasts ongoing and modest growth in Chinese gold jewellery consumption during H2/2023, delivering a 13% rise for 2023. On the one hand, consumption in H2/2022 was relatively low, because of the severe impact of COVID-related regulations in Q3/2022 and the infection peak in Q4/2022. On the other hand, their view that gold prices will weaken during the rest of 2023 will also lend some support to demand. The chief upside risk centres on how lower gold prices stimulate bargain hunting for jewellery, especially those with quasi- investment qualities. On the downside, the lacklustre Chinese economy and deteriorating consumer sentiment may further undermine domestic sales.

Stray Reflections

Bitcoin: Everyone loves a comeback

Despite frozen withdrawals, hedge fund drama and regulatory shutdowns, Bitcoin has returned to its pre-TerraLuna collapse glory. How can this be possible amidst the bankruptcies and lawsuits? Bad news that fails to send prices lower can be interpreted as a bullish sign, and if the news turns positive… Similar to how Glencore’s IPO in 2011 signalled the end of the commodities supercycle, Coinbase’s heralded the top in digital assets. Only thing is, Glencore regained its IPO price last year, and Coinbase stock is up 154% this year. Bitcoin’s volatility is historically low and the Bollinger Bands are the tightest on record, which happens before a strong trending move. Brace yourself.

CPM Group

What you need to know about Comex open interest and inventory

In his latest video, CPM Group’s Jeffrey Christian discusses the change in silver Comex open interest in July and August, and whether it will have any effect on the price of silver. He also discusses the 14.2 million ounce of silver that was moved from Comex eligible to registered within the JP Morgan depository. Jeff concludes the presentation by discussing CPM Group’s short-term gold and silver forecasts heading into September.

Click here to watch.