Company & Sector Research

Europe

The Edge

Special Situations: 10 stocks poised for long-term growth

The companies highlighted in The Edge's latest report are all undervalued vs. their industry peers, while exhibiting strong fundamentals, including impressive profit margins and strategic leverage. European and US names include: 1) Melrose - divesture of its Aerospace division looks set to unlock considerable value for investors. 2) Solvay - the share price has rerated sharply higher following the successful spin-off of Syensqo earlier this month. 3) BorgWarner - ICE to EV opportunity. 4) MDU Resources - the next big utility play; activist involvement. Click on the button below for further information on how to capitalise on these and more spin-off opportunities.

New Street Research

Telecoms: Happier times ahead

After many years of headwinds, New Street is bullish on the outlook for the European telecoms sector as we head into 2024, with a continued reduction in risk perception helping to support a multiple re-rating driven by the following themes: 1) Ongoing regulatory tailwinds, 2) Declining energy costs, 3) Capex going past its peak driving above inflation OpFCF growth, 4) Copper shutdown, 5) Further sector consolidation. Their top picks are BT, Deutsche Telekom, Telefonica, Telenor, Telia and Vodafone.

Willis Welby

Consumer Discretionary / Industrials

Willis Welby looks at UK growth names (>$2.5bn M/Cap) that have not shared in the share price rises since Oct 26th. CPG has seen analyst downgrades despite a robust update during Nov, but looks like a very strong compounding story that is not expensive and makes great sense at current prices. However, it is BAE that really stands out. The defence contractor has seen upgrades to consensus Y2 EBIT over the last three months and more recently has announced more good news on orders. Relative to US peers that implied to Y3 EBITM ratio of <60 looks way too low. Other stocks discussed in their report include AstraZeneca and Games Workshop.

ROCGA Research

ROCGA’s Cash Flow Returns On Investments based DCF valuation platform shows BAYN to be undervalued for the first time in 10 years. BAYN is not a quality company and would not warrant attention, but the valuation gap is compelling with potentially 50% upside. With a few clicks, you can model and value one of 2000 companies across Europe and the US. Other companies that appear on their list of undervalued companies are Ahold, Associated British Foods and Saint-Gobain. A free consultation and trial can be arranged on request.

Iron Blue Financials

Iron Blue initiates coverage with a score of 29/60, which is top quartile (fertile ground for shorting). They highlight elevated use of provisions accounting (22% of FY22 PBT adj) and increased factoring of receivables (DKK1.3bn, up from FY21’s DKK1.1bn). FY22 profits benefitted from DKK122m Covid-19 grants and DKK15m net bad debtor provision release. Iron Blue also notes an unusual organic growth calculation methodology. Regarding governance, they flag overboarding by the Chair (9 other board positions), internal succession of both CEO and CFO, Audit & Risk Committee composition out of line with best practice, and above average non-audit payments to EY. In Iron Blue's report, they discuss a range of areas where disclosure could be improved.

DayByDay

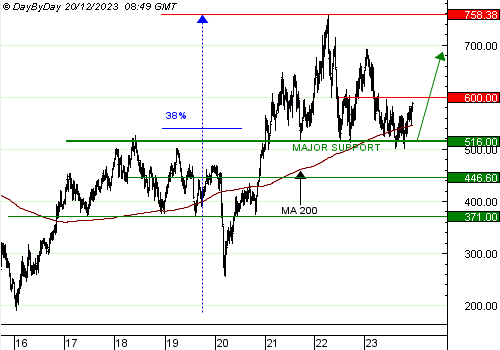

Basic Resources set to hit new highs

The Basic Resources sector formed a head-and-shoulders or rounding top above its key support, between 2021 and 2023 (see STXE600 Weekly chart above). That major support at 500/516 is the area of the 38% Fibonacci level, with several peaks and troughs. As that neckline has not been broken, the trend remains bullish. In 2024, the sector should reach new highs above 760.

North America

Radio Free Mobile

The Metaverse: A year to forget

A rotten year for The Metaverse which has one more gift to give with the cancellation of ByteDance’s Pico 5 headset, one of the most popular devices for developers. Cancellations like this and a market that halves will only serve to delay the take-off of The Metaverse as well as slow the development of the ecosystem around it. While the release of the Apple Vision Pro in 2024 could trigger renewed interest, Richard Windsor believes the segment remains uninvestable at the moment. He is keeping tabs on Roblox and Unity, but both companies are too expensive and their shares look set to stagnate / decline for a while yet.

Global Equity Research

META shares have had an incredible run this year driven by a stabilisation in margins, a depressed multiple and negative sentiment. However, Rickin Thakrar recommends taking profits given his 1) DCF valuation has the company priced for perfection. 2) Two-year growth rates remain sluggish (a sequential improvement in MAU and DAU has been driven by easy comps). 3) Mark Zuckerberg has been selling shares for the first time in a couple of years. Rickin believe the shares could once again retest the $270 level (20%+ downside).

Hedgeye

One of the most boring stocks in Brian McGough’s universe has suddenly become one of the most interesting! After Glenn Chamandy’s ousting as CEO, several shareholders have stated publicly that they want him reinstated. Brian provides his take on the leadership change and what it means for the bull case. With consumer and corporate macro pressure, GIL’s cost advantage presents an opportunity to accelerate share gains. Brian's EPS forecasts of $3.50 for 2024E and $4.22 for 2025E are significantly ahead of consensus. He thinks the share price can double in two years.

Verbatim Advisory Group

Better high growth stores, convenience and popular deals boost Nov comps. Verbatim's latest channel checks reveal high-end luxury brands including The Ordinary, e.l.f. Cosmetics, Benefit Cosmetics and Tarte Cosmetics have been the top sellers. Inventory levels are just right, however one of Verbatim’s sample respondents reported shortages in brands such as Lancome, Murad and COSRX. Prices across their sample are rising at an average of $2 and mostly on fragrances. Hiring new employees is easier due to the increasing wages and applicant interest. Labour hours are consistent Y/Y. Online ordering is increasingly popular as stores fulfil 20 orders a day on average. Verbatim’s Nov Comp Estimate is +5.3% vs. 3Q23 (Aug-Oct) Actual Comp of +4.5%.

Quo Vadis Capital

Which unit growth stories can be bought at a discount?

Consumer Discretionary / Staples

John Zolidis reviewed 18 unit growth stories in the consumer space, breaking out the value of the existing business from the implied value of the growth option. He then calculated the value of future unit growth using a store level DCF. He compared the implied value of the growth option in the first exercise to expected value creation from store growth in the second. From this John solved for where the market was paying the largest premium to the value of future growth and where growth could be purchased at a discount. The most interesting names on the long side were Academy Sports & Outdoors, Luckin Coffee and Yum China. Sprouts Farmers Market still looks very cheap even after +50% move YTD. Investors are paying the biggest premium for Dollarama, Chipotle and Dollar Tree.

Huber Research Partners

Moving in the right direction - Craig Huber points to improved pricing, better client retention and DNB's success in dealing with headwinds from underperforming legacy businesses. He has increased confidence in management achieving their medium-term organic ex-FX revenue growth target of 5-7% by 2026 (at the latest and likely could be sooner) and believes the current valuation (DNB trades at 9.7x/8.5x 2024/25(E) adjusted EPS or 9.6x/9.1x EBITDA) is too steep of a discount to other information service companies. Craig sees great risk-reward at these levels (>40% upside vs. 15% downside) and upgrades the stock to Buy.

Two Rivers Analytics

Declining reimbursement rates coupled with rising expenses looks set to weigh on margins - earnings shortfalls should cause investors to rethink RDNT’s AI-inflated multiples. Medical imaging, notably core MRI reimbursement rates, are declining at CAGRs of 5-6%. All major operating expenses are rising, competition is increasing and capex requirements are high and ongoing. RDNT is also highly levered (5.5x trailing EBITDA). The stock is up >90% YTD and trades at nearly all-time high EV/Sales, EV/EBITDA and earnings multiples. Historically, it traded at a 40-50% EBITDA multiple discount to competitors, now it trades on par with them.

Sidoti & Company

The street has been overly focused on spread normalisation and glossed over WIRE’s roughly half-billion dollars in capital reinvestment made to widen its service “moat” vs. competitors. With copper spreads close to “normal” levels, Sidoti sees the stock’s narrative shifting to WIRE’s multiple secular tailwinds, the looming supply shortage of its raw material (a positive for the company) and its best-in-class service model. WIRE trades at 9.7x Sidoti’s 2025 EPS estimate and the balance sheet remains pristine (debt free; $582m in cash - expected to increase to $994m by the close of 2025).

Thompson Research Group

TRG’s latest report looks to address the following 3 questions: 1) Is non-res construction going to cycle down? 2) Is HRI over-earning, given the meaningful growth since 2019? 3) Should the group reduce leverage and internal investment to generate FCF? TRG believes HRI is in the sweet spot operationally and for investors, as they are a top-3 player with scale advantages, but relatively small at 4% market share. This allows the company to make bolt-on acquisitions that, at this size, move the needle yet carry minimal operating and financial risk. The stock is up meaningfully on a 3-yr and 5-yr basis but is early in its maturation process. HRI remains a top pick for TRG heading into 2024.

Cerundolo Investment Research

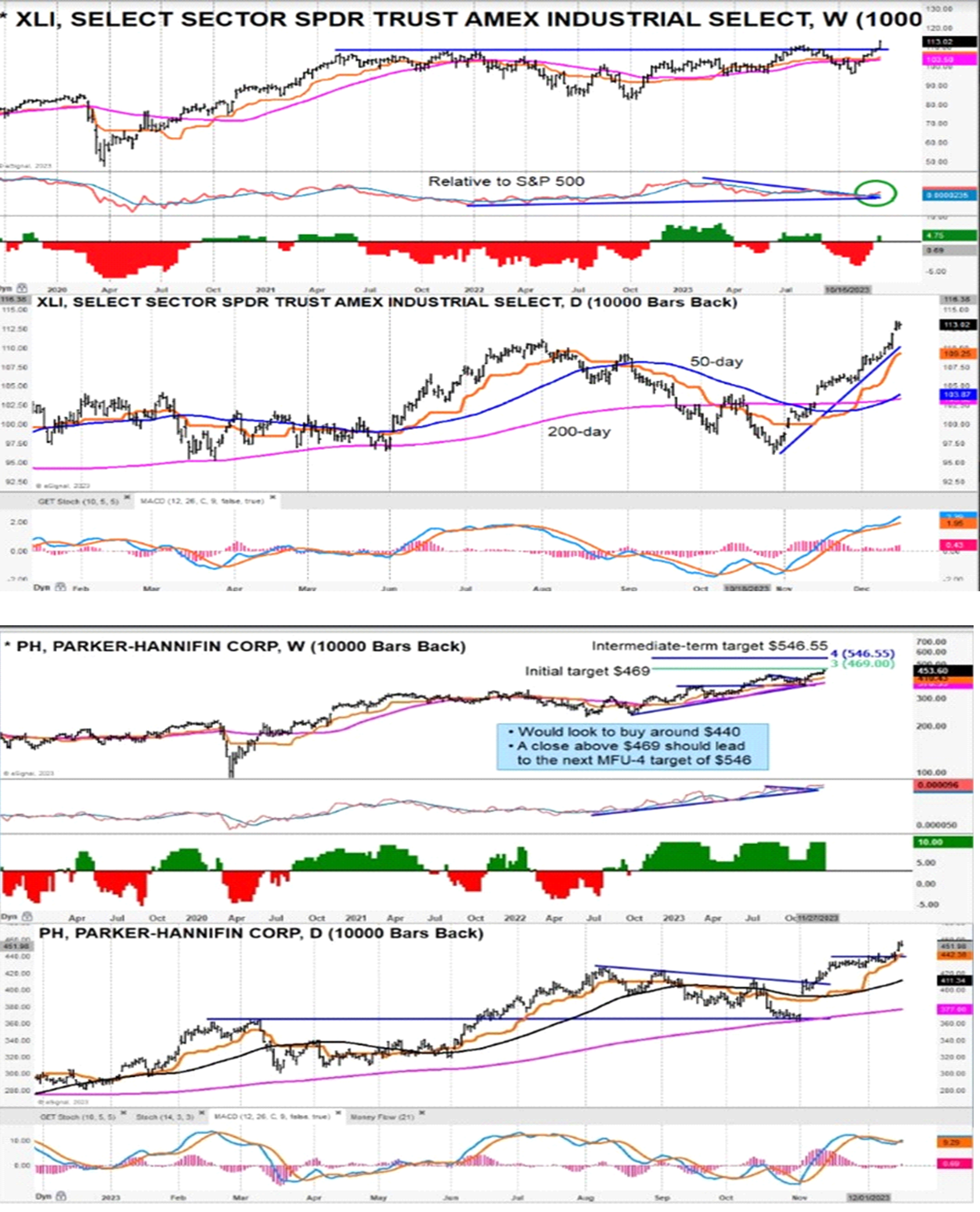

Long ideas in Industrials

The XLI had a strong close last week as it made a new all-time high. Guy Cerundolo has scored and ranked the sector and come up with a basket of long ideas. The highest ranked stocks include Parker-Hannifin (see chart), Copart, Eaton, Grainger, ITT and Trane Technologies.

BWS Financial

Management has brought back the goal of achieving double digit operating margin after three years of underperformance while turning the business around. Unlike prior years where NTGR was relying on unit volume growth to drive operating leverage, it now has a growing base of subscription revenue that is contributing to earnings. The forthcoming upgrade cycle along with improvements in FCF should revalue NTGR's stock towards Hamed Khorsand’s TP of $30 over the next twelve months (>100% upside).

Japan

Galliano's Financials Research

JPX is Victor Galliano’s 2024 high conviction buy amongst the global exchanges, for its attractive valuations, as well as its potential for increased market activity and big data revenue growth. He believes that JPX is the exception to the rule that DM exchanges need to diversify their revenue bases, as it is under less de-regulatory pressure. Victor sticks with Hong Kong Exchange as his deep value pick, as well as Deutsche Boerse, but remains negative on Coinbase (he thinks we are close to exhausting the positive surprises and the fundamentals remain challenging).

Emerging Markets

AlphaMena

Over the last couple of years, Etisalat has seen its share price erase nearly all the gains made following an impressive surge in 2021, but does the sell-off provide an opportunity for investors? AlphaMena doesn’t think so. Global inflationary pressures with double-digit inflation rates in Egypt and Pakistan are hampering the group’s revenue and margins. Peer valuation methods are also still bearish. The stock trades at 7.4x 2024 EV/EBITDA and 16.6x P/E (vs. 5.9x and 13.2x for its MENA peers). AlphaMena prefers to bet on more attractive telecom operators, which offer higher dividend yields (Zain, Vodafone Qatar and STC), especially in times of uncertainty.

Blue Lotus Research Institute

Blue Lotus reinitiates coverage of the stock with a Sell rating as they expect domestic travel growth to slow down in 2024 and assumptions on Chinese outbound travel demand need to be reassessed. They see rising competition in the domestic travel market from Meituan and Tongcheng Travel in the short haul segment as well as share gains made by economy hotels encroaching TCOM’s commission base. While TCOM was quick in launching Large Language Model (LLM) for travel planning, Blue Lotus believes it lacks sufficient data and the advent of AIGC will simplify travel booking which works to TCOM’s disfavour.

Primaresearch

SPP’s problematic implementation of its ERP system has significantly impacted the business, causing lost sales of R1.6bn and foregoing trading profit of R720m in FY23. Shamil Ismail is concerned that there may be longer-term consequences from this episode. Channel checks with store owners suggest SPP will be under increased pressure to sharpen its pricing to maintain loyalty levels, which could impact margins. He also sees challenges in offloading the Polish business, additional impairments from recent acquisitions in Ireland, refinancing risks in Mar 24 and has concerns regarding the company's new board.

Smart Insider

Chumpol Nalamlieng (Director since 1992) sells 60,000 shares at THB 290.50, reducing his holdings by -60%. Smart Insider ranked the stock -N on 23rd Aug based on sales he made at THB 314. Since then, Nalamlieng has continued to sell shares and this most recent one is his largest and at the lowest price. This year, he has reduced his holdings from 201,000 shares to 41,000 shares. Nalamlieng's sales do not appear to be a strong endorsement of Thammasak Sethaudom (currently EVP, formerly CFO) who will be taking over as CEO in Jan 2024. Smart Insider has downgraded the stock further, from -N to -1 (lowest rating).

Macro Research

Developed Markets

CrossBorder Capital

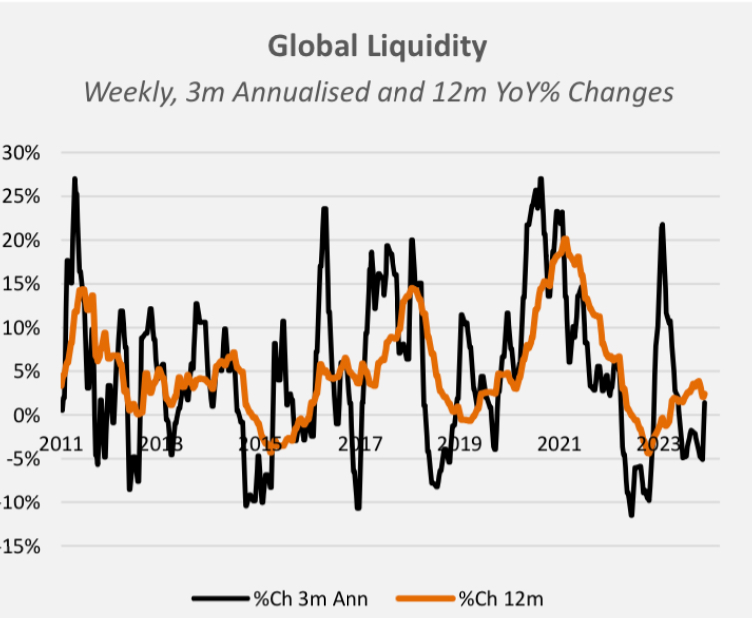

Global liquidity growth accelerates

Michael Howell remarks that the two factors driving liquidity – collateral values and Central Bank injections – are moving in the right direction, albeit with the odd setback here and there. Collateral volatility has picked up again; collateral values are affected by Central Bank actions. Fed liquidity has jumped higher and the PBoC continues to inject much needed liquidity into money markets, but other Central Banks need to step up too. Encouragingly, every new data release adds weight to Michael’s view that QT de facto ended in October 2022. Expect liquidity levels to continue rising before peaking in late 2025. All-in-all, global liquidity levels are akin to those recorded in March when the Fed stepped in after the SVB crisis.

Steno Research

UK CPI: A deflationary shock?

Andreas Steno correctly estimated headline CPI figures to be well below consensus, making clear that the path to 2% is much more doable than many realise. Not only were the base effects of the data huge, but services inflation is also historically soft at this time of year and Andreas could see it even turning deflationary. He recently entered a LONG UK duration trade which so far has been a winning trade. He also comments on market belief that the BoE is expected to outhawk the Fed over the next 12 months, a complete mispricing given current price trends in both countries.

Eurointelligence

What does Orbán want?

The EU woke up to a Hungarian veto on the Commission’s plan for a €50bn aid package to Ukraine, and another veto to the budget compromise. Given Orbán’s meetings with Republican leaders in Washington to urge their opposition to Ukraine aid, Wolfgang Munchau believes he wants to cut the western lifeline for Ukraine, forcing Zelensky into cutting a deal with Putin. EU member states can organise the aid on a bilateral basis, but this will not be easy. The historic day for the EU will come when it finds a way to exist in this newly fragmented world and is able to assert its own interests, without dependence on the US or anyone else for its welfare and security. This day has yet to come.

RW Advisory

US: S&P500 Fly me to the moon & back

S&P500’s blow-off rally +16% net, largest in 30-years, but pressured into all-time high at 4820, near 5k roundaphobia. This serves as a behavioural inflection point, following the dovish “Fed pivot” climax 2-stage reaction, weighed by a triple whammy confluence of momentum, sentiment, and rotation fragility. Healthy mean-reversion unwind expected from +3STD, amplified by record short covering and the yearend (SCR) seasonality lift which included a dash-for-trash YTD laggards, notably small-cap and lower quality stocks. Historical macro analogues signal underperformance of both economically sensitive sectors into late-cycle slowdown, under introduction of rate cuts. Tactical vol-explosion risk, marked by high-frequency vol proxies and FSC model price-time divergence into Q1 2024.

Minack Advisors

US: The 2023 rally limits the 2024 upside

2023 started amidst widespread fear of a hard landing and is ending on a soft landing consensus which Gerard Minack warns skews the likely outcome for markets in 2024. If the US does achieve a soft landing, risk asset returns will be positive but mediocre. Many of the returns have been brought forward already, with valuations quite high compared to prior cycles and EPS growth due to fall, and the scope for a valuation-boosting drop in long-end Treasury yields is probably limited. No market is pricing in a hard landing, but Gerard sees a 50% chance of recession and advises investors to start the year cautious.

GFC Economics

Fed Pivots

With three rate cuts projected for 2024, GFC Economics comments on how the Fed is signalling that it is prepared to run the economy hot. The Fed pivot will be seen by some as a deeply political move to inflate the economy in the run up to the election. Whatever the merits of this argument, the Fed has signalled its intentions: it will be cutting rates into an economy that is strengthening. It’s quite hard to see how this will be positive for long bonds – fiscal policy is far too loose and there is little control over spending. The tight labour market should embed services inflation as the Fed eases. Term premia should rise and the treasury curve should be positively sloped. The sweet spot for the equity market is now, and possibly the next few months.

Stray Reflections

US: When doves get shot

Jawad Mian warns investors to brace themselves for two surprises in 2024. First, he thinks that the Fed will catch markets off guard by swiftly reducing interest rates in the first quarter, possibly by 50 basis points by March. Second, the Fed will deliver less relief than markets expect over the entire year. Consequently, markets will grapple with the impact of pricing out the majority of the six anticipated rate cuts. Why it matters: don’t ignore the former and focus on the latter. Sequencing matters. The rate cuts are bullish for risk assets in the near term. Jawad expects a continuation of recent trends - stocks higher, bond yields and dollar lower.

Rosenberg Research

Japan: Abe’s legacy lives on

David Rosenberg explains how Abenomics has been met with meaningful progress, with Japan one of the strongest-performing advanced economies on a per-worker basis. The country still faces major challenges in the form of demographic headwinds, but policies appear to be working and have room to run. Productivity will be a key determinant of prosperity and performance. Cyclical policy has a rare opportunity to normalise – on the monetary side, David anticipates a gradual return to a positively sloped yield curve. He kicks the tires on his bullish Japan call and finds enough structural policy momentum to switch his emphasis from “cyclical outperformer” to emerging “secular success story”. He likes banks and mid-caps. On FX, he expects the carry trade to die in 2024 as interest rate margins compress sustainably, and he is also highly bullish on the yen.

Talking Heads Macro

Japan: Playing an easy BoJ

The Fed’s ‘attack’ on the global central bank peloton has almost certainly played an important role in keeping the BoJ on hold. That keeps the monetary stance very much in line with weak cyclical domestic fundamentals and structural drivers that need encouragement. An easy BoJ allows Manoj Pradhan to stay long the Nikkei (with support from a Yen that doesn’t strengthen too much). Has the BoJ missed its window to hike? For now, Manoj hopes so. He says that there is a fundamentally sound window for the BoJ to tighten, but it will appear when the planned fiscal expansion, capex drive and services inflation are all entrenched. One can only hope the BoJ doesn’t think January or any time soon is the time to go.

Pennock Idea Hub

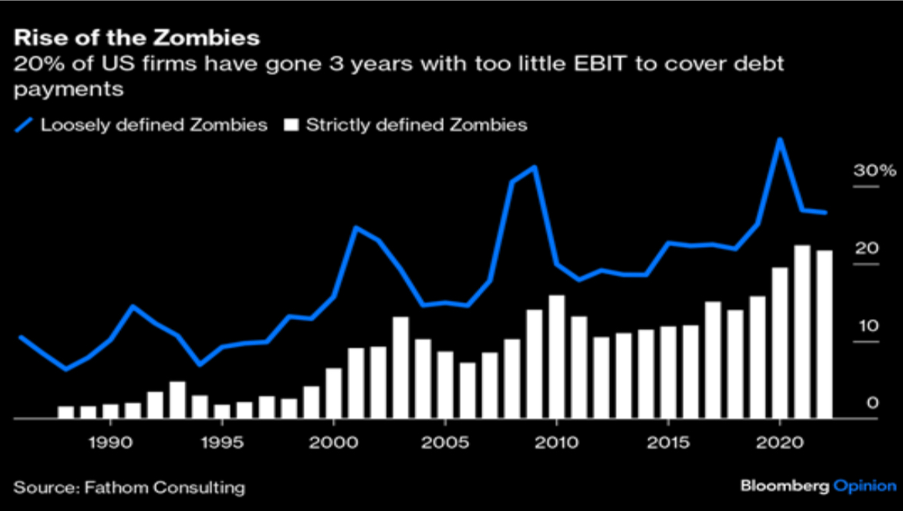

Schumpeter returns

Debt has been Ed Pennock’s main concern throughout 2023, with the structural risks posed by indebtedness threatened by the end of zero interest rate policies (ZIRP). There is a whole generation of investors who have not known a period where interest rates were driven by market forces rather than central banks. It has resulted in a burgeoning of zombie companies who will struggle to cover their interest bills yet have managed to survive in the world of ZIRP. We will see markets return to the days of old, where return of capital becomes a key concern again. Joseph Schumpeter’s concept of creative destruction rises again, heralding the end of zombie companies who continue eking out an existence. WeWork and Sigma are just the start.

AAS Economics

Economic growth causes price decreases, not increases

Some economic commentators are of the view that whenever the economy gains strength it should be the role of the Fed to step in. The AAS Economics team suggest that it makes little sense that genuine economic growth can lead to general price inflation, with the current believe that is does being a result of flawed statistical data derived from an erroneous framework. The subject matter of economic growth is increases in the production of goods and services that individuals require to support their life and wellbeing. It follows that for a given amount of money, all other things being equal, an increase in the quantity of goods results in a decline and not in an increase in the prices of goods and services in general. Hence, one should expect an inverse correlation between changes in the prices of goods and changes in the production of goods, all other things being equal.

Emerging Markets

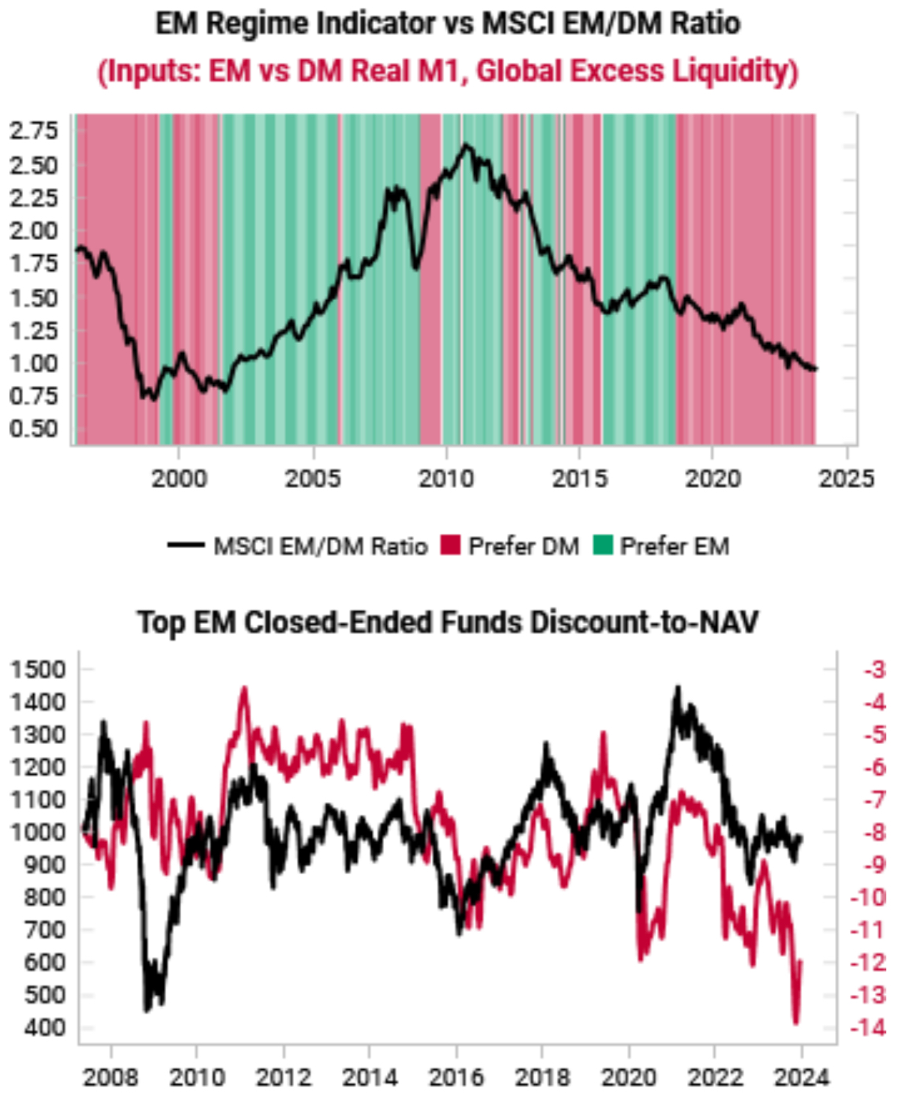

Variant Perception

“A” time to buy EM, not “the” time to buy EM

The Variant Perception team’s EM/DM liquidity regime still prefers DM risk assets over EM (see chart 1). However, some signs of EM dislocation are hard to ignore (chart 2). EM assets do offer tremendous upside once the liquidity cycle improves, but it may not yet be the time to buy. There are some exceptions, with EM bonds standing out as having both high yields and low inflation, underpinning the team’s LONG Brazilian debt thesis going back to 2022. Thailand is also very uncrowded with a positive capital cycle outlook, with the growth outlook improving despite weak YTD Thai equity returns being poor due to weak tourism. Chile is also on their radar – although equities are lagging behind other LatAm countries YTD, the situation is stabilising and there is a positive read across from China or copper upside.

East Asia Econ

China: Credit ratio high, M1 low

In the monetary and credit data for November, there’s no change from recent trends. Given this, the cyclical picture for the economy looks the same. The rise in government borrowing will probably put a floor under growth in the next few months, but there isn’t enough momentum in overall growth to think that the credit impulse is about to lift the economy. Yet despite weak credit growth, the credit ratio continues to creep even higher, now at an estimated 300% of GDP, despite Beijing’s key goal of deleveraging. The pronounced weakness in M1 suggests a continuation of the deflationary momentum into 2024. Having fallen for MoM for 12 of the last 16 months, China is on track to see M1 fall YoY, which would be unprecedented.

Horizon Insights

China: A new phase for the A-share market

In 2023, the market misjudged the benefits of economic reopening. Global and domestic rebalancing alongside post-pandemic disruptions were the reason. In 2024, however, the Horizon Insights team sees greater likelihood of global G2 economic upswing. Despite medium-term downward pressure at home, expansion of China's manufacturing offers a bright light. Impact from the real estate slowdown will diminish further in 2024. The A-share market will enter a new phase because headwinds from market rebalancing due to institutional investor allocation adjustment will come to an end and company profits are set to improve. Therefore, the market's risk appetite on high valuation will simultaneously increase.

Emerging Advisors Group

Is Ghana underestimated?

On external metrics, Ghana is one of the best EM debt stress countries, with low liabilities relative to annual dollar earnings, a good export base and external basic BOP surpluses over the past decade. However, Jonathan Anderson sees it as one of the worst when it comes to domestic metrics, with abysmally low fiscal revenue mobilisation and thus an extremely high ratio of total debt to revenues. Jonathan is impressed with the magnitude of macro adjustment in the near-term, with an easy argument that sovereign dollar yields will be tighter going forward. However, Ghana’s investment case depends crucially on the amount of debt reduction and relief in the external creditor arrangements, and structural progress on increasing the revenue base.

Greenmantle

Mexico’s rail renaissance

In the final months of their six-year term, Mexican presidents traditionally take a step back. But Niall Ferguson comments that outgoing President AMLO is no ordinary leader, having set a new goal for his finale: the return of passenger trains as a major part of the country’s transport system. Ahead of the election he will press forward to complete his big projects, which will be continued by his chosen (and most likely) successor, Claudia Sheinbaum. Yet she is also signalling market positives: fiscal austerity and a new focus on energy transition. In the short term, meanwhile, a cautious central bank and stable macro policy will buffer Mexico from a potential US slowdown and global volatility. Niall’s Mexican outlook therefore remains bullish.

Vermilion Research

Mexico: Signs of further upside

The Vermilion team are upgrading Mexico to Overweight, citing many reasons to be bullish equities into year-end and the beginning of 2024. This includes bullish price patterns and minimal pullbacks on broad global indexes; the continuing lower trend of the USD; European high yield spreads are at 20-month and 9-month narrows; defensive MSCI ACWI sectors remain in YTD downtrends; and US and non-US small caps appear to be putting in RS bottoms. The significance of the risk-on signals cannot be understated, expect upside to continue.

Copley Fund Research

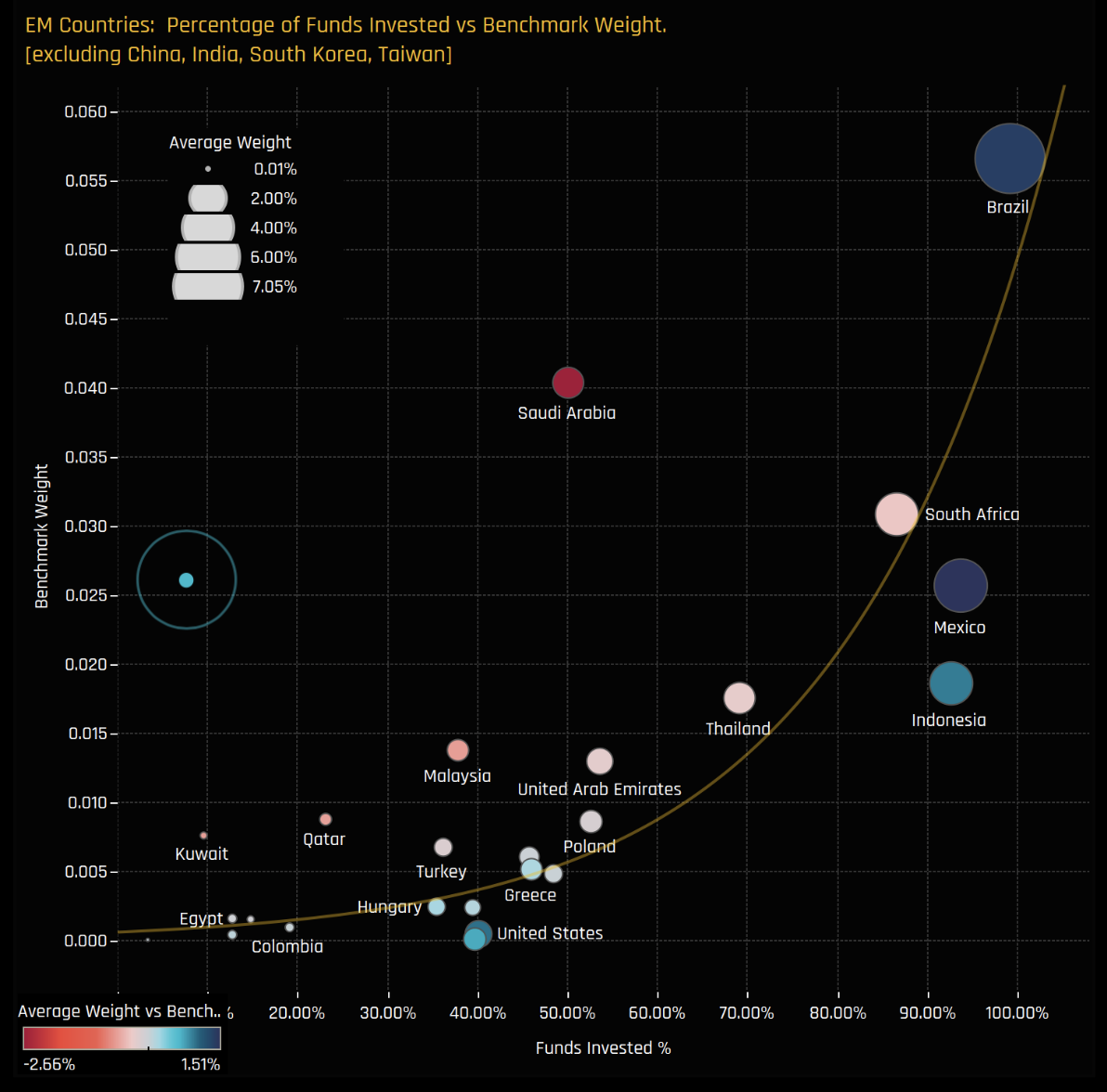

Saudi Arabia: A tipping point in EM equity allocations

Steven Holden’s final report of the year focuses on Saudi Arabia as a key investment allocation among active EM equity funds, reaching the milestone of 50% of funds investing in Saudi for the first time. Fund infows are second-highest after Brazil. Financials lead when it comes to sector exposures, held by 32.6% of funds, followed by energy, communication services and materials. Yet there has been a degree of rotation, with increased exposure to communication services, IT and industrials, and a scaling back in financials and materials. Compared to the country’s counterparts in Asia and LatAm, Steven believes Saudi Arabia to be under-owned, with the nation presenting itself as a remarkable outlier on his chart outlined above.

Krutham (formerly known as Intellidex)

How worried should we be about fiscal dominance in South Africa?

The potential existence of fiscal dominance in South Africa has been of increasing concern. But what is fiscal dominance? Is there evidence of its prevalence? And if so, Peter Attard Montalto asks, is it cause for concern? Peter finds evidence of fiscal dominance in South Africa from Dec 2017 - Sep 2019 and Jun 2022 - Sep 2023. Going forward, Peter says fiscal policy must move first to avert a recurrence of dual policy dominance. “De-risking” should be the guiding principle to reduce long-run interest rates and debt-service costs, with fiscal consolidation as the linchpin and low and stable inflation playing the supporting role. Effectively executed, it can create sufficient leeway for monetary policy to manoeuvre its policy rate unencumbered by fiscal pressures. In contrast, fiscal policy can “passively” stabilise debt as both policies are aligned.

ESG

Sustainable Market Strategies

Bounce back for sustainability

The Sustainable Market Strategies team’s top investment ideas for 2024 for sustainability portfolios are positioned for an economic backdrop whereby the US slides into recession, but accompanying monetary easing is less generous than investors expect. We will see green global industrial stocks outperform US consumer discretionary, with buy now pay later service providers making excellent sustainability SHORT candidates and select oversold infrastructure plays offering excellent value. Nuclear plays and regulated carbon markets are favoured long ideas within the energy transition theme.

Verisk Maplecroft

COP28 treads fine line between action and appeasement

Despite low expectations of COP28, the climate talks in Dubai were bookended with notable achievements. A ‘Loss and Damage’ fund to compensate developing nations for climate change impacts already happening was agreed, and parties rubber-stamped text on transitioning away from fossil fuels within energy systems. However, plenty was left unresolved: the text still leans heavily on transition fuels – effectively gas – is weak on unabated coal and has very little to say on finance. But advances on methane, strong pledges around renewables and a focus on “inefficient” fossil fuel subsidies will give governments and organisations some confidence around mobilising the USD4.5 trillion needed in green investments annually by the early 2030s in order for the world to achieve net zero by 2050.

Commodities

Vanda Insights

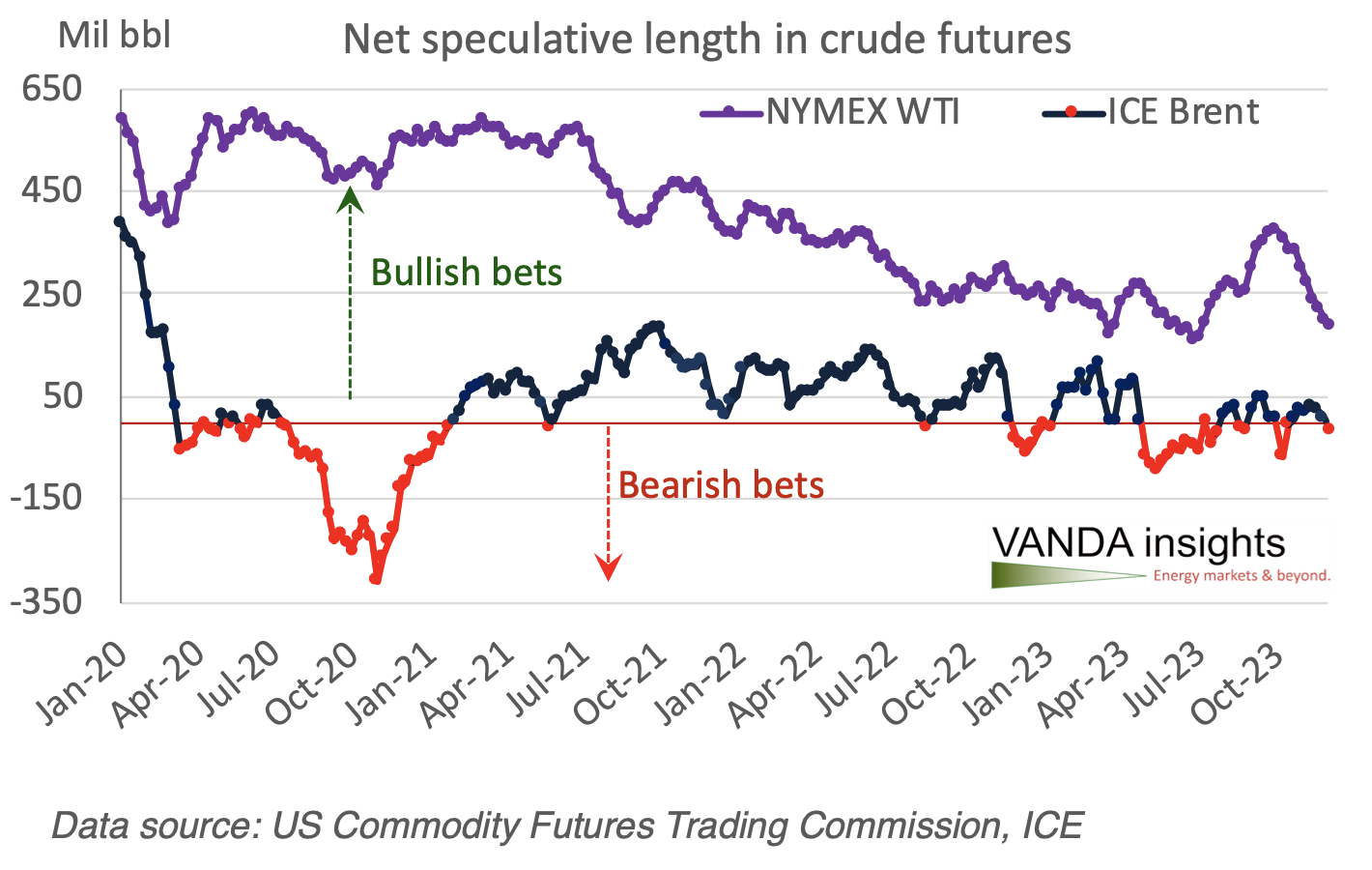

Crude escapes the blues, but don’t bet on a rebound

After the US Fed unexpectedly changed its tune, pencilling in 75 basis points of rate cuts next year, bets on a US economic soft landing came back in full force and overjoyed investors piled into risk assets. Even crude got a shot in the arm from Powell’s remarks, but Vandana Hari remarks that this may not be the early Christmas present from the Fed to the OPEC+ alliance that it may seem. She sees limited runway for crude purely from the latest upturn in risk appetite in the broader financial markets, and remarks that even the most bullish have tempered their views. A bearish view of supply-demand fundamentals going into 2024 has a strong grip on oil sentiment and is unlikely to be pushed aside easily.

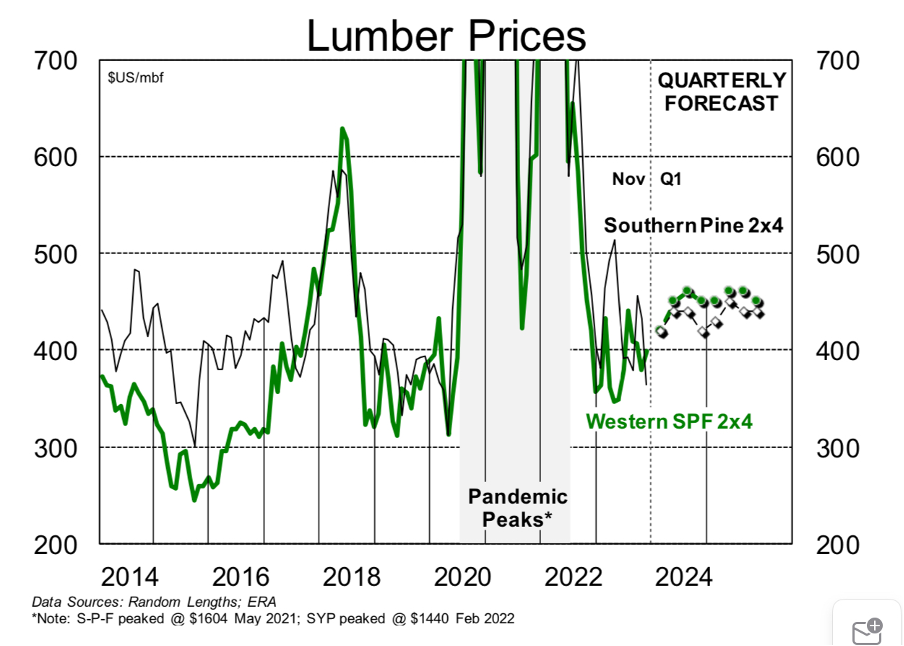

ERA Research

Lumber market making a comeback?

The North American lumber market is sleepwalking toward year-end. SPF 2x4s have been stuck at $408 for three weeks now as a steady trickle of fill-in orders is allowing producers to price defensively. Having been a laggard for much of the quarter, SYP prices are finally moving higher – 2x4s reached $385 on Dec 14th, up from $355 in mid-Nov. As buyers turn their attention to H1/24, the ERA team suspect that “caution” will remain the watchword. Sentiment around US housing prospects for 2024 has turned more positive of late, but do not expect lumber markets to come roaring back to life next quarter.