Company & Sector Research

Europe

Your Weekend Reading

What's so interesting about Auto stocks?

Erik@YWR discusses why we should be investing in Auto stocks - the most undervalued, under owned sector in the market. Auto sales have been depressed for years in the three key global markets (China, US, Europe). This prolonged period of sales below the replacement rate means the average age of cars is at a record high. It's the set-up for a multi-year sales rebound. In addition, the sector is undergoing the biggest technological change in its history. Erik discusses the set-up for OEM’s, but also why auto parts companies and tyre companies can benefit too.

Sandalwood Advisors

BRBY was hit by a slowdown in luxury spending including China one of its key growth markets. In Jan 24 the shares plunged after the company issued a warning to investors about lower-than-expected profits in 4Q24 & FY24. Well ahead of the company’s announcement, Sandalwood published a data-driven report on BRBY (Nov 23) alerting investors about the slowdown in Chinese spending. Sandalwood is a data vendor that specialises tracking Asia/China consumer spending through a unique platform of 25+ datasets. To help global investors, the firm will publish timely data-driven reports on public companies providing demand trend analysis and quarterly projections.

Starling Advisors

An “ultra” luxury brand, synonymous to resilience - strong brand momentum has continued despite complex and challenging market conditions. Alex Dwek believes company guidance for the full year looks very conservative. Margins for 9M 2023 were 28%, meaning that the margin in Q4 could be as low as 22% to reach the full year guidance. For 2024, Alex expects a normalised revenue growth (+6%), in a year which should benefit from several product launches. The order book covers 2025, with oversubscription for every model except for one. TP €384 (25% upside).

ResearchGreece

The Greek retailer’s heavyweight Dec trading update showed group sales growing +9% y/y, pushing FY23 sales +14% y/y, or +200bps above company guidance. Quite a remarkable performance considering a) 2 stores (out of the 53 in Greece) remained closed during Q4 (floods); and b) the group has been strategically reducing prices in recent months. With net cash at €431m, management announced a €0.60 DPS. While investors should keep an eye on container freight costs (up 90%+ in the last few weeks), ResearchGreece remains very bullish on the stock. Trades at (2024E) 10.1x EPS (x-cash); 7.5x EBITDA; with a 5.9% dividend yield. TP €33 (25% upside).

TobaccoIntelligence

BAT reacts to surprise suspension of Velo pouch sales

BAT did not expect the temporary sale suspension of its Velo nicotine pouches in Italy, ordered by health authorities, and is prepared to take action. Italy’s Ministry of Health suspended the retail sales in the country at the end of Dec. A spokesperson for BAT in Italy told TobaccoIntelligence the group was surprised by the measure as Velo pouches are “absolutely compliant with the current law and subsequent prescriptions".

the IDEA!

Aims to double EBIT organically by 2027 - BRNL, a global provider of flexible specialist workforce solutions, has presented challenging goals at its latest CMD. In the IDEA!'s 23-page report, they assess the feasibility of these targets and believe the most important parameters to achieve these objectives are revenue growth (HSD organic) and gross margin (at least unchanged). When analysing the verticals in which BRNL operates a LDD revenue growth should be feasible. They see fair value of EUR 16.65 per share, which is ~60% higher than the current share price.

Arete Research

SAP got a lift this week after announcing tough action to meet its FY25 profit goals. However, while Arete applauds the company’s efforts they struggle to get too excited. Restructurings of this magnitude are not without risk. It is also notable that SAP beat its FY23 targets on licences but scraped home at the bottom end of the range for Cloud growth. The stock is already trading on 23x FY25 FCF if it hits these goals. Arete would rather own Salesforce which trades at a similar valuation but is a much better asset.

North America

280First

AI driven 10Q / 10K filings analysis

Since there are always reasons when companies change the wording in their financial filings, being alerted to these changes allows investors to realise potential risk factors and opportunities before they are reflected in the market, ideal for idea generation and portfolio monitoring. Stocks recently highlighted by 280First include Arrowhead Pharmaceuticals (ownership change / cash flow needs / Horizon license agreement), Atmos Energy (more benign competition), Dollar General (rethink capital allocation and dividends / store openings) and MACOM (increased competition / less pricing power).

Huber Research Partners

NFLX added 13.1m subscribers in 4Q23 (vs. 8.8m guidance) and management expects stronger 1Q24 net adds than they saw in 1Q23. Revenue growth accelerated to 13% in Q4 and should continue to accelerate in 2024 (Craig Huber estimates up 14.9% vs. 6.9% in 2023) and 2025 (+16.1%), driven by price increases, scaling the advertising business and continued monetisation of previously shared accounts. Operating profit margins will continue to expand (Craig forecasts 24.7% in 2024 and 29.4% in 2025 vs. 20.6% in 2023). He raises his 12-month TP to $610 based on 20.0x 2025(E) EBITDA or 24.4x EPS.

Housing Research Center

The revaluation of the housing industry

Is it possible for the public builders as a whole to be revalued by Wall Street based on the premise that fundamental structural changes have taken place that deserve a fresh look at the way the companies are valued? Alex Barron certainly thinks so. With stronger balance sheets and more defined business models, the builders are likely to offer more predictable earnings streams and growth in book value. Alex doesn’t see any fundamental reason why P/B of 2x should be the ceiling for the builder stocks. If they are growing rapidly and generating a high ROE then there is no magical ceiling that should limit them. The builders should trade at a P/E of 10-15x going forward.

Veritas Investment Research

Despite a 50%+ drop from its 52-week high and ongoing cost reduction efforts, the potential for further downside remains high. Veritas' report focuses on how 1) the automotive aftermarket industry has grown substantially, but AAP has been losing market share in both the DIY and DIFM segments. 2) Over three decades, the company's operating margin has consistently lagged peers. 3) The company has unique off-balance sheet supply chain financing exposure (60% of its EV). This exposure is considered an outlier and the estimated financing components are substantial. Normalising operating lease liabilities further reveals higher leverage than reported. TP $38 (40% downside).

R5 Capital

Scott Mushkin thinks it is glaringly obvious that the company does not have enough labour in its stores, is putting off basic maintenance and has not invested enough in its asset base. While eliminating a competitor through a merger that should yield significant synergies would normally lead him to be more positive, Scott’s research around the poor store conditions and Walmart’s execution improvements being accompanied by an accelerating remodel programme, has led him to become very bearish and he sees significant equity downside despite the modest PE and EV/EBITDA multiples afforded to the stock.

Portales Partners

Banks are still attractive

Charles Peabody provides a comprehensive analysis of recent 4Q23 results and his revised outlook for 2024-25. No bank sharply exceeded expectations, but NII was generally better than anticipated, while credit trends were generally worse. The revenue outlook for 2024 is mixed with high hopes for capital markets revenues and expectations that NII will bottom by mid-year setting up for a robust 2025. Charles favours 1) Citi - epic valuation discount to TBV but is mistakenly ignored by many as a value trap. 2) Wells Fargo - saddled by excessive CRE exposure, but investors forget this company has survived every CRE cycle of our lifetimes. 3) JPMorgan - "over owned" but still benefiting from the First Republic deal.

MYST Advisors

OTC birth control rollout to drive considerable earnings inflection - the opportunity for Opill in the US is huge (estimates an incremental ~60% accretion to EPS if PRGO achieved similar pricing and penetration (~10%) as it did in the UK). PRGO shares continue to trade at a trough valuation even though the company has been “cleaned up” over the past 5 years following the exit of 3 ancillary businesses and last year’s replacement of a previously deal-focused CEO. Trades at ~9.6x FY24 EBITDA and ~11x EPS (vs. peers in the low-teens EBITDA / high-teens EPS multiples). TP $60 (80% upside).

ERA Research

Following eye-watering share-price appreciation over the past 12 months (+80%), ERA believes that BCC has run ahead of fundamentals. A lasting recovery in US housing over the coming years could see wood products buyers switch back to purchasing larger orders directly from mills, which would threaten top-line growth in BCC’s distribution business. Further, a raft of new OSB supply, coupled with rising plywood imports from offshore should put downward pressure on structural panel prices as 2024 progresses. At current levels, equity price risk is downside weighted and evidence that structural panel prices have reached a near-term peak (likely this quarter) should present an attractive entry point for building short positions. TP $108 is based on a 5.0x multiple applied to 2024 EBITDA of $691m.

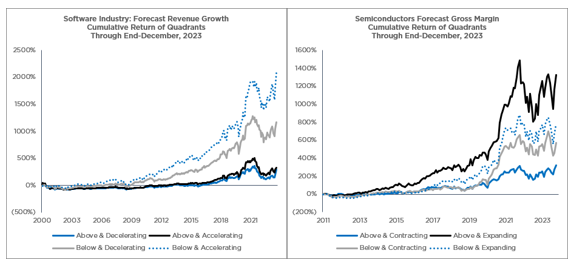

Trivariate Research

Favour Software over Semiconductors

While these industries are highly correlated, high inventory, lower-than-average growth and stretched valuation fuel Adam Parker’s caution on Semis. Within Software, he sees a continued trend toward productivity investments from major corporations, and reasonable growth, high margins, and valuations that are no longer an impediment. The best performing Software companies are those with relatively lower growth that is accelerating. For Semis stock selection, gross margins matter. High margin companies that are contracting strongly underperform high margin companies that are experiencing gross margin expansion. Quantitatively derived long and short ideas are available on request.

ETR

2024 Enterprise Tech Demand: Technology Spending Intentions Survey

ETR highlights the vendors best and worst positioned for the year ahead based on spending intentions data collected from their Jan 24 TSIS, which saw participation from 1766 IT Decision-Makers, including 308 Fortune 500 and 423 Global 2000 organisations. Respondents are, on average, more optimistic on 2024 spending than 3 months ago, with full year spend anticipated to grow +4.3% vs. 2023. However, Q1 is slightly tempered, now sitting at +2.4% y/y growth. Vendor outlook upgrades include Gitlab (has seen a sharp rebound in its Net Score), SentinelOne, Elastic and IBM. While there are downgrades for Datadog (Net Score hits an all-time low), CyberArk and HashiCorp.

Japan

Astris Advisory Japan

Generative AI: With Japanese LLMs coming online, 2024 will be more eventful

In 2023, generative AI took the world by storm but the impact in Japan was less exciting as language and heavy computing loads dampened performance. That should change with the deployment of Japanese-specific LLMs which are already performing modestly better in some tests versus larger general-purpose English LLMs and with less power intensity. Kirk Boodry lays out the basics and state of play for generative AI in Japan within his Telecom / Internet coverage. SoftBank Group and NTT have been early winners thanks to exposure at the infrastructure / platform layer, but true gen AI deployments are only just starting.

Azabu Research

Mike Allen expects NMAC to post OP of ¥5bn (vs. consensus of ¥4bn) when the company reports Q3 results on Jan 30th. In the previous quarter, NMAC’s operating profit exceeded original consensus forecast by 95%, and for a stock with 18% of its M/Cap in cash, a trough RoE exceeding 18%, and almost zero capital requirements, he thinks it is unambiguously cheap. But the market seems unimpressed, at least so far. In the past three months, the stock is up 13.1% vs. Topix +12.8%. In his latest report, Mike details what needs to happen to gain the market’s attention.

Asymmetric Advisors

ML, the No. 3~4 global forklift player, has seen its share price nearly double since Asymmetric turned bullish last May. A combination of strong US orders and backlog, price hike effect and FX have boosted earnings whilst a large amortisation charge will disappear from FY3/26. Despite the impressive share performance, Asymmetric remains the only broker covering the stock and ML's PER remains low at <7x next year vs. >13x at global peers Kion and Jungheinrich.

Emerging Markets

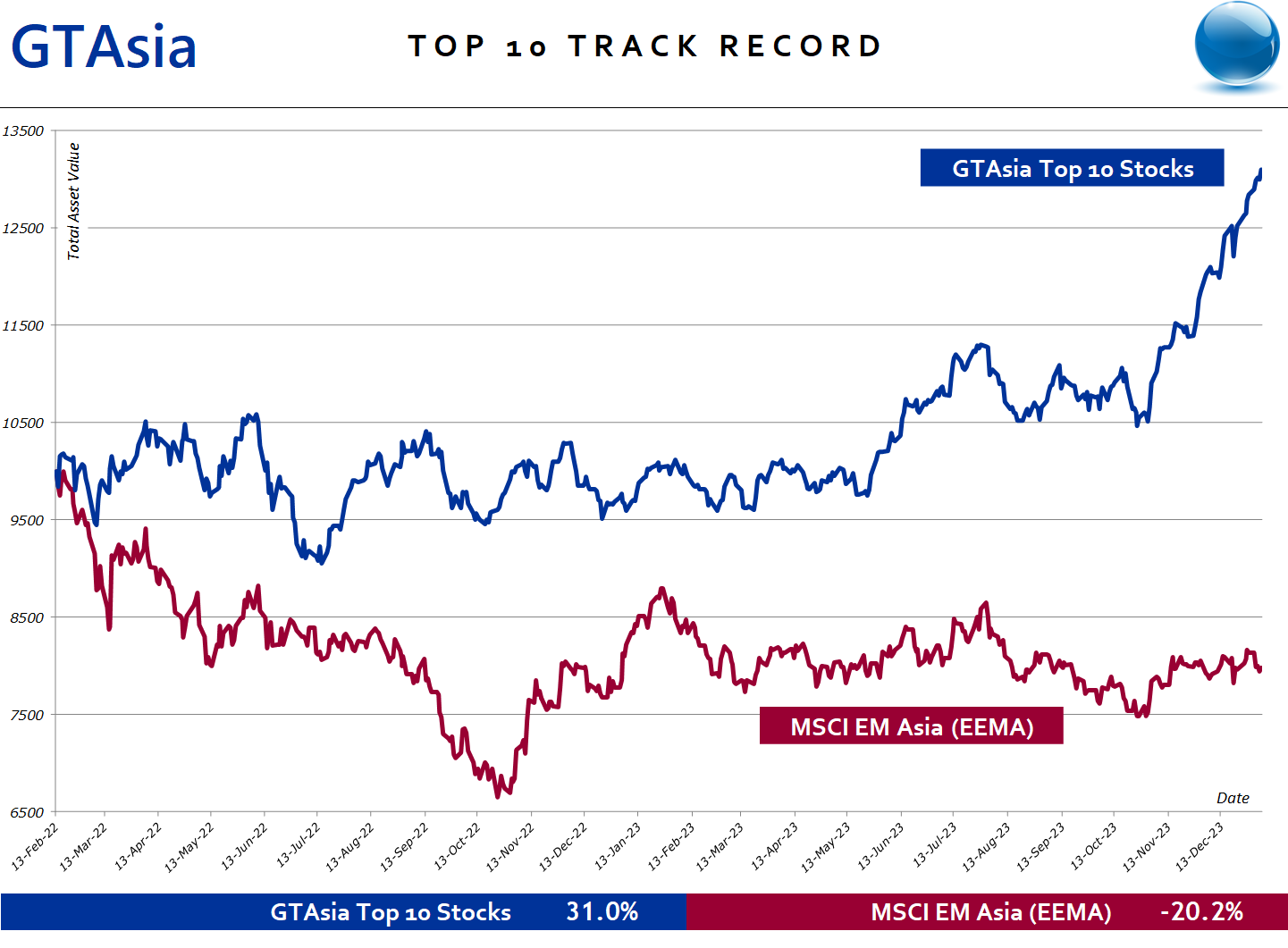

Crystal Shore Alpha

CSD’s Top 10 Asia Stocks have outperformed MSCI Emerging Asia by an astonishing +55% over the past 2 years

The flagship strategy combines 1) CSD’s weekly ranking of 900 Asian stocks and 2) CSD’s country risk scores covering China, India, Taiwan, South Korea, Indonesia, Thailand, Malaysia, Philippines and Pakistan. Top 10 Asia stocks is delivered to subscribers every weekend before the Monday morning market open in Asia. The top 3 performing positions are Hindustan Petroleum (+74.2% since BUY on 15th May 2023); Tata Consumer Products (+31.6% since 2nd Oct 2023 BUY); and Yes Bank (+30.6% since 4th Dec 2023 BUY).

Westlake International

China: Cautious ad spending outlook but branding ads likely to be driven by major 2024 sports events

From Westlake's primary research, most large advertisers remain cautious about their 4Q ad spending and 2024 ad allocation outlook, but the UEFA European Football Championship and Paris Olympics this year will likely drive branding ad spending growth. Baidu can deliver 4Q online marketing (primarily search and feed) revenue growth at least in line with street expectation of 5-6% given the strength from medical, eComm, EV, travel and restaurants, offsetting some share loss to closed-loop searches within mega or popular apps. Tencent saw solid 4Q social ads, healthy online video ads & subscriptions and in line global game performance, and is likely on track to meet street revenue expectation. Westlake continues to see strong growth momentum from Tencent's Video Account ads.

Tabbush Report

India Banks: NPL ratios see a dramatic an improvement

There is significant growth potential for India’s banks, in consumer and corporate loans, the system is incredibly under-penetrated. As banks see dramatically lower NPL levels this will allow loan officers to become less risk averse, to lend more. Improved NPLs appear to be real, with strong financial metrics for corporate India on debt/ebitda and interest coverage. Credit cost reductions have been dramatic and this can continue. ROA expansion is significant with many driving factors including loan volume, better NIM and lower credit costs. LDR expansion can further support ROA expansion and profit delta, which was generally not rising in recent years.

AlphaMena

QNB delivered a strong FY23 with an 8% increase in net profit despite a QAR 3.5bn loss on hyperinflation in Turkey. AlphaMena remains bullish because of QNB's strong government support (35% of loans), resulting in high asset quality and sound profitably. By maintaining a dominant market share in Qatar and a growing international contribution, its diversifying business mix can sustain its top-line positive momentum amid a rather unfavourable interest rate environment. The sharp plunge in the share price since 2022 offers a great opportunity to buy shares in one of the world's strongest banks. TP QAR 21.0 (30% upside).

Macro Research

Developed Markets

Belkin Report

Soft landing? Yeah, right!

Michael Belkin forecasts a major decline in 2024 S&P500 earnings, with a year-end earnings target of $120, about half of the Wall Street consensus. When will earnings decline? They peaked in Q4/2021 after a surge in stimulus and inflation. Two years since the Fed started tightening and the economy is finally starting to feel the impact. Expectations of a soft landing are naïve, despite it being the overwhelming consensus. The macro picture is changing, and Michael’s model has turned LONG the USD and LONG energy. The model also suggests an EM capital outflow is looking likely, with fresh SELL signals on numerous EM currencies. The elephant in the room is China, with a culmination of factors dragging the global economy down. With the consensus hooked on the soft landing nirvana, prepare for earnings warnings, misses and a downgrade of current bullish sentiment that send equity markets south in 2024.

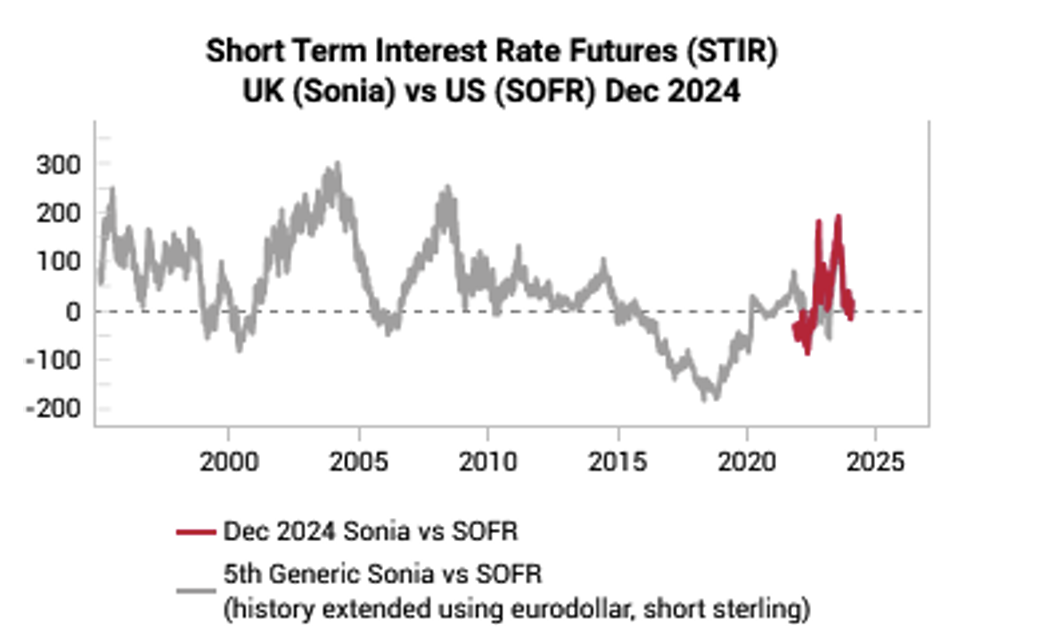

Variant Perception

UK: SONIA vs SOFR

In their 2024 UK themes, Variant Perception discussed the disinflation consensus and the contrarian long GDP/USD set up. Another expression of this idea is SHORT SONIA futures vs SOFR futures. It is very notable that the UK is flipping back into a hawkish regime while the US remains dovish, but this divergence has not been reflected in short term interest rate (STIR) pricing (see chart). The spread between SONIA and SOFR Dec 2024 futures is around 0, having peaked closer to 200bps back in the summer of 2023. The team continue to see more signs of stabilisation in UK growth leading indicators. The team also reminds readers again of the contrarian GBP set up that causes them to have a “buy-the-dip” bias on GBP this year; on a 12-month basis, the GBP is a contrarian LONG. As the UK maintains a loose fiscal policy and tight monetary policy, it can suck in foreign capital to finance the current account deficit, supporting the currency.

Greenmantle

Poland: Dismantling PiS

In Poland, the new centrist government led by prime minister Donald Tusk is trying to undo eight years of rule by the right-wing nationalist Law and Justice (PiS) party. Tensions between Tusk and President Andrzej Duda, who hails from PiS, have already reached fever pitch. The stand-off will slow the pace of EU-mandated reform, but Niall Ferguson’s base case is that Brussels will unlock Poland’s frozen COVID-19 recovery funds regardless. Meanwhile, the economy is running hot. Fiscal policy is likely to remain expansionary, providing a boost to household incomes. The National Bank of Poland will ease significantly less than other central banks this year - for political as well as economic reasons. Niall is bullish PLNEUR and Polish sovereign bonds.

Pennock Idea Hub

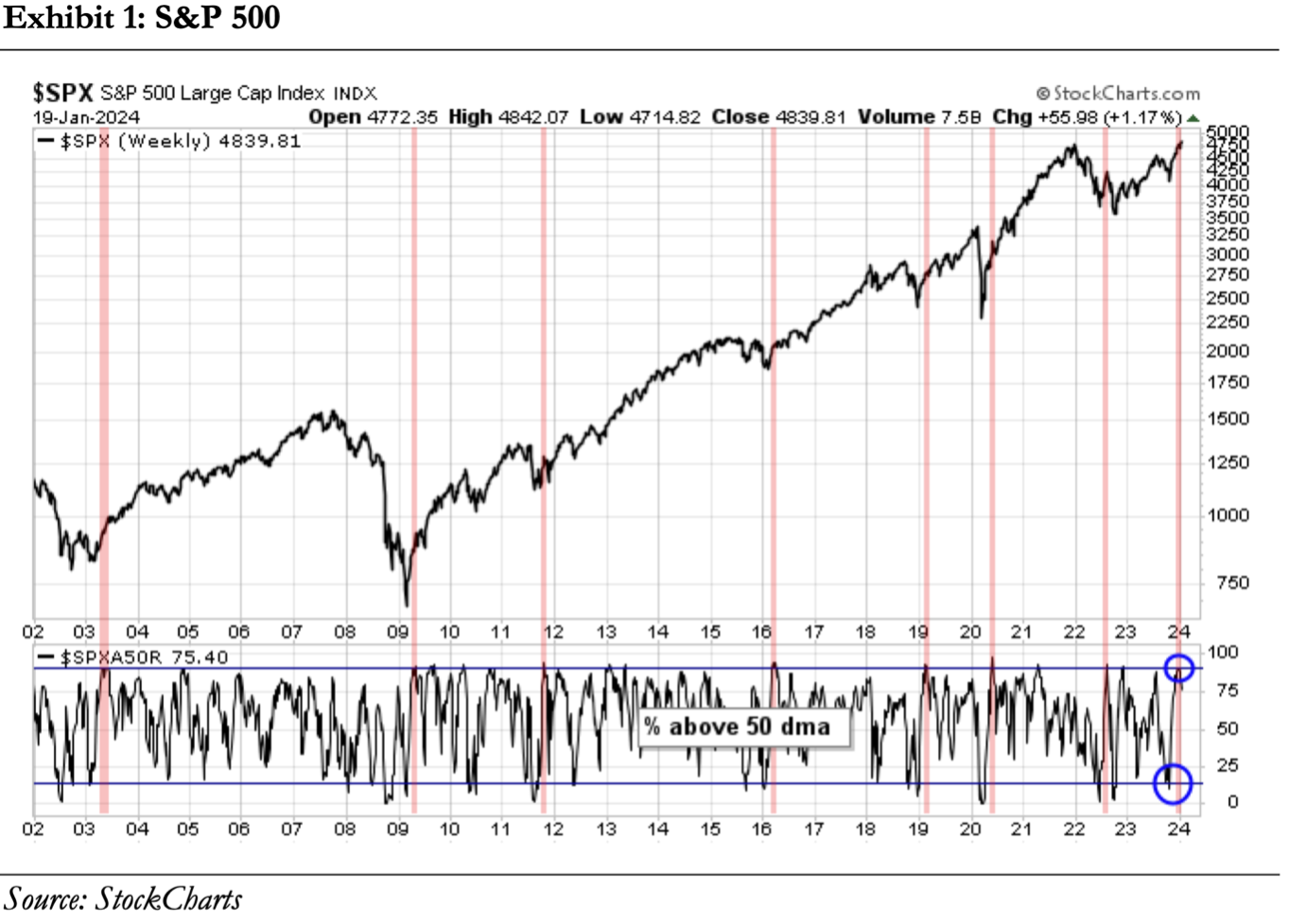

US: Reasons to be bullish

According to Cam Hui, a bottom-up driven scan of stock charts shows numerous stocks with bullish technical patterns consisting of uptrends or breakouts from multi-month bases with strong potential upsides. Bullish patterns are broadly based, primarily concentrated in technology and cyclicals, which argue for a continuation of the AI-related bull and an economic rebound. This bottom-up analysis also pointed to bullish macro conclusions about the economy. Exhibitions of powerful price momentum are rare. Since the market bottom in 2002, there have been eight occasions when the percentage of S&P 500 above their 50 dma has surged from below 15% to over 90% in a brief period. That latest episode occurred when stock prices soared off the bottom in October 2023. These price surges were usually resolved in either a short-term consolidation or setback, but the S&P 500 was invariably higher a year later with a 100% success rate.

Talking Heads Macro

Australia: The biggest disconnect in central bank pricing

Wage growth is a key barrier that stands in the way of faster RBA easing, claims Manoj Pradhan. However, declining demand along with the surge in immigration and participation suggests that real wages can rise via falling inflation and keep wage growth steady, allowing the RBA to ease in line with other central banks. The 65bps of cuts priced in for the RBA is unreasonably low given the fundamental and broad-based weakness in the economy. Receive 1y1y. All rates are moving in lock-step with the US for the moment. The bet here is that Australian rates will move lower faster than almost everywhere else over time, including the US and AUD. There is likely to be some whipsaw if the central bank resists fundamental gravity – that makes FX a more two-sided bet compared to rates.

AAS Economics

US: What drives the economy?

Rather than looking at many economic indicators to establish the state of the economy, it is going to be more effective to establish the key factor that drives the economy. Frank Shostak suggests that this is the pool of real savings. With respect to the Fed’s monetary policies, the market is starting to sense that the US central bank is likely to ease its interest rate stance in a few months’ time. For the time being, the ongoing Fed’s tampering is continuing to distort the economy. This undermines the process of real savings formation. Because of the time lag from changes in money supply and its effect on economic activity and prices, Frank is of the view that the strong decline in the momentum of money is likely to dominate the economic scene in the months ahead.

East Asia Econ

Japan: Love Labour’s Lost

In its quarterly outlook report, the BOJ once again presented a constructive view of the outlook for wages. Given there is plenty of room for interest rates and the JPY to move, Paul Cavey says the bank's cautious confidence obviously matters. What is also interesting about the bank's continuing optimism is it seems to be at odds with the hard data for the labour market. The unemployment rate hardly moved in 2023, and in the latest release, headline wage growth slowed. Obviously, then, the bank isn't placing much weight on these hard data. Rather, its starting point is its own Tankan survey, which shows labour market conditions – particularly in non-manufacturing – reaching a level of tightness not seen since the bubble in the 1980s.

Grey Investment

Japan: Breaking free

The Topix recently hit 2,507, the best level for almost 33 years. The all-time high of 2,855 in 1989 now looks reachable, and Chris Roberts’ base case is that the breakout will see a move to at least 3,400-3,600. There will be a whole new generation of investors in Japan who did not experience the pain of the 22+ year decline, so when the barrier is broken, they can dare think big. For a truly powerful advance, sustained yen strength is required – Chris is currently neutral on the yen, but comments that a breakout would be an indication of broadening interest in the Japanese bull market. Chris remains 100% LONG the Topix from 2,073.50.

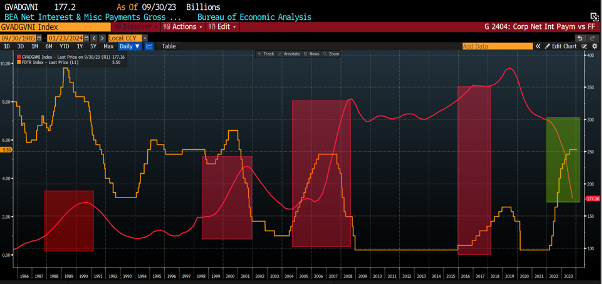

Ollari Consulting

The question nobody cares about anymore: What is r*?

Christophe Ollari recalls how, only a few months ago, at the peak of the rates malaise partially triggered by stubbornly hot US data, the overwhelming debate was around the fact that r* might have shifted meaningfully higher. At the latest Dot Plot released last December, 7 Fed officials put their long run Dot above 2.50%, arguing they envisaged a higher neutral rate. A lot of potential explanations have been floated to explain the US economy's resilience. Starting with US consumers’ excess savings and that large corporates have in fact benefited from the rate hikes as they front-ran their funding needs in 2020-21, at ultra-yield levels, going into the rate hiking cycle long of cash. The key graph in that respect (see graph): collapsing net interest paid by US corporates despite a 500bps increase of the FF rate. In other words: factors that have impaired the monetary transmission channel with effects of the monetary tightening still to come.

Emerging Markets

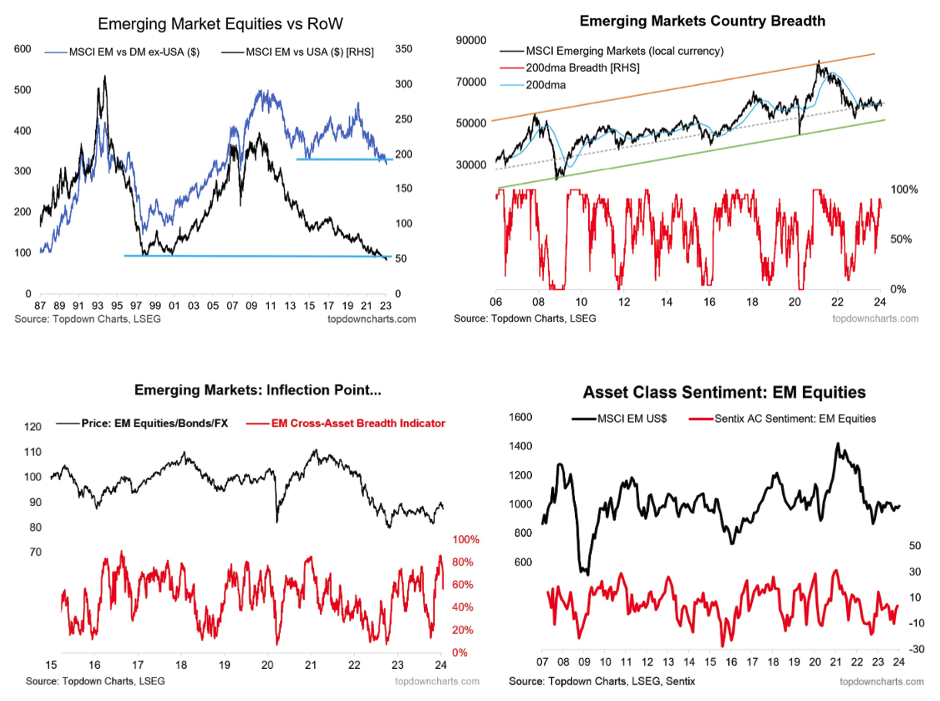

Topdown Charts

EM: Wearily bullish

EM equities have broken down through key long-term support lines relative to DM and US equities, which is a concern. However, the MSCI EM index in local currency has held onto its long-term uptrend line with strong breadth. Callum Thomas sees the rebound in the USD as a key risk to EM. There is hope in the form of the EM policy pivot to easing, but this will need to be large and fast enough to offset further USD strength. Meanwhile, the EM cross-asset breadth indicator has held onto its major inflection point and surveyed sentiment on EM is ticking up but is not excessive. The background of cheap valuations, upward trending broader sentiment indicators, the EM central bank pivot, and potential for Chinese stimulus means EM equities remain attractive. Remain bullish but reduce conviction in the face of short-term risks/headwinds.

GFC Economics

The fault at the heart of China’s strategy

China’s dominance in the broader renewables supply chain is clear, achieved with smart subsidies early on. However, debt has risen as a share of GDP, and property woes subsist. Growth in the three key sectors – EVs, solar, batteries – is providing an offset to the country’s these woes, but overinvestment in renewables threatens further downward pressure on prices and a profits squeeze. This will lead to a retaliatory backlash from nations struggling to compete with China, stoking trade tensions. It is not possible for China to grow at its current pace and maintain its manufacturing output without increasing its share of global trade. This is the fault line at the heart of China’s strategy, remarks Graham Turner: Western governments want to reduce their reliance on Chinese imports, not increase it.

PRC Macro

China: Holiday blues

So far, there are few indications of sharply lower activity levels outside of normal seasonality. That is, except for PBOC liquidity injections. There is always some form of seasonal liquidity injection for the holiday period, but as William Hess has been noting for weeks, large and highly volatile levels of PBOC net outstanding OMO is indicative of abnormally high liquidity demand from some quadrant(s) of the economy. The property sector and related creditors are the obvious sources of systemic stress. The recent bloodbath in onshore equity markets didn’t help either. But, as has been the case in the interbank market, significant state intervention in equity (and the FX) markets helped to stabilize levels. None of this seems consistent with President Xi’s call to make China a “financial powerhouse”. It also draws into question the policy implications of related calls for a “strong economy, strong currency and strong central bank”.

Alberdi Partners

Colombia: Endorsement of the radical?

According to Marcos Buscaglia, Colombian President Gustavo Petro is showing signs of frustration and discontent. The first far radical leftwing president since competitive elections were established, Petro has found strong and effective opposition in congress, mass media and the business sector. To his disappointment, the voters that supported him have not rallied behind his radical reform agenda. Because Petro fails to understand that he won due to a protest vote rather than to a firm endorsement to his agenda, he has been unable to find a strong base of support for his unconvincing roadmap to a more environmentally friendly and state-centered economic model. The 63-year-old former guerilla fighter faces an uphill battle to leave a legacy as President. Unfortunately for him, if he remains in denial about the popular support he really has, he will continue to miss viable opportunities for sensible and moderately progressive reforms.

Emerging Advisors Group

Indonesia: Still in, still watchful

The underlying mantra of Jonathan Anderson’s Indonesia position is simple: a flat economy at home, no import pressures, no inflation pressures and decently attractive bond yields. This doesn't do much to recommend Indonesia as an exciting equity story, but it has helped maintain a relatively stable rupiah and kept him in IDR fixed income. The main “swing vote” is the external balance. As with most of Jonathan’s EM FX and local fixed income positions, the trend most likely to force an exit is a widening external deficit. Jonathan is keeping a cautious eye on the recent volatility in the country. The trade numbers swung Indonesia into implied deficit last year. They are once again strengthening at the margin, so he’s holding for the time being, but this is what you want to watch.

Teneo

Kenya: Support in times of trouble

The IMF’s latest review and augmentation of Kenya’s three current facilities shows how supportive the Fund remains of the sovereign amid the country’s public finance squeeze. Nonetheless, the IMF voiced significant concerns, including over debt management capacity and shortfalls in tax collection, which will increase pressure on President William Ruto’s government to further increase taxes and collection despite their unpopularity and potential dampening effect on the economy. Geopolitical factors, including heightened regional instability in the Horn of Africa, will likely enable Kenya to count on continued support from the IMF to help the country avoid a default on its Eurobond maturing in 2024.

ESG

Queen Anne's Gate Capital

CCUS and the energy transition

The jury is still out on how big a role CCUS (carbon capture, usage and storage) can play in the energy transition. A recent study sees the opportunities in the sector expanding exponentially in 2024, with 119 projects aiming for FID this year. Most of these projects are in North America, as a result of the Inflation Reduction Act and Infrastructure Law. Projects coming on this year are mostly hubs. On the flipside, another study finds that the viability of a number of projects in CCUS rely on a much higher carbon price. Their study of natural gas-powered engines found that CCUS projects would need a breakeven carbon price of $307/tonne. The US federal compensation for carbon is currently $80/tonne. This makes these projects uneconomic in the short and medium term, unless costs can be brought down elsewhere.

Commodities

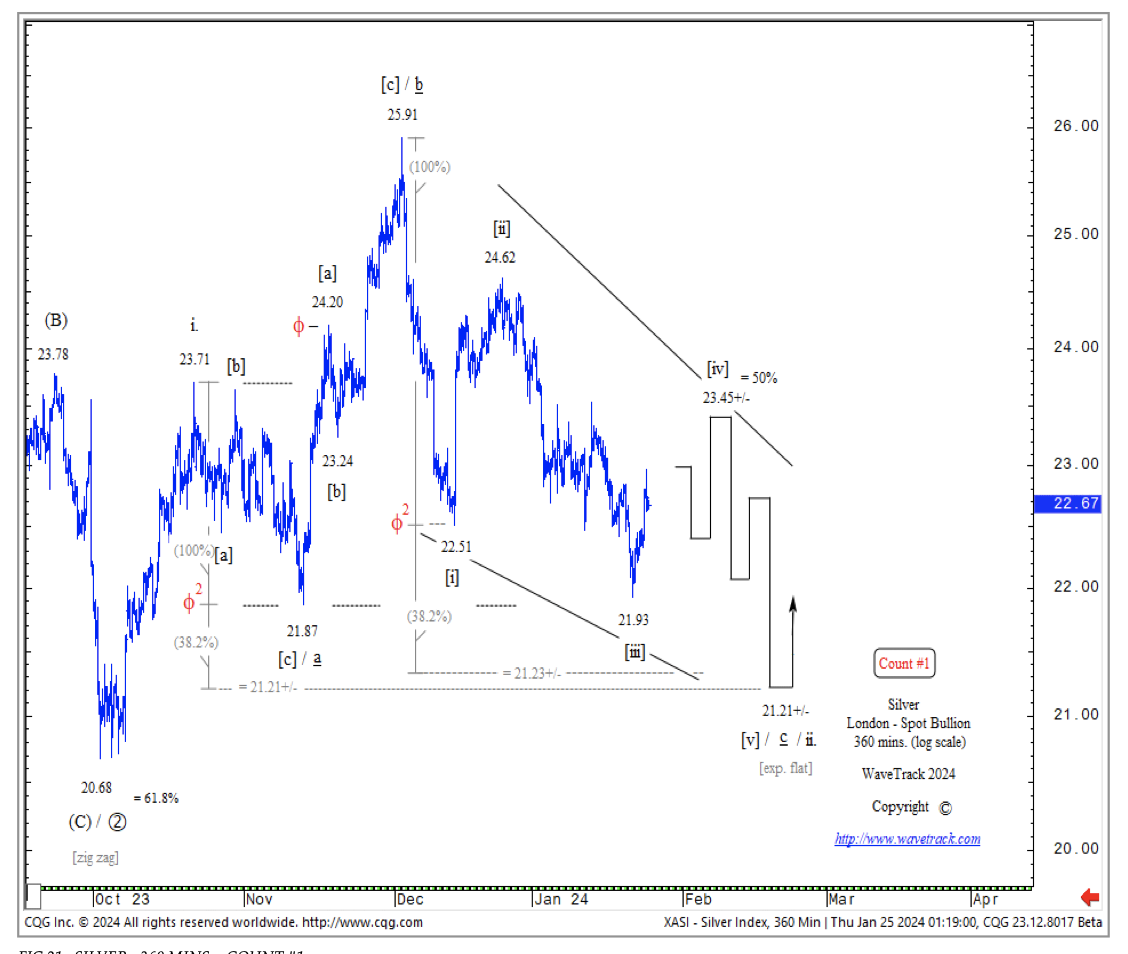

WaveTrack International

Precious metals: From limbo to bullishness

Gold’s relative outperformance over silver since December has been surprising insomuch they both began unfolding into similar corrective patterns, but silver is far more advanced than gold. Even a short-term bout of USD weakness recently failed to motivate gold into a counter-trend rally. Whilst gold’s pattern is in limbo, that’s not the case for silver – it’s expanding flat correction from October’s high is still working lower towards 21.21+/-. Platinum confirmed intermediate wave (2)’s low at 875.36 mid-month with evidence of a five-wave uptrend since – very bullish. Palladium hit a major low mid-month, completing intermediate wave (4)’s expanding flat pattern that originated from the Feb.’20 high of 2880.87 – very bullish.

CPM Group

PGM projections to 2050

According to Jeffrey Christian, the tide is turning for platinum group metal fabrication demand. Platinum, palladium and rhodium markets have been dominated by their use in catalytic converters for half a century, but now that demand is contracting, a great deal of imbalance is underway. CPM Group’s latest report provides detailed statistics and analysis through to 2050. The 95-page annual report includes a realistic assessment of the evolving trends in the alternative energy and vehicle propulsion markets; the outlook for fabrication demand by end-use; market share and sales volume by region for vehicles; supply analysis and outlook for major PGM producing countries, companies and mines. Please contact us to find out more.