Company & Sector Research

Europe

Betaville

On the morning of 8th Feb 2024 Betaville published a paywall protected UNCOOKED Alert re. the renewed takeover rumours circulating about SMDS and highlighted one of the rumoured acquirers as MNDI. An hour and a half later SMDS confirmed it had received an approach from MNDI to create a £10bn packaging giant. SMDS shares initially rose 16% on confirmation of the Alert. Other Betaville Intelligence Alerts that have recently been confirmed include Italy-listed oil refiner Saras and Germany / US-listed pharmaceutical company MorphoSys.

Pernas Research

A globally recognised luxury brand that has existed for over 168 years - BRBY finds itself in the later stages of its brand elevation journey and currently trades at ~12x 2023 earnings. The company has been in the midst of a seven-year transformation aimed at revamping its product offerings and pricing architecture. Although market sentiment is negative towards the stock due to temporary headwinds and brand elevation risks, taking a longer term outlook Pernas Research sees a minimum of 50% upside as BRBY has the right mix of heritage and strategy.

ResearchGreece

ResearchGreece initiates coverage with a Do Not Own (DOI) rating due to a) the low-capped-earnings growth outlook; b) the uncompelling 3.6% dividend yield left over from 2023 (paid in 2024); c) DCF/DDM valuation; and d) the warranted discount to peers given the shorter remaining concession life. Some investors may consider the average dividend yield of c.8% between 2024-2046, assuming a 100% payout ratio, to be a good enough reason to own the stock, but weak earnings growth (2023-2030 clean EBITDA CAGR at +0.7% and EPS CAGR at -0.4%), means the dividend yield edges closer to 6.6%-7.4% in 2025-2030. Therefore, they fail to see any upside or capital appreciation above this yield at the current share price.

the IDEA!

FY23 results were well ahead of market consensus following an impressive final quarter. Ahead of BAM's CMD, the company unveiled its main financial targets for 2024 to 2026. Besides an adjusted EBITDA margin of between 4-6%, it targets revenue of €6bn+, capital ratio of c.25% and a return to shareholders consisting of a dividend amounting to 30-50% of net income from operations (8% dividend yield) and additional cash returns via share buybacks. the IDEA! argues BAM’s mid-term financial targets are not overly ambitious and reiterates their view that the stock is significantly undervalued.

Ben Jones Investments

AAZ reports maiden JORC resource at Xarxar copper deposit. Xarxar (and Garadag) form an important part of the miner’s strategy as it looks to increase production from ~30koz GEO in 2023 towards 200koz GEO by 2028. The next steps involve bringing Gilar into production in 2H24, a JORC resource estimate for Garadag and pre-feasibility studies for a joint Xarxar and Garadag mining operation. Ben Jones believes AAZ is significantly undervalued.

Forensic Alpha

With Q4 results released earlier this month, Forensic Alpha claims the level of inventory now looks even more alarming than when they flagged concerns in Oct last year. Even as sales continue to decline, inventory is growing in absolute terms. DSI has increased from 216 days (Q3) to 287 days (Q4). At the current level of sales, this would take over 9 months to clear down. The recent change in CEO creates a risk that NOD will take a “big bath” on the accounts in the next few months - writing off inventory and / or recognising higher provisions for rebates.

North America

Quantitative Partners with Phil Erlanger Research

DEFCON 4 for long/short and aggressive long only managers

Even though the S&P 500 has hit new highs multiple times this year, the percentage of Type 4s (defined as a Long Squeeze where the stock is lagging the S&P 500 and short selling is below average) has climbed as well. This is a precursor of potential trouble ahead as the percentage of Type 4s should be falling against the S&P 500 not rising. In the past, as you can see above such a relationship has led to a sell-off or a correction in the S&P 500 when the Type 4s move above 10% after being below 10%. For the full report including further details of the 4 different Types of stocks click here.

Paragon Intel

CEO Bill Ready underwhelms against heightened expectations - Paragon Intel’s thesis is that Ready struggles with monetisation and that while they expect him to drive an increase in velocity of product development, he will be unable to fundamentally alter PINS growth trajectory because the company's desire to become a shopping hub is due to its business model needing that to happen vs. minimal demand from online shoppers. Paragon expects Ready will grow MAUs 4-6% and ad load per hour 3-5%, but fail to move the needle on user engagement, which will grow just 0-2%. As a result, ARPU per MAU will grow 5-10% annually to reach just $7.01-7.70 in 2024.

The Retail Tracker

Long & short ideas in the Consumer and Retail sectors

Target (TGT) - product improvements continue; stronger value message positions TGT for a better year ahead.

Gap (GPS) - key brands Gap & Old Navy building momentum; while the new CEO is expected to have a positive impact.

Nike (NKE) - lower expectations off Nov Qtr impacted the stock, but adding back retailers allows for EPS acceleration throughout 2024.

Williams-Sonoma (WSM) - the stock is at an all-time high; sees a mismatch between expectations and earnings performance.

Kohl's (KSS) - continues to struggle with its business, yet the stock has traded up with peers, look for share weakness on 4Q results.

VF Corp (VFC) - not convinced the company can turn it around after a tough 2023 as it looks to trim its portfolio of brands.

Real Street Retail Research

ULTA's bet that big Jan / Feb launches would help regain prestige beauty share losses from 2023 may be at risk. While Sol de Janeiro and Charlotte Tilbury are the most highly anticipated launches in ULTA's history, foot and web traffic were down in Jan (-4.3% & -0.5% respectively per Placer & Similarweb) and a sudden downtrend in the mass beauty segment (-3% YTD Y/Y per Neilsen) threatens to offset this newness. Momentum in exclusive Sephora brands and stagnation of legacy brands (EL) dampen the outlook even further.

Gordon Haskett Research Advisors

Big 4Q23 beat driven by traffic & US GPM - FY24 guide looks conservative as the 2-year stacks need to implicitly decelerate from 1Q24's ~11.4% run-rate… a phenomenon that GHRA doesn’t think manifests as WMT's General Merchandise categories continue to mean revert. EPS of $7.30-7.50 looks plausible this year. From a capital allocation perspective, WMT returned to more aggressively repurchasing its stock which alongside the largest dividend increase since 2014 are all signs of a management team playing offense. The model's moat is becoming “Costco-like”, which reinforces GHRA’s positive stance. TP increases to $200 (25x FY25E EPS of $8.00).

MYST Advisors

AXP’s revenue growth has been slowing in its largest, most valuable and highest multiple business - sees a scenario where: 1) discount revenue growth continues to decline / stagnate; 2) fee revenues are not repeatable; and 3) consumers become more reluctant to pay higher fees, intensifying concerns that the AXP model is broken. The only other way for AXP to maintain its growth is through its balance sheet. It has been vying for the "incremental prime consumer" by growing its loan book aggressively, which will result in higher delinquencies. The share price has risen ~50% over recent months, despite heavy insider selling. Multiple looks "full" with the shares trading over 16x FY24E EPS.

Alumbra Research

Alumbra Research specialises in identifying high conviction short selling opportunities with clear near-term catalysts and longer-term structural issues. Recent successful calls include:

QDEL - share price collapsed 32% on 14th Feb after the company reported disappointing 4Q23 results citing weaker than expected Covid / flu-related revenues. Tim Rickert had previously raised concerns that consensus revenue / EBITDA growth expectations appeared overly optimistic considering the likely non-recurring benefits from normalising excess backlog, settlement gains and government-contract revenue during the first nine months of FY23.

EXTR - share price dropped 27% last month after management issued a profit warning citing weaker than expected revenue in the quarter, before later significantly reducing its FY24 revenue guidance as well. Derek Aherne had been flagging EXTR’s declining backlog coverage (which the firm had recently stopped disclosing) and excess channel inventories (e.g. DSO at EXTR’s top distributor had increased to 94 days (1Q24) vs. 69 days (1Q22)).

Vision Research

Vision initiated a short on CAR to clients on 10th Jan 2023 focused on peaking rental rates and used car values as fleets returned to pre-pandemic levels and promotions increased. Vision expected depreciation to rise, gain on sale of used vehicles to abate and rising debt per vehicle to raise interest expense. The short was closed on 16th Feb 2024, generating alpha of 61.2% as the shares declined (31.2%) while the S&P 500 rose 30.0%. At the time of the initiation, ADV was >$150m and there was no cost to borrow the shares.

Vision uses fundamental analysis to identify structurally challenged companies. They currently have 16 active US shorts, 13 active European shorts and 8 active APAC shorts.

Sidoti & Company

A key Dec-Qtr standout was record volumes sold, a function of WIRE’s capital reinvestment and quick-turn model. Copper spreads continue to inch closer to “normal”. This is a precursor to the stock narrative shifting to WIRE’s secular tailwinds, the looming supply shortage of its raw material (a positive) and its best-in-class service model. WIRE continues to deploy cash toward capex and share repurchases ($1.3bn since 2020) yet remains debt-free ($561m cash). Sidoti’s TP increases to $302 (from $241) based on 15x estimated 2025 EPS of $20.11. 40% upside.

Huber Research Partners

AI-hype is aboard the TRI express with the shares recently hitting an all-time high. The stock sells at 23.5x 2025E EBITDA, 40x 2025E Earnings and 37x FCF. This is higher than any other Information Services company Huber Research tracks apart from MSCI (rated OW), but MSCI has a huge moat around its business and 60% EBITDA margins. That is not to say CEO Steve Hasker has not been masterful in re-positioning TRI into growth opportunities and raising the margin profile of the company’s three key segments, but at the end of the day, this is a 6-7% organic growth story, with EBITDA margins in the mid-40% range. Douglas Arthur now estimates 2024 adj. EPS of $3.54 per share (prior $3.80).

ERA Research

Investors should start building long positions in IFP - while Q4 earnings were disappointing (and Q1 earnings may be only marginally better), ERA expects lumber demand from residential construction to improve steadily as the year progresses and a raft of sawmill capacity closures this quarter should also help further improve lumber’s supply and demand balance. IFP’s geographic diversity remains its strong point (it has the lowest relative exposure to high-cost BC at just 14% of sawmilling capacity) and a series of forest tenure sales on the BC Coast will continue to boost liquidity over the next several quarters. TP of $26 is based on a 7.0x multiple applied to 2024E EBITDA of $287m. 30% upside.

BWS Financial

A contrarian deep value asset story - NLOP is trading at a fraction of its book value as the company gets lumped into the negative investor sentiment towards office buildings. It was created and spun out of WP Carey to oversee the liquidation of 59 office properties, but the timing could not have been any worse. News headlines of commercial real estate being sold at materially less than the prior purchase are a regular occurrence. However, NLOP is not in a rush to liquidate its portfolio and nearly every property has a single tenant tied to a long-term lease agreement. Investors can enjoy a dividend of >5% while waiting for additional asset sales. TP $60 (130% upside).

Trivariate Research

Technology Strategy: Finding short ideas

Investors appear increasingly nervous about the strong price momentum in software and semis. This performance has occurred with average volatility vs. history and with declining volatility over the last six months. Trivariate’s analysis reveals how changes in volatility impact subsequent performance. Specifically, it is software volatility that matters the most. Stocks with the biggest change in volatility Q/Q strongly underperform those with decreases in volatility among the group of tech stocks in the highest tertile of CSR (Trivariate has a proprietary seven-factor model to compute company-specific risk). Short ideas include AppFolio, Vertex, CleanSpark and Alkami.

Hedgeye

PI acts like a hot, semiconductor / IoT company (up 100%+ since its lows in late Oct 23), even though it’s not an AI play - instead, it’s a small, plain RFID (radio frequency identification) company that bulls think has achieved a tipping point, while Hedgeye argues new adoption trends have been more episodic than sustainable. PI paints itself as a market leader, but it has been a market share loser over the past decade. Furthermore, it faces significant risk of its largest customer one day becoming a competitor. Growth expectations are wildly optimistic and the stock trades at a very expensive 11x 2024 EV/Sales and 9.5x 2025 EV/Sales. 40% downside.

Japan

JapaneseIPO.com

Having weathered many challenges over the last 20 years, the remaining players in the pachinko / pachislot industry have entered a new phase of growth, according to Yuka Marosek, driven by the innovation of "smart" machines, which offer more interactivity and variety to the players. As the line between pachinko and video game machines becomes more blurred, Sankyo looks set to prosper. Its long history and large scale enables it to develop and market smart machines and collaborate with popular anime series / singers to create attractive and engaging games. The stock is up 70% over the last 12 months, but trades on a cash adjusted PE of 4.95x. The dividend yield is high at 3.6%.

Emerging Markets

Copley Fund Research

The narrowing divide between China and India’s weight in the MSCI Indices

The spread between India and China weights in active Asia Ex-Japan funds has narrowed to the lowest levels in Copley’s 13-year history and now stands at 16.17% vs. a peak of 45.3% in Aug 20. China’s decline over this period has been dominated by Consumer Discretionary, Communication Services and Financials. 3 companies standout as key drivers of the move lower: Alibaba, Tencent and Ping An Insurance. Increases in fund weight have been minimal with PDD, BYD and Trip.com seeing moderate upticks. India’s rise has been driven by the Financials sector. Specifically, 3 banks: ICICI Bank, HDFC Bank and Axis Bank.

AlphaMena

PGH’s share price has been in a downward spiral since Apr 21, losing >40%. However, its financial performance has been solid. FY23 revenues increased 6% to TND4.07bn, boosted by a dynamic local market in Q4, while the core group businesses - Poultry and Food - saw revenues up 12% and 8%, respectively. PGH boasts a strong balance sheet structure despite its high gearing and the company's 2023 ROCE of 8.9% was respectable. The group will do better in terms of return on assets when the economy picks up again, but there is significant room for upside (60% discount to NAV) even if the household consumption recovery expected in 2024 is pushed back again. TP TND14.2 (95% upside).

Galliano's Financials Research

Victor Galliano reviews 6 large and mid-cap Indonesian commercial banks on the back of recently announced 4Q23 results to identify those that are attractive value, have good earnings growth prospects and have the potential to deliver higher returns. BMRI is his top pick for its quality attributes, its premium and growing pre- and post-provision returns; it also provides a better valuations to returns mix than Bank Central Asia. Bank Negara is his value pick with its low PE multiples, its attractive PEG ratio, whilst also improving pre- and post-provision returns with cost of risk well controlled.

Macro Research

Developed Markets

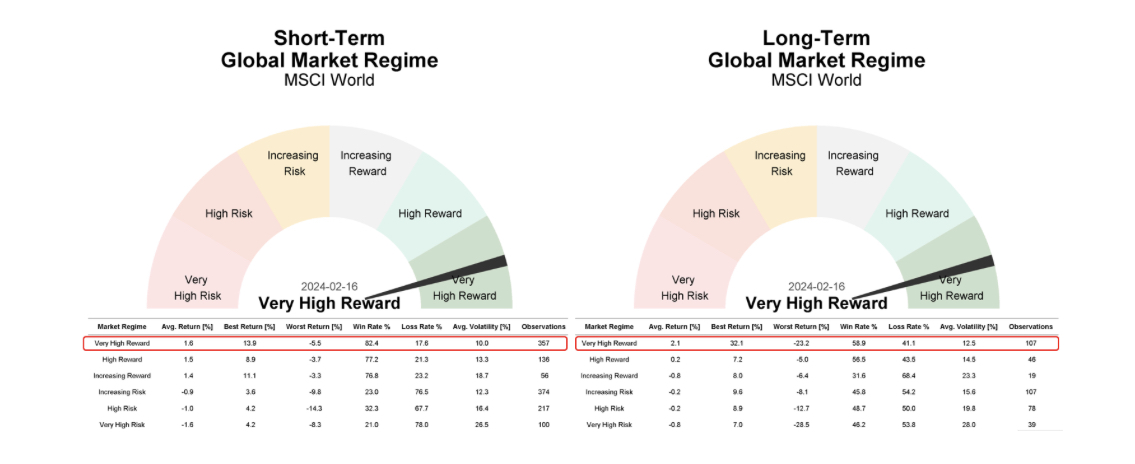

WallStreetCourier

Bullish brilliance: Positive outlook on the MSCI World still persists

Since WallStreetCourier emphasised the “very high reward” market regime in mid-Dec, the MSCI World has surged by 6%. This positive market regime continues to be supported by robust signals from 1,500 indicators across 26 major indexes and sectors. Their data reinforces the expectation for a sustained continuation of the global bull run, with all Market Health indicators displaying robust signals. Historically, the MSCI World demonstrated gains in 82.4% of all cases when operating within a very high reward market regime.

DayByDay

A new era for equities

With China and commodities trying to bounce, we may come to a new era for equities, with long-term laggards catching up. This is what happens in a medium-term bullish trend when passing the previous record. The stocks that led the way up need a break, while those that have been out of fashion can support indices. It does not happen very often, but the current juncture has the necessary characteristics for such a rotation. It will extend over several weeks (perhaps around 4-12 weeks). This can happen providing bonds are stable and the short-term trend suggests just so. The USD may fall, but this is a logical conclusion and there is no such signal yet.

Greenmantle

UK: History and Labour

The UK’s opposition Labour Party continues to hold a commanding lead in the polls over the governing Conservatives. While past incumbents have usually narrowed such gaps, Prime Minister Rishi Sunak has so far failed to reverse his party’s slide and faces a historically steep uphill battle in the year ahead. Labour’s decision to avoid bold policies, most recently exemplified by its U-turn over a £28bn-per-year green investment plan, may not inspire voters. However, it also minimises criticism of the party and places the focus squarely on the Conservatives, who will be left to defend their poor record on the economy. Niall Ferguson maintains his base case of a Labour majority at the next general election but expects a narrowing in their poll lead as the date approaches.

Harlyn Research

Keep an open mind on Europe

Simon Goodfellow has several indicators which suggest that Eurozone equities could be about to generate a positive surprise. His euro-denominated asset allocation model has upgraded global equities to overweight, chiefly because of some emerging weakness in German bunds. It is now more bullish on global equities than its dollar-denominated counterpart. Simon’s global equity models still have the US as an overweight and the Eurozone as a neutral. There is only limited upside for the US but a lot more for the Eurozone, which has a much stronger uptrend and a better leading indicator. The positive mood is not yet supported by survey or hard economic data, but markets always move before this is published. Simon urges investors to keep an open mind about Europe, particularly Germany and the Eurozone.

High Frequency Economics

Canada: Set up for a cut

On 20th February StatCan reported a slowdown of consumer prices to a 2.9% rate of increase. Carl Weinberg points out that the details are even more impressive. CPI basket shelter prices were 6.2% higher than a year ago. Given the 28% weighting of the shelter, the CPI basket other than shelter must have increased by just 1.6% year-over-year - less than the 2% inflation target. In Carl Weinberg’s view, the Bank of Canada can now justify easing monetary conditions and Canada is now at the top of those economies that could cut rates first.

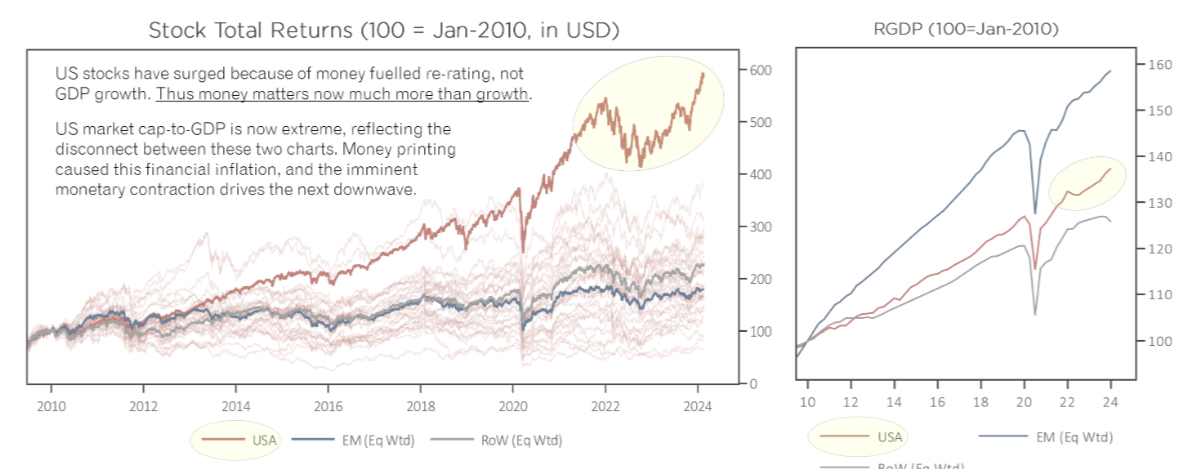

Totem Macro

US: The next downwave

Whitney Baker comments on how 25yrs of central bank pricing in US and China drove once-in-a-generation bubbles in both place. The result is that assets have become tethered to central bank flows, rather than economic outcomes, and the huge size of the bubbles mean that central banks must slowly withdraw liquidity to avoid asset collapse. The market action through the unwind follows violent ups and downs, just like in 2020, but Whitney warns that this no-return volatility provides a smokescreen that hides a sideways lost decade or so for real returns on dollar assets, as economic cashflows inflate into them. This brings us to the US right now, where the pace of the Fed’s money creation is slowing fast and will start to contract in 2Q24, ushering in the next downwave in US assets. The most important thing is not US growth, it’s US liquidity, because that money disconnected asset caps from the economy and is alone sufficient to lead to a tactical bearish inflection.

Underlying Inflation

US inflation in the medium term

In this note, the Underlying Inflation team revise their forecast after putting 2024:Q1 and 2024:Q2 in-sample. The bottom line is that the medium-term models have converged towards the estimate of pi*: 2.5% in core PCE space. At this point, this forecast is unlikely to change substantially in the next few months, and the risks are well balanced. Returning to the Fed target is still a question mark. Now that the team have a better understanding of the current quarter, their main model is currently assuming that core PCE price inflation will grow 3.1% (QoQ saar) in Q1 and 2.6% (QoQ saar) in Q2. Underlying Inflation also assume that real GDP growth will be 2.5% (QoQ saar) in both Q1 and Q2, and that the unemployment rate stays flat. The forecast for core PCE inflation is: 2.8% (Q4/Q4) in 2024, 2.5% in 2025, and 2.5% in 2026.

Emerging Markets

CrossBorder Capital

Capital Wars: The battle for Asia-Pacific

Watershed moments in global financial markets keep coming. The latest reflux of international capital back into the US may represent a welcome deleveraging of global balance sheets, but it comes at a cost for others. In particular, China has suffered huge capital flight. These outflows have made it more difficult for China to keep the Yuan stable and so forced the PBoC to further tighten their monetary stance. In fact, persistently tight money over the past few years proves a better explanation of China’s economic plight than the increasingly popular ‘End of China’ narrative. Michael Howell says that China needs to devalue the Yuan; his target is RMB 8/US$. This will add turmoil to Asian currencies, renew disinflationary pressures and speed-up protectionist measures. A weak Japanese currency is part of this story because Michael believes the Yen has been weaponised and serves as the USD’s stalking horse.

East Asia Econ

Asia: Secular depreciation

The TWD and JPY appreciated rapidly in the 80s then gave up the gains in subsequent decades, a result of deflation, tech and household consumption. The consensus is that CNY is about to follow the same path at the behest of the same dynamics. Paul Cavey is sceptical that CNY depreciation is inevitable; in fact, he continues to argue that CNY strength is possible and desirable for China, which is needed to achieve rich-country per capita income by 2035 and to prevent the ever-rising-surplus, ever-depreciating model of Taiwan taking hold. There is also reason to think that the secular weakness of TWD and JYP is ending, with the former benefitting from good economic momentum and the latter from a tight labour market and recovering exports.

Your Weekend Reading

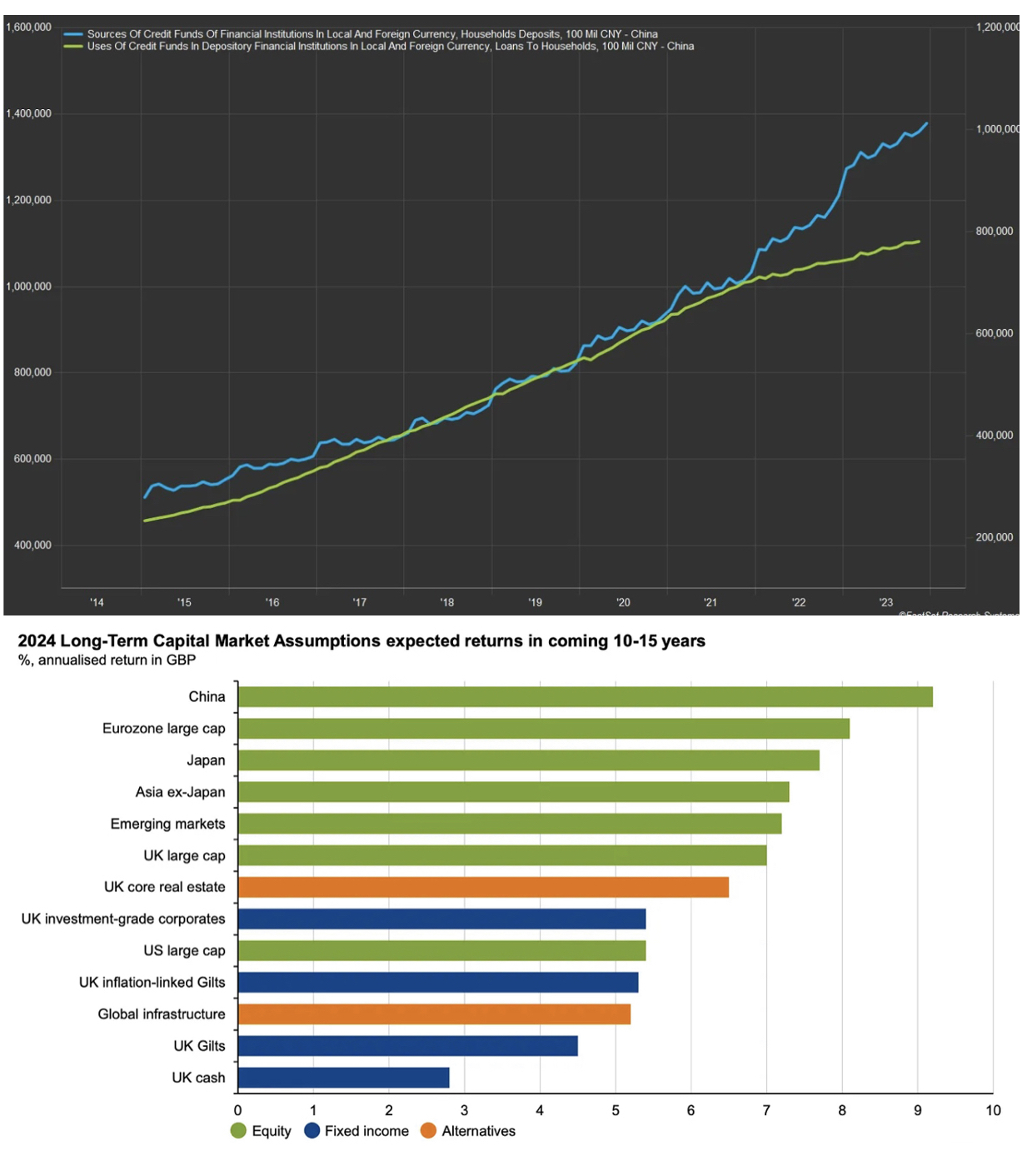

The surprise market for 2024

In 2009 China was on the ropes. The GFC was crossing the Pacific and they needed growth. The provinces went to their economic drawing boards and came out with bold promises of 9% growth for 2009. The market didn’t believe it was possible and was surprised when China boomed. Why is this relevant? Because it’s happening again. China’s provinces are pulling every lever to deliver 5.5% growth for 2024, the central bank has restarted QE, the Chinese consumer is delevered and sitting on record amounts of liquid deposits (chart 1), and Chinese equities have the highest expected return from current levels (chart 2). Meanwhile, investors are at maximum bearishness. Prepare for a surprise!

Greenmantle

Big Trouble in Big China

Since mid-2021, foreign and domestic investors have turned sour on China. As party officials struggle to stabilise the market, heads are rolling in Beijing; the turmoil reminds Niall Ferguson of the 2015–16 stock market rout, which was made worse by bungled policy and poor signaling to the markets. To stabilise the situation, Beijing is likely to respond more aggressively in the coming weeks, including with more significant share purchases and buybacks, more liquidity, and more restrictions on short-selling. Yet it is likely to move more cautiously on the fiscal front, with a small boost to fiscal and monetary stimulus at the lianghui in March. In the short-term, CNY should strengthen as Beijing tries to elicit more market confidence, but there is no light at the end of the tunnel in terms of a big macro recovery this year. Niall expects share prices to move sideways from here through year-end with some risks to the downside in H1.

Alberdi Partners

Argentina: First January surplus since 2011

The government posted a fiscal surplus of ARS518bn in January and a primary surplus of ARS2tn. This contrasts with a primary deficit of ARS140bn in January 2023 and is the first financial surplus for the month of January since 2011. While revenues rose above inflation at 256.7% yoy, due to higher export taxes and the Impuesto PAIS, primary spending rose “only” 114.6% yoy. Social security spending expanded by 125%, wages 158%, transfers to the private sector by 125.5% yoy and the ones to the public sector (mostly the provinces) 71.2% yoy. Energy subsidies dropped in nominal terms, which may suggest the government accumulated a debt with Cammessa, the energy wholesale company. Marcos Buscaglia believes the numbers are quite positive, yet they also show the temporary nature of the adjustment as pensions dropped in real terms due to the acceleration of inflation, but for the same reason they will increase above inflation once it starts to fall.

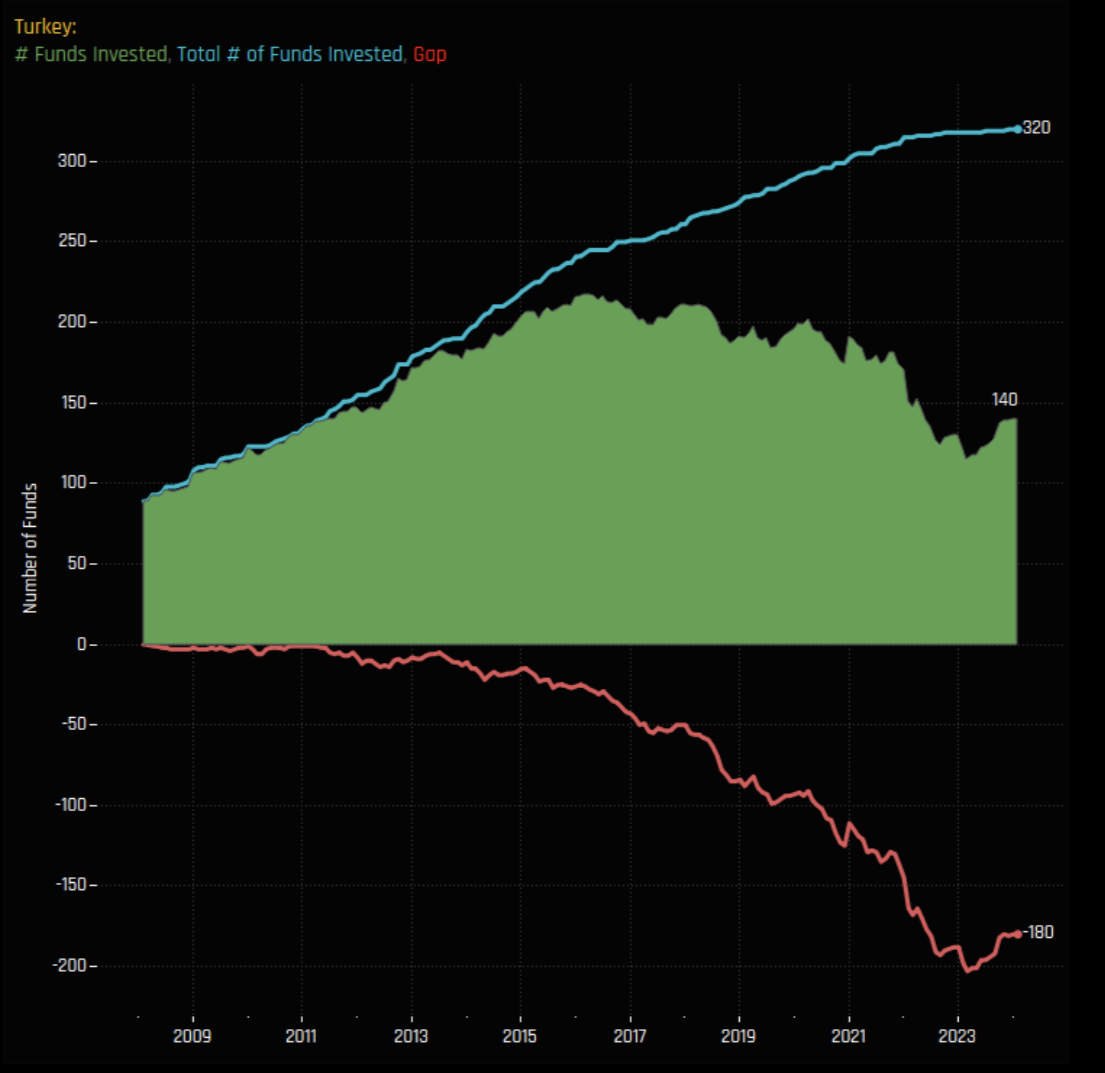

Copley Fund Research

Turkey: EM fund managers show signs of sentiment shift

After a decade-long bear market in investor positioning, GEM managers are beginning to show tentative signs of a sentiment shift towards Turkey. Over the last six months, a total of 121 funds increased their Turkish weights, compared to just 23 that reduced them. The Turkish investment narrative highlights two main points: firstly, a shift towards positive investor activity, and secondly, that current investment levels remain near historic lows. Chart 1 shows the total number of funds (out of 361) that have ever held a Turkish position (blue line), the number of funds invested at any one time (green) and the difference between the two (red). The country joins Saudi Arabia, UAE, Poland and Greece as EMEA countries benefitting from rotation.

ESG

GFC Economics

Climate change pushing up insurance prices

As extreme weather intensifies, insurers are pushing up premiums and dropping coverage in high-risk zones, passing the bigger bills onto homeowners. This mounting climate damage inflames political tensions. Meanwhile, clean energy tax credits in the US Inflation Reduction Act have seen estimated costs balloon to over $870 billion through 2031, more than double original projections. Accelerating the green transition is imperative but adds to price pressures. Higher investment in renewable power, AI, and related energy needs will keep real yields and term premiums lofty; the inflationary impacts of tackling climate change and advancing technology sustain elevated interest rates. Difficult trade-offs between urgent climate action and price stability are unavoidable as policymakers face a delicate balancing act between green progress and inflation control.

Verisk Maplecroft

Chile: ESG outlook amid wildfires and scandal

Chile's pioneering leadership in sustainable sovereign debt is expanding, with social bonds now comprising over a third of public debt. However, political and environmental risks cloud the investment outlook, which the Maplecroft team examines in their latest report. Leftist President Boric is struggling to boost lacklustre growth and pass reforms amid legislative defeats and corruption scandals. Devastating wildfires have raised concerns over lax zoning, poor disaster preparedness, and proliferation of flammable non-native trees. Analysts warn climatic changes are fuelling unpredictable fire extremes across South America that will take many years to recover from. Investors must weigh the country's ESG credentials against mounting political dysfunction and climate vulnerability; Chile may continue innovating in sustainable finance, but governance and environmental fragility pose challenges.

Commodities

View from the Peak

Trades that reflect excessive bearishness in agricultural commodities

There comes a time when positioning becomes so extreme and attitudes so bearish that it it becomes time to act, not just for a tactical trade but a structural realignment that better reflects balance sheets and punishes reckless sentiment. According to Paul Krake, that is where we are in agricultural commodities. Some of his recommendations include LONG a basket of soybeans, wheat and corn vs LONG US two-year notes; such prices will only continue in the event of a hard landing, which is hedged by the two year note position. Paul also recommends LONG wheat and SHORT cocoa as a purely financial trade, and LONG Nestle and SHORT General Mills and Kellogg.

CPM Group

The truth about silver demand and price

In a preview of the upcoming Silver Facts and Fantasies 2024, CPM Group's Jeffrey Christian goes through some of the fantasies in the silver, precious metals, and economic markets, as well as some of the things to which investors should be paying more attention. Jeffrey also discusses investor demand for silver products as well as the long-term sustainable price for silver.

Click here to watch.