Company & Sector Research

Europe

Pernas Research

No permanent impairment to the brand - DOCS has experienced a recent revenue decline driven by several short-term operational and inventory mishaps (now fixed) along with general cyclical challenges in the footwear category. Analysts at Pernas Research believe DOCS has an enduring appeal across genders, regions, cultures and socio-economics. They also argue that the market is currently discounting several growth opportunities. Pernas (conservatively) estimates FY25 will see a return to 1bn in revenue with an after-tax FCF margin of 9%. Revenue will then grow by 4-7% over the next 4-5 years with gradual increases in FCF margin. Their TP offers 60%+ upside.

Vision Research

Last week, Robert Prather pitched LPP as Vision's short idea at IRF’s latest Equity Shorting Conference. Key points include: 1) Loss of Russian growth opportunity (LPP’s fastest growing market). 2) Poland saturation. 3) Trouble growing in Western Europe (more expensive / increased competition). 4) Weak same store sales. 5) Management overpromising / underdelivering. 6) Quality of earnings issues. Robert’s presentation also includes commentary on the recent activist short report and management’s subsequent response.

Smart Insider

Ian Gallienne (CEO since 2012) buys €1.4m of stock at €69.33, increasing his stake by 67%. He has been a rare buyer with only 2 purchases in the last decade, he bought €294,000 of stock at €58.78 in Mar 20 which was perfectly timed and a further €398,000 at €79.50 in Sep 20. It's notable to see him now make his largest purchase nearly 4 years since he last bought stock. It's also the first trade by any insider for 2 years. Stock Rank +1 (highest rating).

Iron Blue Financials

SGO’s Iron Blue score increases to 26/60 (newly top quartile / fertile grounds for shorting). This reflects an expanded gap between PPE capex and the P&L depreciation charge (14% of PBT adj, vs. 11% and 7% the two previous years) and another increase in receivables factoring (+6% y/y, +40% since FY20). Stripped out one-off costs remained elevated (10% of FY23 PBT adj). A new contingent liability was named in FY23 concerning competition authority investigations into the additives and admixtures sector in the EU, UK and Turkey, while class actions were instituted in the US and Canada. SGO has also continued to consolidate its Russian operations despite seemingly operating independently from the rest of the group. Iron Blue calculates that €112m of gross cash was stranded in Russia.

Ben Jones Investments

KMR is a mineral sands miner that has operated the Moma mine in Mozambique since 2007 and is the world’s third largest producer of titanium feedstock. 2023 was KMR’s second best year after the record year in 2022. It remains in the first cost quartile with over 100 years of remaining mine life, which maintains its competitive advantage. Ben Jones thinks the downward pressure on the share price in a response to a large capex programme over 2024/25 has been overdone. Once the capex programme is complete, he expects to see KMR generating ~$100m FCF p.a. This would represent a 30% FCF yield on its $340m market cap.

North America

Trivariate Research

When the management gets weaselly…

Trivariate has scanned through all the earnings call transcripts for the top 3000 US equities since 2017 and counted the occurrences of "weasel" words (i.e. words associated with uncertainty, such as “maybe”, “could”, “almost”, “sometimes” and “depends”) in the answers from the executives on these calls. Trivariate found it to be an effective signal in distinguishing winners from losers in the lowest quality quartile of their substance model (“Junk”). The return differential between Junk stocks with declining usages of weasel words vs. those increasing their quarterly usages has generated a 50% cumulative return since 2017. This figure climbs to 85% when combining Value and Junk stocks.

Value / Junk stocks that have recently used less weaselly language (Buy ideas) include Truist Financial Corp, Stanley Black & Decker and OneMain. Sell ideas include Annaly Capital Management, AGNC Investment Corp and Zions Bank.

280First

10Q / 10K filings analysis

Utilising AI, NLP, data analytics and qualitative analyst oversight, 280First can rapidly glean material / actionable insights from a company's financial reports. Recent alerts include: 1) Assured Guaranty - caution on liquidity claims; colour on impact from downgrade of financial strength. 2) Burlington - more positive views on comparable store sales. 3) Dollar Tree - may need to lower prices to remain competitive. 4) Keysight Technologies - seeing order cancellations? 5) Mattel - no longer focused on advancing e-Commerce and DTC business. 6) Salesforce - rethinking level of additional growth opportunities.

Hedgeye

Fire without the smoke - 3 consecutive years of HSD% organic revenue growth with positive volumes ranks among the best in class in Consumer Staples. Yet PM trades at a modest 15x PE and offers a 5.5% dividend yield. The non-combustible portfolio reaching a tipping point for the company’s profitability and growth will trigger the re-rating, according to Hedgeye. They see the potential for the shares to deliver a 25% compounded annual return from EPS growth, multiple expansion, dividends and deleveraging. That would lead to shares doubling over a multi-year duration in most economic scenarios. Investors who cover Staples can't afford not to own this stock.

Churchill Research

E&P ranking model appears to be working

Mike Churchill only developed this model in early Jan but is pleased with the results so far. The E&Ps that scored better than average back in Jan have performed 11 points better than those rated below average (+28% vs. +17%) over the last 12 weeks. Interestingly, all the stocks with a 40%+ gain were in the better-than-average group (Riley, Vaalco, Valeura, SM Energy and Ring Energy). During this process, Mike also noted that certain meta-themes became apparent including how Permian plays seem to really generate wealth (they don’t just recycle capital endlessly without benefitting investors) and Canadian domestic E&Ps often have a problem with creating wealth over time.

Portales Partners

Bank stocks up sharply in 1Q24 but earnings declining - hope springs eternal

Charles Peabody has been an ardent bank stock fan since a power shift last autumn but is getting queasy as some valuation thresholds are being reached. Last month, large cap banks sharply outperformed, rising 9.6% over 3x the SPX increase. Importantly, there was wide divergence around this number and there seems to be a mix shift favouring banks with balance sheet risk vs. non-bank financials. While earnings reflect declining revenues and rising credit costs, there is hope that these trends reverse in 2025. Unfortunately, Charles suspects that there will be little evidence to support this optimism when Q1 earnings commence. His strategic position is bullish as banks transition into a position of market leadership but tactically is bearish as near-term earnings come in weak.

Thompson Research Group

Building Product Distributors still offer plenty of upside

Many market participants are looking for a way to play housing and it would be easy to look at building product distributors and write them off as being overvalued and that you’ve missed out. However, TRG believes this is faulty logic. Builders FirstSource, Beacon Roofing and GMS (as well as others) have margin profiles that have risen to comparable or superior levels in relation to the “premium-valued group” (SiteOne, Pool, Leslie's, Core & Main and Ferguson), but have EV/EBITDA multiples (avg. 10.6x) well below these stocks (avg. >20x). If they gain a more appropriate multiple (for strong SF starts and better margins) on higher EBITDA, then all three companies still offer significant (~70%) upside.

Sales Pulse Research

Broadcom's uplift in pricing shocks VMware users

SPR provides recent field feedback on AVGO’s actions, users reactions and vendors who are benefitting. While many acquisitions do not produce the increases in revenue and cost synergies that were promised, based upon AVGO’s aggressive approach, SPR expects it will immediately deliver strong results for both metrics. Despite the disruption and animosity it is creating, SPR is picking up many examples of end users who are paying much more to AVGO then they were prior to this acquisition (price hikes of 100-1000% have been reported). These end users are locked into some or all the VMware products. The cost of switching is very high and, in some cases, will take years. Other vendors discussed include Nutanix, IBM Red Hat and HashiCorp.

Off Wall Street

EV/Sales multiple has doubled in the past year - Nvidia’s initial choice of FN to make 800G InfiniBand transceivers for its GPUs has led investors to perceive the company as a secular AI growth beneficiary. OWS thinks this is a misperception. Ethernet appears to be gaining on InfiniBand and is likely to supersede it as the standard AI networking technology. Competition for 800G+ transceivers for AI applications is likely to increase and lower FN 800G+ transceiver market share. Furthermore, widespread selling by insiders in the past few weeks suggests that they may not share bulls’ enthusiasm for the firm’s prospects. TP $131 (30% downside).

Arete Research

Market value does not reflect the steep reduction in sales, more limited end-markets. U’s interim CEO has taken swift action, shedding low margin Create Solutions sales and disclosing abnormal ironSource revenue, yet the “new” company’s sales and FCF generation is now materially smaller. Grow Solutions sales fell sequentially in 2H23 and needs to invest in tech and resolve execution issues - all whilst cutting costs, changing management, opposing competition and navigating platform policy changes. Arete forecasts $100-200m Adj. EBITDA shortfalls vs. consensus estimates out to 2026E. TP reduces to $16 (40% downside).

ETR

Is AI spend impacting the RPA sector?

ETR’s latest Gen AI survey indicates that budget to fuel AI ambitions is being reallocated from elsewhere (vs. newly added budget). In addition, preliminary data from their Apr 24 Technology Spending Intentions Survey shows a stark divergence in Net Score momentum between ML/AI and RPA. The y/y Net Score declines are squarely focused on three vendors: UiPath and Automation Anywhere, with whopping 18 ppts and 24 ppts Net Score declines y/y, respectively (along with Blue Prism’s 24 ppts decline, with a lower citation count). Microsoft Power Automate and Pegasystems are notably stable both y/y and sequentially from Jan, with Appian the only vendor seeing significant Net Score momentum to the upside.

Japan

Astris Advisory Japan

Telecoms: Valuation upgrades

FY23 has so far been a goldilocks scenario for Japanese telcos. Incumbents are moving closer to a recovery in high-margin, mobile service revenue growth with little competitive trouble from Rakuten Mobile despite it managing to grow subs by tapping under-served corporate users. While Kirk Boodry expects competitive intensity to step up in FY24, there are limits to how aggressive Rakuten can be and his positive outlook on the sector has not changed. IIJ is his top overall pick. He also moves KDDI ahead of NTT as his preferred large-cap telco.

Galliano's Financials Research

The shares have re-rated but remain attractive given Rakuten Bank's strong balance sheet and low-cost base with undemanding valuations compared to its Asian digital banking peers. The bank is well positioned to benefit from the negative interest rate policy exit in Japan, with its low LDR, high cash balances, growing loan book and healthy capital ratio. It continues to leverage off the Rakuten Group eco-system, as a low-cost source of new customers; nearly a third of clients use Rakuten Bank as their primary Japanese bank.

Azabu Research

Trades at less than half the TOPIX multiple and generates nearly twice the average ROE. OHG has grown sales at a 25% annual clip during the past 5 years, despite declining house starts, because of overwhelming pricing advantages. The consensus believes these advantages have suddenly disappeared and projects earnings to flatline indefinitely. However, Mike Allen sees an inventory correction that may already be completed but will inevitably end without having any long-term impact on the company’s position. He expects cash flows from operations to exceed capital requirements by >¥500bn in the next 5 years - an amount that exceeds current shareholders’ equity. Mike sees fair value at ~¥17,000, nearly 4x the current price!

Emerging Markets

Horizon Insights

The company’s trajectory, marked by a blend of user engagement, content diversity and strategic foresight, remains significantly undervalued by the broader market. Bilibili's ability to maintain user growth with minimal marketing investment underscores a strong user stickiness and a sustainable and thriving content ecosystem, that has untapped potential for commercialisation through increased ad revenue. The strategic recalibration in its gaming sector, coupled with nuanced advertising strategies, signals robust growth prospects for 2024, reinforcing Horizon Insights’ bullish stance on the stock. Furthermore, the embrace of AI technology not only aims to enhance user experiences but also to unlock new commercialisation frontiers.

Tabbush Report

BMRI's image needs updating. It is expanding its loans strongly, despite its size. Its credit metrics are improving dramatically. Daniel Tabbush sees this with some of the best NPL decline in the country and also now with strong credit cost reversals. With much lower Loss NPLs and far higher NPL coverage than in the past, benign credit costs can continue. NIM may be lower but this can mislead where the credit focus is on higher quality loans. Operating costs are improving substantially, while the bank’s funding structure is also improving. ROA expansion continues, with BMRI seeing higher returns than in any period of the past 10-15 years. Daniel believes this can continue or improve further.

Macro Research

Developed Markets

Belkin Report

Investors' misguided psychology

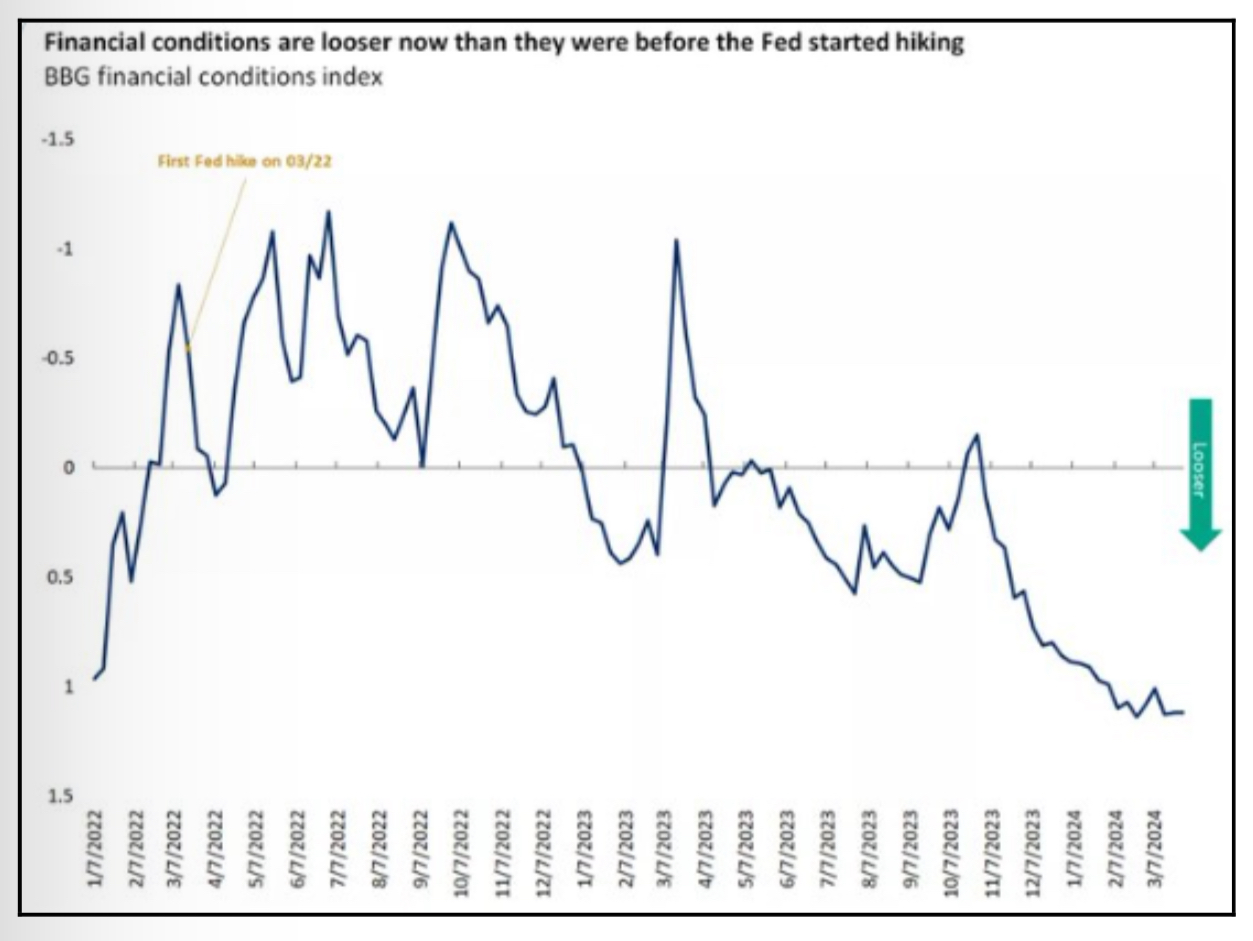

Michael Belkin welcomes the recent newfound interest in energy stocks, remaining LONG as sentiment is yet to reach excessive levels. Meanwhile, investors keep pouring money into US and global equities. One reason is the looser financial conditions (see chart), but Michael posits that market psychology is the key reason, with investors and portfolio managers conditioned to believe that Fed interest rate cuts are bullish across the board. But what if the Fed is completely wrong on inflation? Michael’s model, which forecasted the 2022-23 decline in CPI from 7.7% to below 3%, has completely reversed, suggesting that no interest rate cuts lie ahead. Investors have been eating dessert based on misguidance from the Fed, with commodity markets going nuts. Watch out when the bubble is punctured.

Ekins Guinness

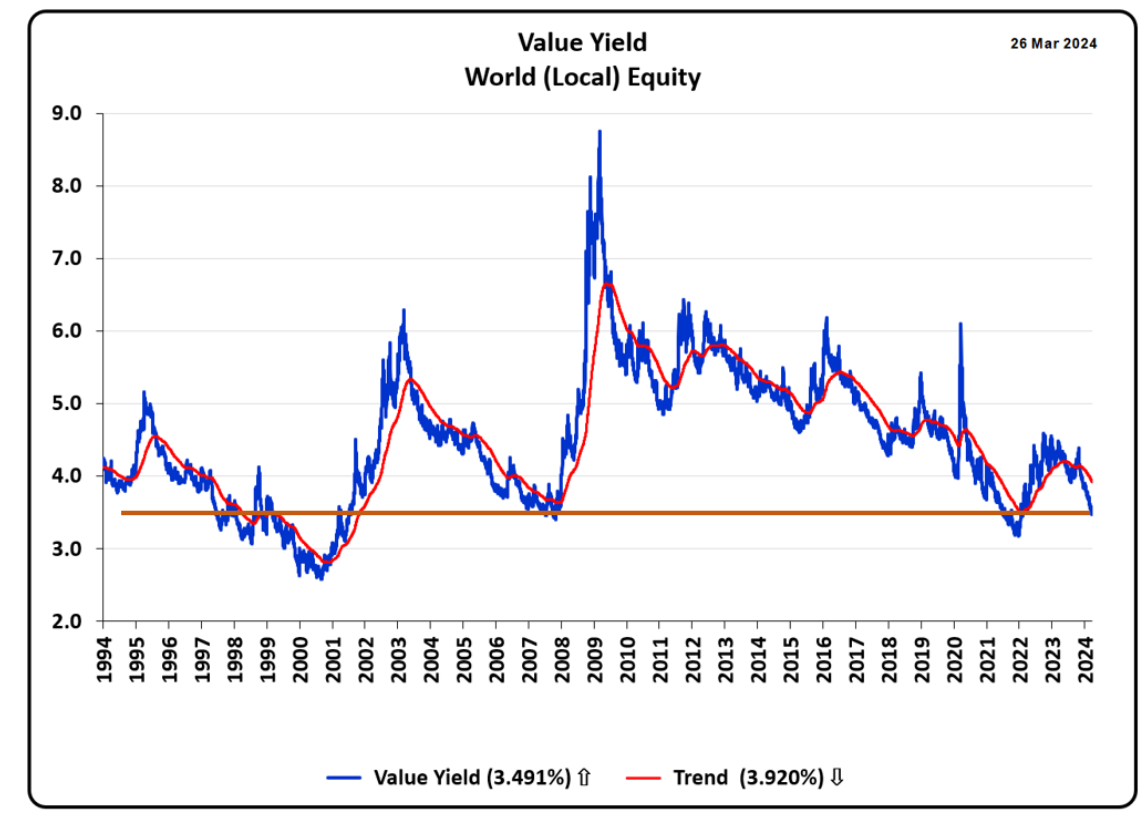

Worries over equity valuation

Following the strong equity rally since October 2022, the world equity market value yield has fallen to a level at which the Ekins Guinness team’s model starts to worry. However, it is some way off from being at dangerous levels. The whole point about long term investing is that one should ignore temporary corrections in an ongoing bull market, but it can be tricky knowing the difference between simple noise and actual bear markets. The model therefore, once in the warning zone, accelerates the reduction in equity allocation as price trends turn down, but this has not kicked in yet. Investors should be ready to start a gradual reduction in equity exposure if the model falls further, moving more quickly if sentiment deteriorates.

CrossBorder Capital

Another major policy error is coming

US bond markets are pricing in around ‘3½’ cuts in US policy rates over the next 12 months. This looks generous given latest evidence of economic acceleration. Nonetheless, the message from Fed Chairman Powell is that US policy rates are at a peak and will likely be cut this year. In short, Michael Howell claims that policy makers are set to ease into an accelerating economy. Whoops? A problem is building for 2025 as central banks will be forced to hit the brakes. Term premia and bond yields look set to rise further, stick with risk assets and avoid bonds.

WallStreetCourier

Has the bull market gone ahead of itself?

The MSCI World has surged by 28% since late October, with no pullback exceeding 3%, prompting concerns that the rally may have gone ahead of itself. Despite these impressive gains, WallStreetCourier’s data currently provides no evidence of an imminent correction. The strong uptrend continues to be supported by robust signals from 1500 indicators across 26 major indexes and sectors covering trend, trend quality and smart money positionings. This fact continues to confirm their positive outlook on the MSCI World, which they covered multiple times last year. Throughout history, the MSCI World (MXWO) saw gains in 84.6% of instances during short-term 'Very High Reward' market regimes and in 70% of all cases during long-term ones.

Eurointelligence

The name’s Bond, Eurobond

Wolfgang Münchau has long advocated for eurobonds, but he is becoming increasingly nervous about the kind of company he is keeping. Recent debates over a possible EU-debt financed security spending differs from the purpose of using eurobonds for political unification, with sovereign debt occurring as a result. Such an instrument cannot exist without the powers to raise taxes that could cover debt servicing costs, which will not happen for as long as the EU depends on its member states for its finances. If we’re going to get close to bringing it to reality, significant treaty changes would be a necessity.

Greenmantle

Japan: Renewed optimism

The Bank of Japan started normalising its monetary policy in March, raising its overnight call rate to 0-0.1% from its negative lower bound of -0.1%. The first rate hike since 2006 followed wage increases and signals the BoJ’s increasing optimism that Japan is on course for sustained nominal growth and a virtuous cycle of price and wage increases. Given the Bank’s previously short-lived attempts to escape the zero-lower bound, Niall Ferguson expects any moves to be cautious, He expects a 0.25% rate hike by October, after which it will then be forced to pause by goods disinflation. Niall is neutral on the yen, given tactical risks from currency intervention, and is LONG Japanese equities.

Independent Strategy

Japan and the yen: Beware idle days in April

David Roche thinks Japanese authorities are close to the point where they must intervene to halt the yen’s downward spiral. Everyone is short. The yen remains the cheapest currency in the world and the market believes a more radical tightening of monetary policy would change that. David’s technical charts point to 160Y to the USD if the yen breaks the Y151/USD barrier. The downward spiral risks undermining BoJ strategy, hitting consumer income through high import prices and incentivising saving. Currency intervention and another rate hike are the likely tools.

Global Macro Technical Thoughts

Flash crash? Stay in cash

Jitschak Nager points out that gold and the stock market keep making new highs. It is alarming and Jitschak is putting out a warning signal that a flash crash is around the corner. He acknowledges that he could be wrong and be misreading the markets, but he prefers to be cautious with any long positions in Indices / Equities. As always, he refers to the levels for direction and technically the buy signal in ES is not yet cancelled. However, there are times that it is better to stay in cash than to try and take out the last few percentages in the already overinflated stock-market. He expects a 20-25% stock market correction from current levels in Q2/2024.

Radio Free Mobile

The pin that bursts the AI bubble

Roughly $50bn has been ploughed into an industry that has generated $3bn in revenues, yet most participants show little concern over how proper returns on these investments will be made. Richard Windsor sees the real return on investment in AI being made in terms of productivity and lower costs, but this is not what is being priced in. Instead, the market believes we are well on the way to creating super-intelligent machines that will take over most economic tasks from humans. Many generative AI services are pricing their services at ~$20 a month, an unrealistic price in the face of growing competition and free models, and other cracks are showing. It is only if we are on the cusp of super-intelligent machines that the current hype and frenzy can be maintained.

Emerging Markets

Emerging Advisors Group

The big EM high-stress rally

High-stress sovereign spreads have declined sharply over the past two quarters, despite “boring” markets in other EM classes. Jonathan Anderson contemplates what’s going on. He says part of the rally is due to funding support and due to global sentiment, the former a result of IMF and bilateral donor support exceeding expectations and the latter a consequence of lowering global volatility. However, EM stress cases have not resolved underlying macro imbalances; dollar earnings capacity remains weak, market debt burdens have not fallen, and overall external liabilities continue to rise. Spreads and yields are now more exposed to bad news at the margin and Jonathan sees the rally as a good time to take profits.

PRC Macro

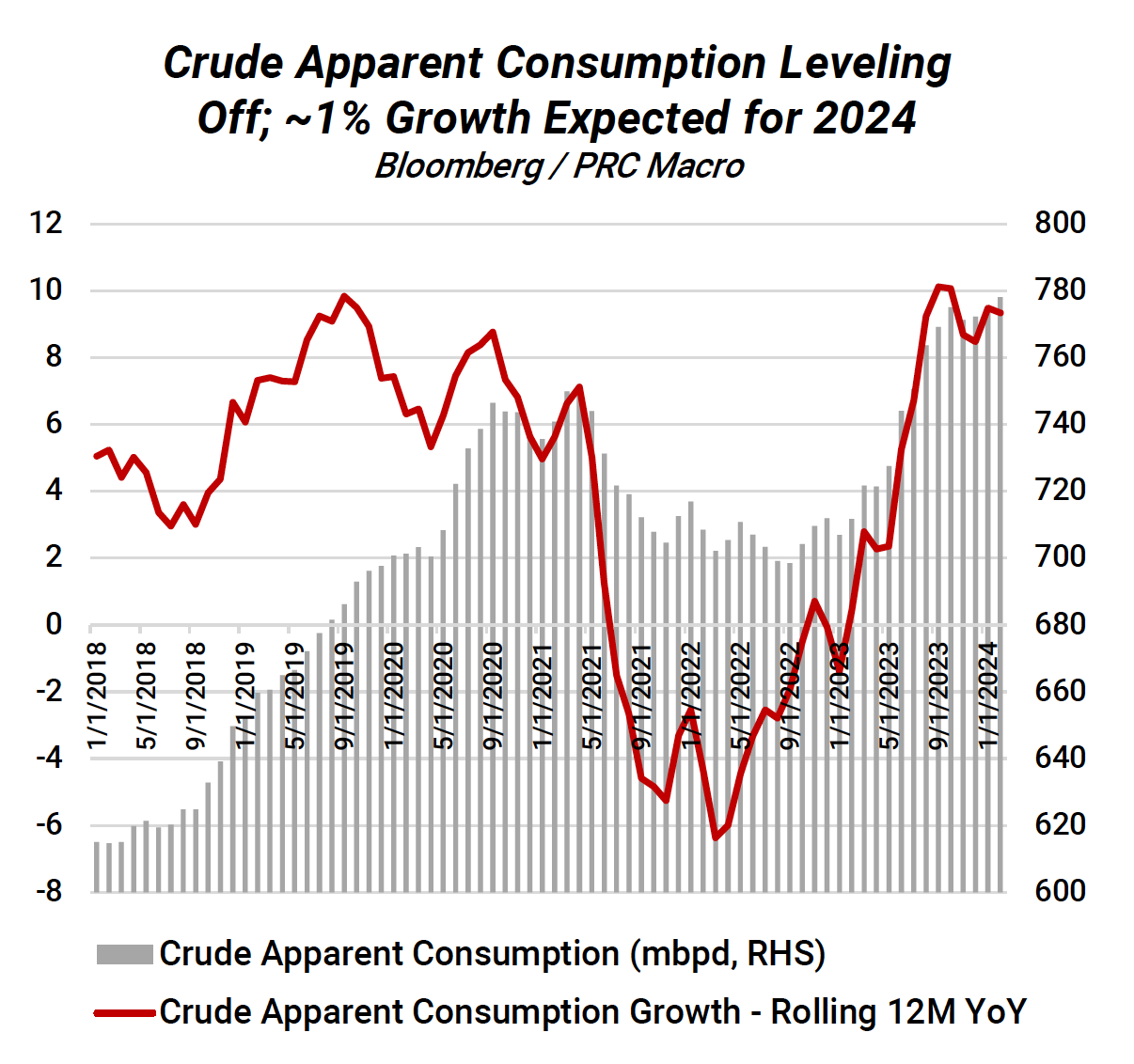

Peak domestic crude demand expected in China

Strong holiday travel data in China sparked debate as to whether this would lead to a sustained recovery for domestic crude demand. William Hess doesn’t think so and advises investors not to mistake seasonal crude restocking and imports as a sign of strength. The recent crude inventory drawdowns are larger than normal, reflecting weak demand expectations on a cyclical basis, a secular domestic view that peak crude demand is nearing and a reduction to teapot operating rates. The coincidence of peak crude demand in both China and the US provides an interesting long-term set up for USD/CNY, especially with markets underappreciating the petrocurrency characteristics of the USD and China’s involvement in the global energy transition.

Teneo

Nigeria: Rising currency, simmering tensions

The CBN’s (Central Bank of Nigeria’s) battle to bring inflation under control is producing mixed results. The appreciation of the naira represents a boon for President Tinubu’s government which has faced recent heavy criticism over decisions that have resulted in a rapid increase in inflation. With the early sings of exchange rate stabilisation likely to go a long way to silencing critics and placating public anger, the CBN will not yet be likely to change policy trajectory and will be seen as a critical player in helping the government achieve its critical political objective of maintaining public order.

East Asia Econ

Taiwan: Still no manufacturing recovery

Taiwan’s industrial sector has been contracting for 22 months, the longest recession on record. Yet the overall economy hasn’t ailed all too much, propped up by non-manufacturing and services; the non-manufacturing PMI has seen its 21st consecutive month above 50, its longest sustained period of expansion on record since the survey started in 2014. Paul Cavey doesn’t see this momentum lasting. The fall from 55.4 in February to 53.5 was relatively pronounced and indicates that the softening is underway. However, there are signs the long-awaited manufacturing recovery is starting, with decent increases in new export orders and backlogs.

Greenmantle

Ukraine: In the face of war

Greenmantle spent a week in Kyiv speaking with Ukrainians engaged in the war effort, from front-line soldiers to defence analysts, from charity volunteers to war widows. Optimism has waned since the birth of the war, but the situation is better than headlines suggest. Ukrainians are psychologically prepared for a long war and the country’s armed forces retain the ability to fight a spirited defense in the face of material constraints. Ukranian strikes into Russia may have ruffled Washington’s feathers, but there is little they can do to induce cooperation with aid stalled in Congress. Ukraine may be unwilling to capitulate, but there are signs the Russian governing elite are equally obdurate.

ESG

Verisk Maplecroft

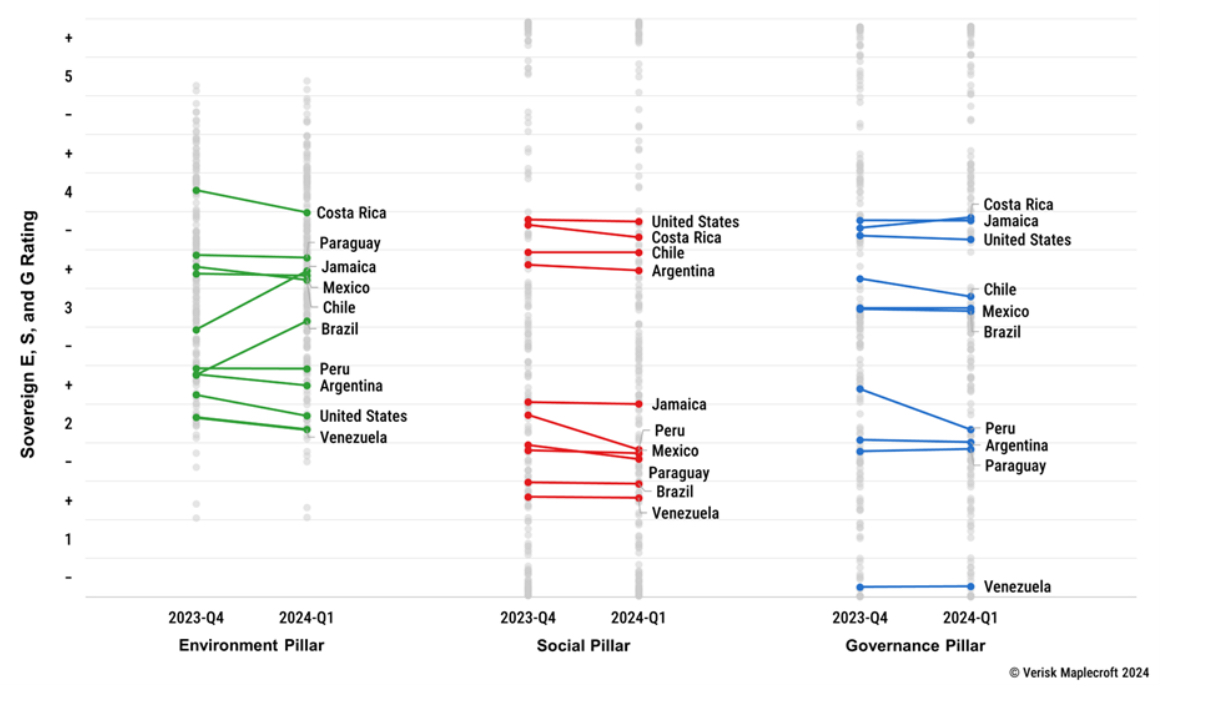

In the Americas, progress is stalling across E, S and G pillars

Overall ESG progress in the Americas remains stalled amid troublesome social and political trends in the form of weaker human rights protections and rising civil unrest. Overall, 22 countries in the region saw their scores slide in Q1/2024, with just 5 seeing improvement. Key improvers included Jamaica, benefitting from a narrowing emissions gap and strengthening government effectiveness, and Brazil, which has seen better Transition Risk performance under President da Silva. Worse performers include Peru, Paraguay and Costa Rica, despite the latter often being a regional outperformer.

Commodities

Global Mining Research

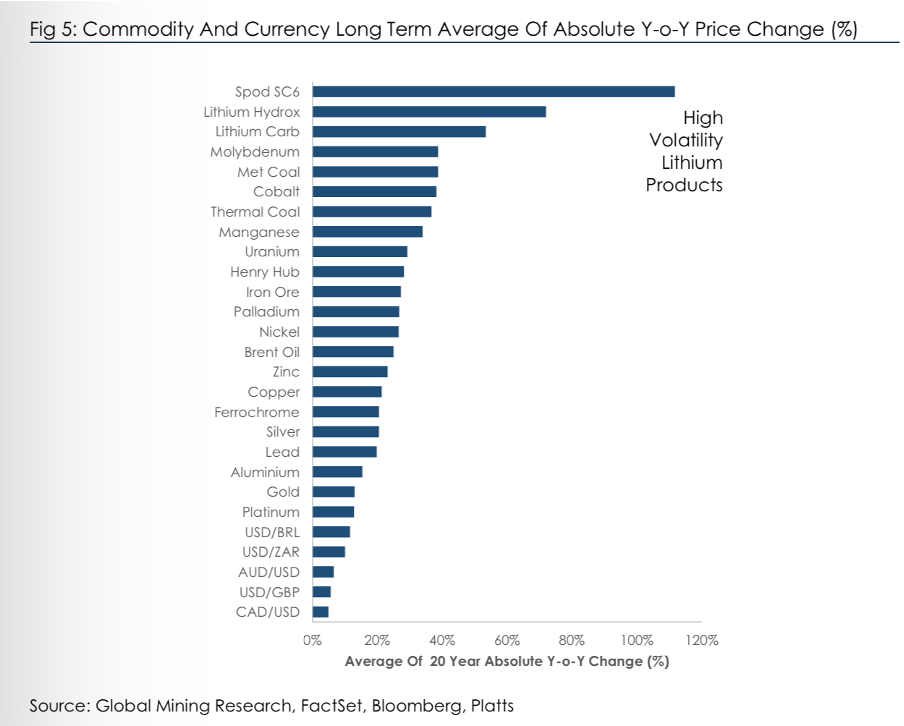

Lithium: Signs of cycle troughing

The last 12 months have marked a complete collapse in lithium pricing from all-time highs. The commodity is marked by short and sharp cycles (see graph) and David Radclyffe sees evidence that investors should increase exposure: product prices are stabilising, production curtailment is underway, EV demand growth is continuing, and seniors are raising equity (like in 2021). Low prices should make Boards more cautious when it comes to adding new capacity. Having been underweight for some time, David now sees opportunity in lithium equities with preferred stocks including Pilbara Minerals and IGO.

CPM Group

Why investors are rushing to gold and silver

Jeffrey Christian of CPM Group discusses the remarkable surge in precious metal prices, particularly gold, which reached new record highs. He highlights the consistent rise in gold prices over the last few trading days and throughout March, focusing on the increase to both long-term and short-term investors entering the market. He also touches on the economic backdrop against which these price movements are happening, noting strong GDP growth in several countries.

Click here to watch.

Veritas Investment Research

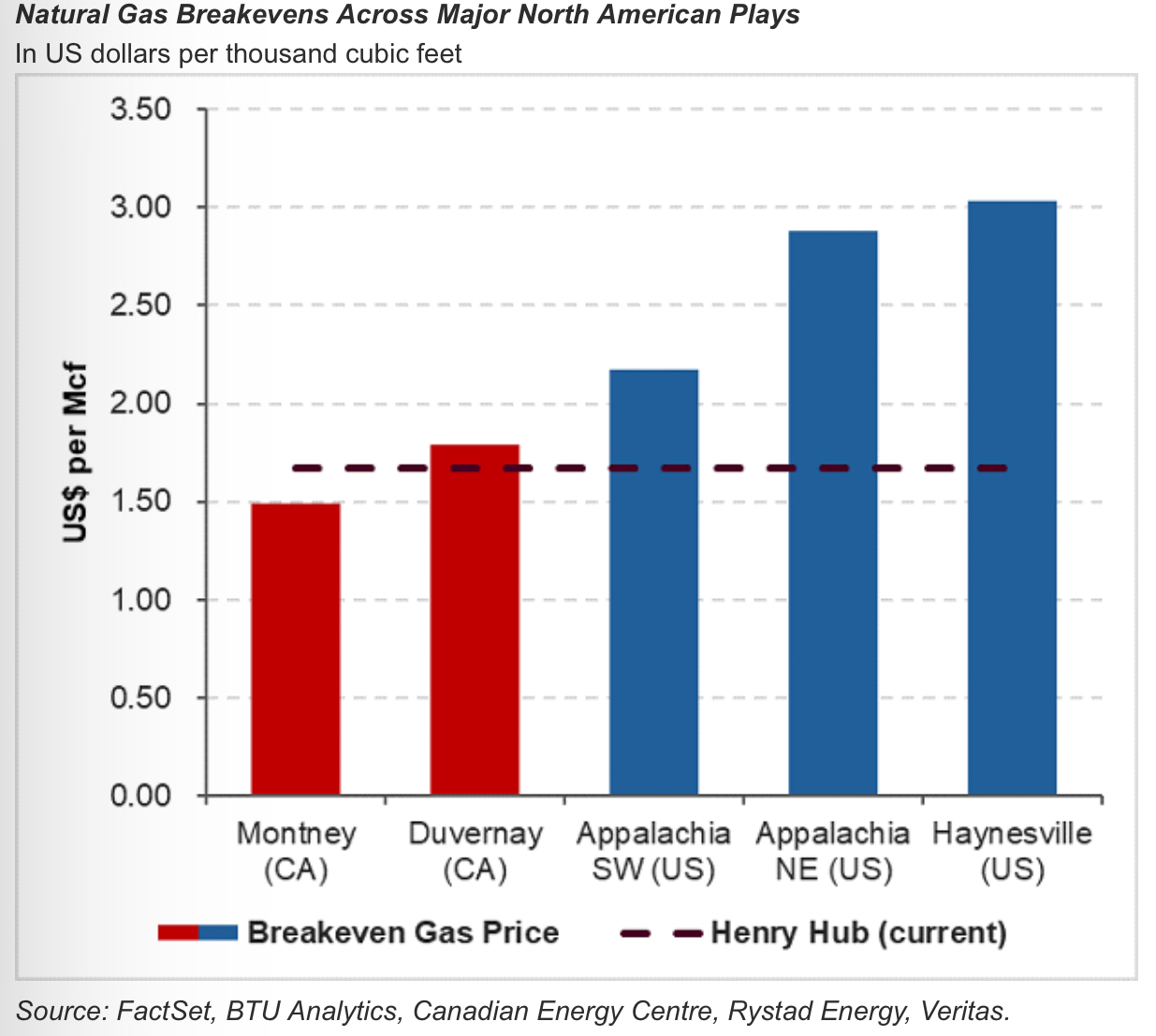

Feeling gassed

Natural gas prices have traded below US$2.00/Mcf for over a month, with current levels representing multi-decade lows on an inflation-adjusted basis. Producer profitability has been tested. However, the Veritas team point out that not all nat gas plays are built the same and breakevens vary across basins (see chart), with the Canadians having a wider margin of safety. The team see many US producers likely capitulating in the face of lacklustre returns across their portfolios. Longer-term, favourable economics, liquids-rich nature and a stronger USD could position Canadian producers as attractive M&A targets. Favoured plays are Tourmaline Oil and ARC Resources given their strong operations, broad hedge books and appealing liquids-rich growth prospects.