Company & Sector Research

Europe

Forensic Alpha

New accounting and governance red flags

Forensic Alpha is a machine intelligence system that is able to scan through a company's filings, extracting relevant accounting and governance data. Their technology works by translating unstructured data found in the notes to the accounts and governance disclosures into structured data. They then process that data, searching for the presence of common red flags that are known to be indicators of weak fundamentals and / or imminent problems. 147 new company filings were processed in the past week across Europe. 29 companies saw significant new red flags. While this report focuses on Nordex (Contract Assets, Ageing of Receivables, Related Party Transactions), other stocks highlighted include Hellenic Telecommunications, Ubisoft, Merck KGaA and Hapag-Lloyd.

Woozle Research

Woozle downgrades the stock to Sell following their latest channel checks. Volumes declined by 0.5% on average in 4Q24 with prices up 2% Y/Y. Within RI's portfolio its Rum category performed the best. This segment’s success was attributed to consumer interest in premium products and the solid growth of Havana Rum. Conversely, there was an overall decline in spirit consumption, with Vodka, Gin and Whisky suffering the most. RI’s Whisky and Vodka categories were notably impacted, especially flavoured Vodka, which saw strong declines in the UK while Absolut underperformed.

Your Weekend Reading

Not so boring CBK - the bank is benefitting from the continuation of the ECB’s 4% policy rate, the interest rate hedge portfolio rolling off and deposit pricing pressure which isn’t as bad as it expected. Higher for longer on interest rates is exactly why Erik@YWR originally turned bullish on the Euro banks (he anticipated they would just give the extra profits back to shareholders, which is what is happening with the dividends / buybacks). He believes the next stage is for the banks to realise the sky isn’t falling and flip from deleveraging mode to growth mode. Erik’s EPS forecasts for 2024 and 2025 are 20%+ ahead of consensus and sees the share price hitting €27 by 2026 (70% upside).

CEN-ESG

ESG disclosure report - SPI's ESG score increases to 42.3/100. Highlights include: 1) Environmental - saw the group reduce its emissions by 3% ahead of its decarbonisation target and SPI also conducted climate scenario analysis for the first time. A £12m investment is planned in FY24 for solar PV installations and to upgrade all hospital Building Management Systems. 2) Social - 98% of inspected locations achieved ‘Good’ or ‘Outstanding’ ratings from inspections. However, Y/Y scoring was impacted by the absence of previously disclosed metrics. 3) Governance - remains above the sector median. SPI has exceeded its 2025 target of >40% female board representation two years early. Click here to access the full report.

the IDEA!

Since the IDEA! issued their previous in-depth report on INPST, the share price has nearly trebled. Against this background, they argued the time had come to make an assessment whether all the drivers they referred to then are reflected in the share price now or that the stock could have more in store for its shareholders. For that purpose, the IDEA! has looked at the latest trends in e-commerce and how these could affect INPST. They have also taken a deep dive into the main markets where the company is active. Their DCF model points towards a fair value per share in the mid-20s. This represents a premium of almost 50% vs. the current share price.

North America

Trivariate Research

The ways to use FCF yield to pick stocks

Trivariate Research's latest report analyses FCF trends of US corporates, both yield and conversion, efficacy of the signal and opportunities that may surface when financial conditions tighten. Key findings include: 1) FCF yield works in SMID cap and middle quality best. 2) From a sector perspective, it is effective in Machinery; volatile in Healthcare. 3) FCF yield matters more when financial conditions are loose. As soon as it begins tightening, de-emphasizing FCF yield and focusing on FCF conversion to pick winners from losers in “junk stocks” is prudent. 4) Quantitatively derived longs include Cigna, Cummins and Centene. Shorts include Elevance Health, Humana and Xylem.

Belkin Report

Stock market rotation is gradually turning defensive

While Utilities outperformance is being attributed to greater energy demands of AI and EVs, many “boring” electric utilities without obvious AI potential are up DD % over the last few months (AES, Dominion Energy, PSEG). Furthermore, Consumer Staples has an early outperform forecast in Michael Belkin's proprietary times series analysis model - another risk-off signal. The AI and Tech obsession obscures a bigger trend: many Tech stocks are declining. The CLOU cloud software ETF is down -15% since early Feb. Former leading new-era disruptors are top Sell recommendations (Uber, Meta, Netflix). Even Nvidia remains a Sell and its biggest risk is something nobody is talking about: its chips are made in Taiwan.

Two Rivers Analytics

HOG features as one of the top short candidates in Two Rivers’ Declining Business Model. Sales have fallen at an accelerating rate since the Jun 23 quarter. Sales per employee are at previous lows of $912k per employee. Margins have given up their post-Covid bounce. SG&A was being cut through Mar 22, then increased on upbeat expectations that did not pan out and is being cut again. Unlevered FCF appears to be recovering but on unsustainable working capital liquidation. EBITDA is declining and the company needs to make its capex. Leverage has risen post-Covid with maturities every year until 2030. At the last earnings release, guidance was weak and the stock fell.

Behind the Numbers

MHK reported non-GAAP EPS of $1.86 in 1Q24 which was 18 cps ahead of the consensus estimate. Revenue was a slight beat. However, as is often the case with this company, there were two one-time accounting-related benefits that BTN believes accounted for almost all the earnings beat - lower allowance for bad debt could have added as much as 12 cps and a decline in warranty accrual relative to sales could have added as much as 5 cps. Both items have been benefitting results for multiple quarters and BTN expects them to shift to becoming earnings headwinds.

Bios Research

Another successful short from the Bios Research team - the stock has fallen nearly 40% since they turned bearish in Feb 24. They originally identified STVN as a short due to excitement around STVN and other biologics suppliers following the tremendous growth seen in the GLP-1 craze. In Bios' opinion the market was mistakenly looking for "picks and shovels" in the GLP space and overvaluing the company. Recent earnings were disappointing and management was also forced to decrease FY24 revenue guidance. Although Bios believes STVN remains overvalued, expectations have now come down to more appropriate levels.

Northcoast Research

BA lowers its FCF target for 2024 to the negative $1-2bn range as Chinese customers are currently unwilling to accept the new 737 MAX aircraft. The latest corporate dilemma, which seemingly adds to the weak balance sheet narrative, relates to an ongoing Chinese regulator review of batteries that power the 25-hour cockpit voice recorder. However, there is growing speculation to suggest BA has, once again, become a casualty of renewed US / China trade tensions. Northcoast updates their model to account for fewer commercial aircraft deliveries in the current quarter, driving a larger earnings loss forecast for 2024. Their TP of $140 still offers 20%+ downside.

Sidoti & Company

A healthy earnings beat in 3Q24 - BRC is benefitting from expanded sales per customer, as it continues to roll out upgraded products and utilise increased digital advertising to reach a wider customer base. Sidoti lifts their FY24 EPS forecast to $4.12 and FY25 to $4.40, as they increase their long-term gross margin assumptions to ~51%. They introduce their FY26 EPS estimate of $4.68 based on 4% revenue growth and further improvement in operating margin. Sidoti models FCF per share growing to $4.19 in FY25 and $4.36 in FY26 (vs. $2.47 in FY24), as capex returns closer to maintenance level and cash conversion approaches 100%. TP increased to $80 (20% upside).

Thompson Research Group

The secular trend of the reindustrialisation of the US / North American market is one that TRG believes has a long tail for growth (10+ years) and will see a greater differentiation of winners. As a vertically integrated heavy materials producer, KNF is well placed to benefit. It was an “orphaned asset” under the MDU umbrella, and now as an independent entity, it has a greater ability to focus on value creation. To that end, KNF has already hit its 15% EBITDA margin target two years early. The next stop is 20%+, which TRG believes will come from a mix of pricing, cost control, and mix shift to materials focused from both organic and acquired efforts. 55% upside.

Abacus Research

FTV is a high-quality business with an asset light model, high margins, high incremental margins and consistent FCF generation that is reinvested in M&A. Recent guidance for slow organic growth for Q2 and FY24 has impacted the stock, which Abacus believes is an opportunity to accumulate. FTV’s key strength of integrating and improving acquisitions along with organic growth in instrumentation and testing should deliver close to management’s targeted earnings growth of 15% per year over the next 4 years. Relative to other compounder business models, FTV looks to be well positioned and offers compelling potential returns.

BWS Financial

Profitable AI - INOD is a misunderstood data engineering company benefitting from working with large tech companies and enterprises in developing LLMs or refining LLMs to fit the need of a specific industry. The company has been around for 30 years evolving with data and Hamed Khorsand believes the current pathway related to AI could have longevity the stock is not valued for. He forecasts revenue growth of 40% in 2024 and over 25% in 2025. TP $24 (85% upside).

Kailash Capital Research

Kailash’s ranking tools are surfacing high-quality, high-growth stocks with long “economic runways” trading like value stocks. ARIS trades at 7.4x EV/2023 adjusted EBITDA, more than four multiple turns below the overall stock market. Bridging half this gap would push the share price above $20. With 84% of its 2023 revenue in its largest business, Water Handling, from long-term contracts, future revenues and cash flows are highly predictable. The company should generate $45-65m in FCF in 2024, with much dedicated to share repurchases. So, you have a rapidly growing company with a tremendous economic moat repurchasing shares and throwing off enough cash to pay double the dividend you receive as an owner of a large-cap index.

Japan

JapaneseIPO.com

This tofu manufacturer has leveraged automation to gain a cost advantage in the Japanese market. However, with the domestic market expected to remain flat, Yamami needs to find new avenues for growth. Its strategy involves expanding into the Greater Tokyo area and capturing market share by offering premium tofu at competitive prices. The stock reached an all-time high of ¥4,170 in Feb 24, but the shares have since fallen nearly 30%, likely due to profit-taking and the absence of fresh catalysts. It is now trading at an attractive 14x 6/25E, compared to the historical operating profit CAGR of 16% over the past four years, with another 15.5% increase anticipated for FY25.

Asymmetric Advisors

Earnings have grown +600% over the last 5 years to ¥3.5bn with OPM increasing from 5.6% to 22.3%. For FY24, I’ll should be able to achieve >¥4.5bn and given the strong business momentum, a further +15-20% OP growth in FY25. Why is the story so good? I'll is increasingly dominant in software for inventory and sales management for manufacturers and wholesalers; and 1) as the labour market gets tighter demand is growing for software to improve operational flow; 2) project sizes are getting bigger; 3) strong demand means it can "cherry-pick" projects; 4) I'll has been raising the % of its business that includes higher margin consulting; 5) it is also expanding in to software for retailers.

Emerging Markets

CHA-AM Advisors

China: Dividends and duds

Now is not the time to be buying developers and other property plays, according to David Scott. 1) Chinese property developers have never generated any meaningful FCF. 2) David heard the same story in Japan / Thailand following their property busts. The boom never returned and never will. 3) The more government involvement in an industry, the worse the returns are for the minority shareholders. 4) In a country of enormous numbers the amounts being talked about are too small. In this week’s edition of David's ‘A Strategist’s Diary’, he also outlines the key characteristics of a GCGB (Great China Growth Business) focusing on 3 stocks: Midea, Kweichow Moutai and Sungrow Power Supply.

Galliano's Financials Research

EM Digital Banks

Victor Galliano turns bullish on KakaoBank, for its increasingly secure competitive positioning in Korea, its attractive digital efficiency ratio, its low customer acquisition cost and for its high activity rate. He switches his Buy rating from Banco Pan to Inter as the latter has improved operationally, it is sound on capital and attractive on valuations. While Nubank is executing well, Victor remains cautious on the stock as he continues to see potential capital constraints as a key risk, along with its stretched valuations.

Smart Insider

Kong Lam (Chairman / President / CEO / Founder) purchased US$3.5m worth of stock from May 24-28th at an average price of HKD 6.87. These are his first purchases since Dec 20, when he spent US$17m at an average price of HKD 8.14. Smart Insider ranked the stock +1 (highest ranking) in Dec 20 based partly on his purchases but at the time Hongbing Chen (COO) was also buying the shares. That signal proved to be very timely as the stock traded above HKD 20 six months later. They are ranking the stock +N and will monitor closely to see if he is joined by the COO or other insiders at the company for a potential further upgrade.

Macro Research

Developed Markets

View from the Peak

Is AI destined to crush volatility and tighten credit spreads?

Artificial Intelligence won't save bad companies or business models, but it will make strong companies more resilient, improve margins and optimise processes. Paul Krake says that this will lead to more stable cash flows and balance sheet stability, a prerequisite for credit investors. AI will improve the credit quality of companies, boost equity valuations and depress the volatility of earnings and share prices. For the balance of the decade, credit spreads should remain suppressed and realised volatility will be low as the SPX grinds towards 10,000. The cycle will be influential, but it is important to note that outside of global crises (GFC and the Pandemic), the US has had one recession since 1990 and hence concerns about default rates are consistently overblown. Credit will be a compelling asset class for the next five years.

Radio Free Mobile

AI: Artificially Inflated

The market is currently valuing revenues from AI at 150x for 2024, which is clearly unsustainable. A significant reset will come soon, with only the big digital ecosystems surviving. Nvidia remains the exception, with a far more reasonable valuation that will result in a much calmer correction when the time comes. Richard Windsor prefers to look more laterally where there is more value to be had. One of these lateral arcs is nuclear power which is going to be needed to power all the data centres and another is inference at the edge (which Microsoft has just championed) where Qualcomm and MediaTek are likely to be the big players.

Blonde Money

UK: Early election, early decimation

Rishi Sunak is not trying to win; he’s trying to avoid going down in history as the man who destroyed the Conservative Party. Polls and forecasts show very poor results for the Tories. Sure, polling is unreliable, and a campaign can shake things up, but Helen Thomas points out that the electorate made up its mind a year ago. Sunak hopes that calling an early election will allow him to fare better, but his actions have upended the Conservative Party machine. He lacks the boots and the resources on the ground, hasn’t consulted his MPs, lacks enough candidates and doesn’t appear to have a plan. Sunak may be aiming to narrow the polls and gain momentum, especially with ideas such as the introduction of national service, but he won’t get the chance. For now, he remains an election liability.

Minack Advisors

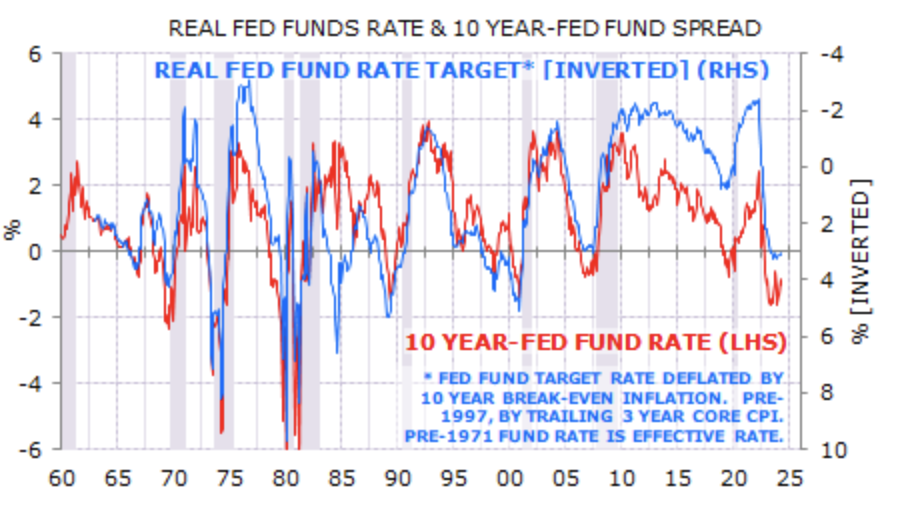

Why is the yield curve inverted if the US is going to soft land?

The soft landing base case has been embraced by all, yet the yield curve is still inverted. Gerard Minack doesn’t see this signaling elevated recession risk. Rather, the market is mispricing the neutral Fed funds rate as it remains too optimistic about how low the policy rate will ultimately fall in a soft landing. What drives the yield curve is the perceived restrictiveness of Fed policy. Prior to the GFC there was a reliable relationship between the shape of the curve and the level of the real Fed fund rate (see chart), but afterwards the curve was roughly 200bps lower than any given fund rate (shown by the divergence between the two lines in the chart). Now, the neutral rate has returned to the pre-GFC level, which means the curve is now around 100bps too low, an error that explains the curve inversion.

East Asia Econ

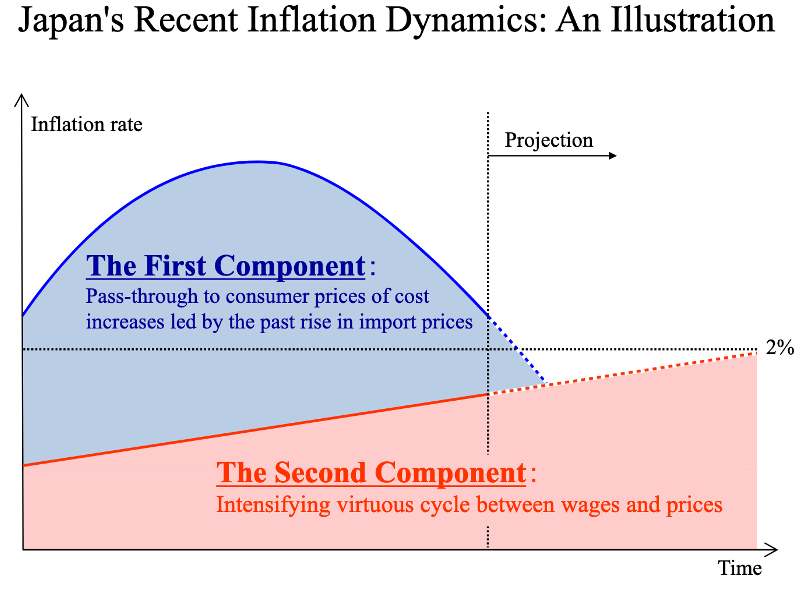

Japan’s inflation dynamics

The BOJ expects core inflation to average 2% in the coming years. For that to happen, Paul Cavey points out that there has to be a transition, away from what the bank calls the "first component – the pass-through to consumer prices of cost increases led by the past rise in import prices" to a "second component – an intensifying virtuous cycle between wages and prices". In monitoring progress in this transition, the bank stresses that "developments in services prices – where labour costs account for a high share of output prices – are particularly important". The upshot is that monthly inflation data aren't going to sway the bank's opinion very much. As long as the labour market remains tight, then the bank's overarching view likely won't shift.

Independent Strategy

QT vs QE: The nature of asymmetry

The reduction in central bank balance sheets is not reducing liquidity in any way that matters to financial markets. David Roche explores the two reasons: The “Fire Brigade syndrome”, which makes QE and QT asymmetrical and is related to human behaviour; and the new central bank operating frameworks, which he examines in his latest report. Central banks will see their economic footprint vary according to which operating system they choose! The Fed’s choice spells greater involvement in sovereign debt markets than say the ECB, which coincides with booming fiscal debts and deficits. A question is the extent to which the “Abundant Reserve” operating system chosen by the Fed will lead to de facto monetisation that might cause the USD to lose some of its reserve currency advantages.

Emerging Markets

Rosenberg Research

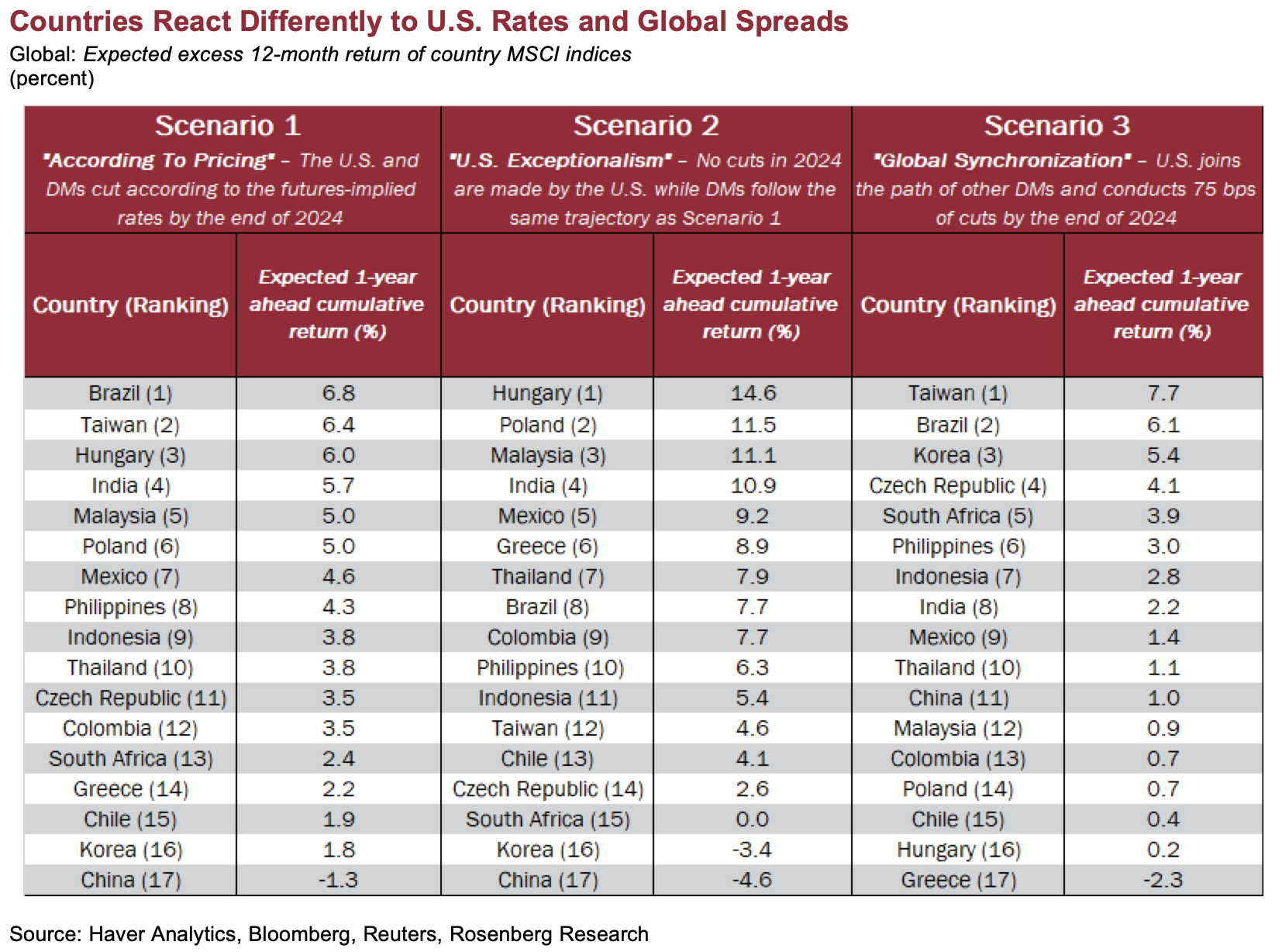

The EM playbook for the coming cutting cycle

EMs aren’t what they used to be. Better-run and more resilient EMs are delivering more stable returns, but they do throw up some challenges for investors who need to adjust to new global financial transmission patterns. Add to that the fact the US will be keeping rate settings tight this cycle, whereas EM-focused investors find themselves in need of a new playbook. David Rosenberg uses an equities return model that addresses both of these issues. He finds that Taiwan, along with Brazil, are well-placed among their peers, while Hungary will greatly benefit from future Euro area cuts. His long-term bullish calls also line up for Mexico and India, which look like strong plays across a range of scenarios for global rates.

Greenmantle

Argentina: Swift action needed

After six months in power, President Milei’s performance is remarkable. Nobody now challenges his legitimacy and the opposition is leaderless. This is no small feat in Argentina. His popularity appears highly resilient, despite the fiscal shock therapy and recession. If Milei gets his Ley Bases and if Caputo manages to bring inflation down close to the official rate of exchange rate depreciation in the coming quarter, the initial programme will have been a success. Yet Niall Ferguson worries that inflation is being kept down by artificial and/or temporary factors such as frozen prices or delayed subsidy removals. After the Ley Bases passes, the government needs to move fast with the IMF and the lifting of capital controls, which are the necessary preconditions for the economic recovery Milei needs for 2025.

Alberdi Partners

Chile: Stronger copper, weaker government

The government of President Boric is trying, once again, to reboot and regain control of the political agenda and reposition its priorities. Yet, as happened before, unforced errors have thrown the attempts into disarray. Fruitless debates over student loan forgiveness and concerns over crime have undermined the government’s eagerness to rescue the pension and tax reforms from legislative gridlock. Marcos Buscaglia believes the CLP still has room to strengthen on the back of higher copper prices and a less dovish central bank, which he expects to reduce the pace of easing to 25bp from 50bp in its next meeting. With higher copper prices, expect the government to start accumulating external assets again, amounting to about 1% of GDP.

PRC Macro

China RMB: Buy the rumour and sell the fact?

President Xi recently hosted a preparatory session for the Third Plenum in July. On the previous two occasions, William Hess points out that Beijing’s pivot to growth support helped the RMB appreciate against the USD. Will this occur again? For this to happen, the PBoC and RMB must overcome two technical obstacles: 1) RMB overvaluation against the currency basket, and 2) the large and persistent deviation between the official fixing rate and the market exchange rate. These issues have only worsened recently. Moreover, the current policy and transmission lags for property stimulus and backloaded fiscal spending will raise questions about the efficacy of growth support measures. William has significantly revised the probability of a one-off devaluation of the PBoC’s USD/CNY daily fixing rate by 1.5% from 20% to 60%.

Copley Fund Research

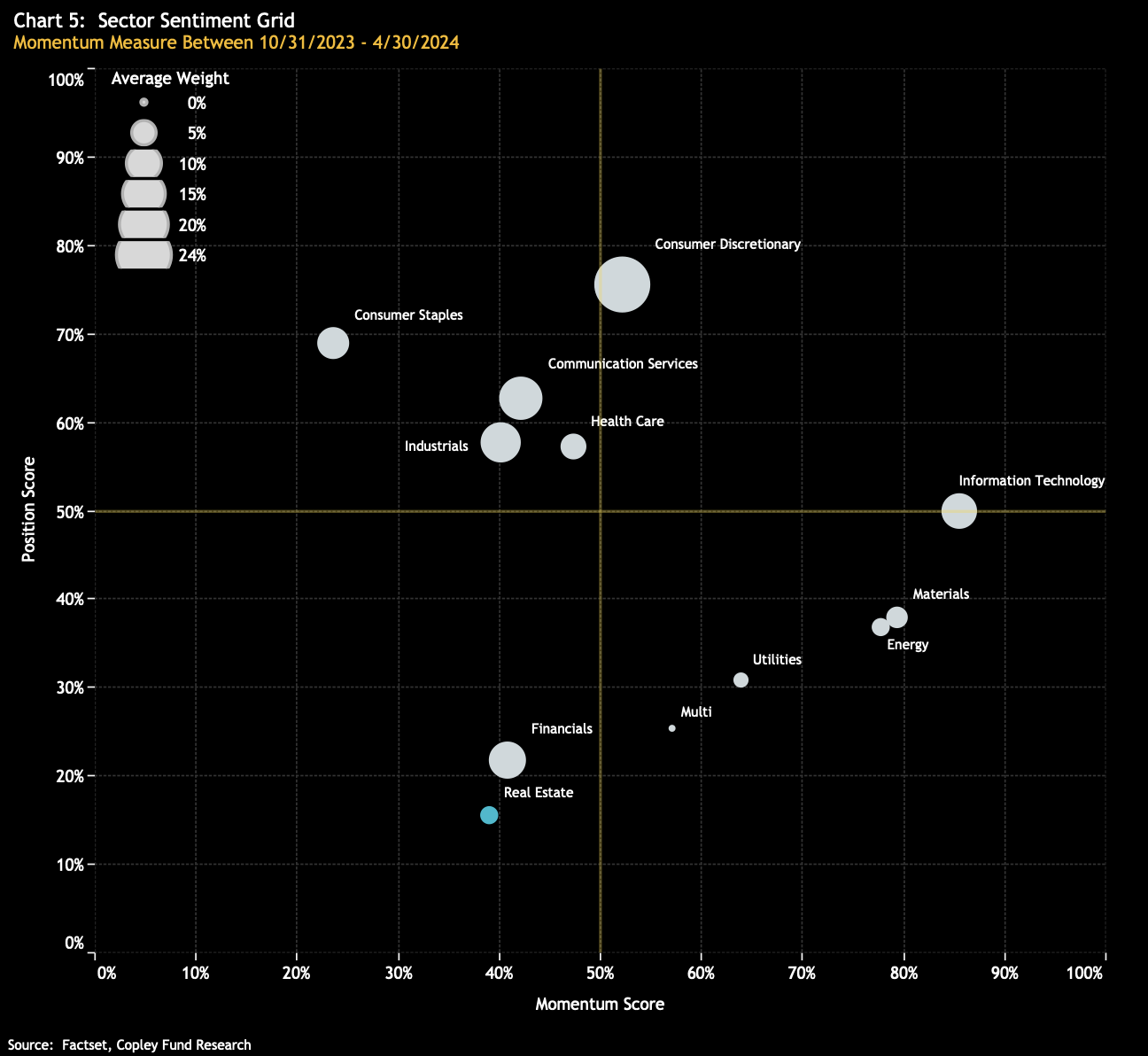

China Real Estate: Continued fund rotation drives new lows

Steven Copley takes a look at positions in China’s real estate sector, and it does not look good. Real estate holdings in active China equity funds have plummeted to a new low of 2.51% (from 8%), with only 76.4% of funds maintaining any position. The number of real estate companies held has plummeted from just under 100 in 2019 to just 42. It represents the largest percentage of funds invested in any sector, with significant closures driven by key investors such as Janus Henderson and Quilter. Amid the downturn, KE Holdings stands out, having attracted a growing ownership base and reaching an all-time high in investment. Nevertheless, investors are reallocating to sectors like Technology, Energy and Materials.

CrossBorder Capital

China: Stronger USD, weaker Yuan

Michael Howell argues that domestic high street and asset prices must fall and/or the nominal Yuan exchange rate needs to devalue. He thinks the latter is more likely because otherwise the PBoC will be forced to run a tight monetary policy to defend the exchange rate, which is at odds with expected economic growth. A weak Yuan suits the US by discouraging investors from shifting funds into Chinese assets. It could also be a globally disinflationary force, but the threat of devaluation in China may also trigger a surge in gold buying – gold looks like a general winner. The vast size of her trade surplus means China will find it hard to avoid using the USD, but the country will more widely diversify dollar investments across safe counterparties, which could encourage the development of an Asian-based ‘Eurodollar’ type market.

Emerging Advisors Group

Mexico: Slowing from… what?

Most of the recent non-election news has focused on slowing growth, but Jonathan Anderson points out that this is an old story – the economy has been flat for over a year. Unfortunately, there’s very little momentum to be found in the data today, neither in domestic nor external indicators. The only hope is for a much more rapid cutting cycle, but Banxico remains the most conservative central bank in the region. In this environment, Jonathan sees no reason to chase equities. Rather, with nominal rates still in the double digits, peso carry and fixed income remain his trades of choice.

ESG

Verisk Maplecroft

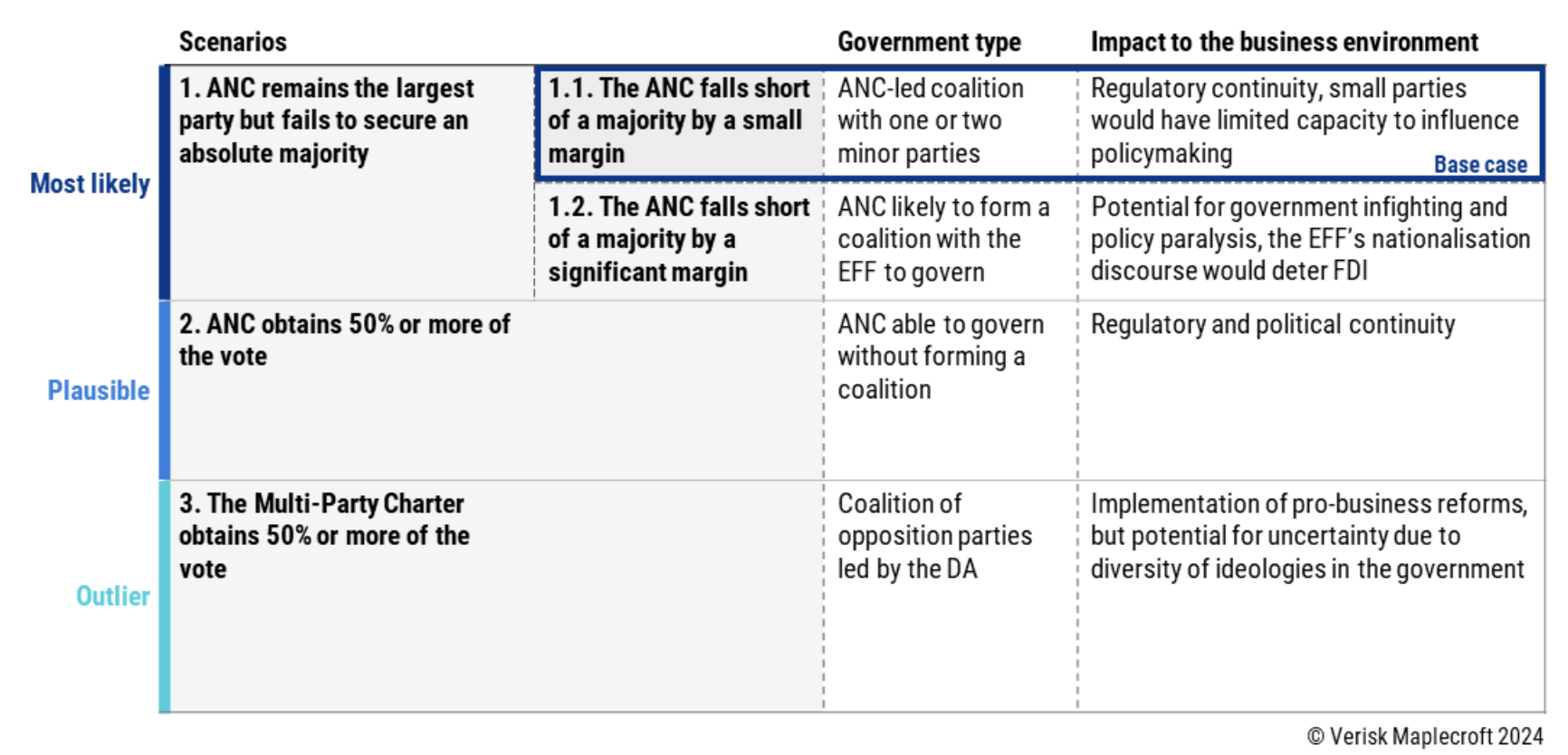

South Africa: Election risks

South Africa is the worst performer in sub-Saharan Africa on Maplecroft’s Civil Unrest (forecast) Index and the second highest-risk country globally on their Predictive SRCC Model, built for the insurance market. The recent election risks triggering protests, although they are unlikely to reach the levels of disruption experienced in 2021 after Zuma’s imprisonment. On the sovereign outlook front, investors will watch and wait on the sidelines. S&P affirmed the BB-junk rating, and FDI levels remain ignominiously weak. SA bonds have seen tailwinds in 2024 as investors hunt for yield, and assets will rally again in the coming weeks if the base case scenario plays out (see table), with higher mining and other commodity export prices also supportive of rebounding market sentiment. However, without a clear commitment to fiscal consolidation after the polls, any rally will be short-lived.

Sustainable Market Strategies

Healthcare and AI: A complete check-up

The Sustainable Market Strategies team’s latest report examines the impact of AI in healthcare, which is growing at a rapid pace but is bringing about significant cause for concern. One major issue is bias, with AI risking exacerbating existing health disparities when trained on data that lack diversity. There are also worries around safety, privacy and security, loss of personal interaction and job displacement. As it stands, regulation of AI in healthcare is very limited, but this will grow over time. The companies that will be best positioned for the future will be those that proactively engage with regulators to shape effective and fair AI policies. Although concerns are valid, the healthcare sector stands to benefit the most positively from AI. Potential winners include Sysmex, Fresenius, Hologic and Intuitive Surgical.

Commodities

Vanda Insights

Crude may stay rangebound this summer

More than three weeks of rangebound movements in benchmark crude prices, which have seen Brent broadly locked in a $82-84/barrel range, has stirred up some unease in the market as to whether there might be factors gathering in the background that could prompt a bull run or a bear slump. With the geopolitical risk premium firmly out of the way for the time being – both on account of the Gaza war and the Ukraine war – Vandana Hari thinks the conditions remain conducive for the current equilibrium to hold for a bit longer. Economic outlook is in the driver’s seat for the oil complex and there is plenty of uncertainty and skittishness in the broader financial markets. However, the mood shifts are a few degrees removed from implications for oil demand, so they do not produce big price swings in crude.

Meridian Macro Research

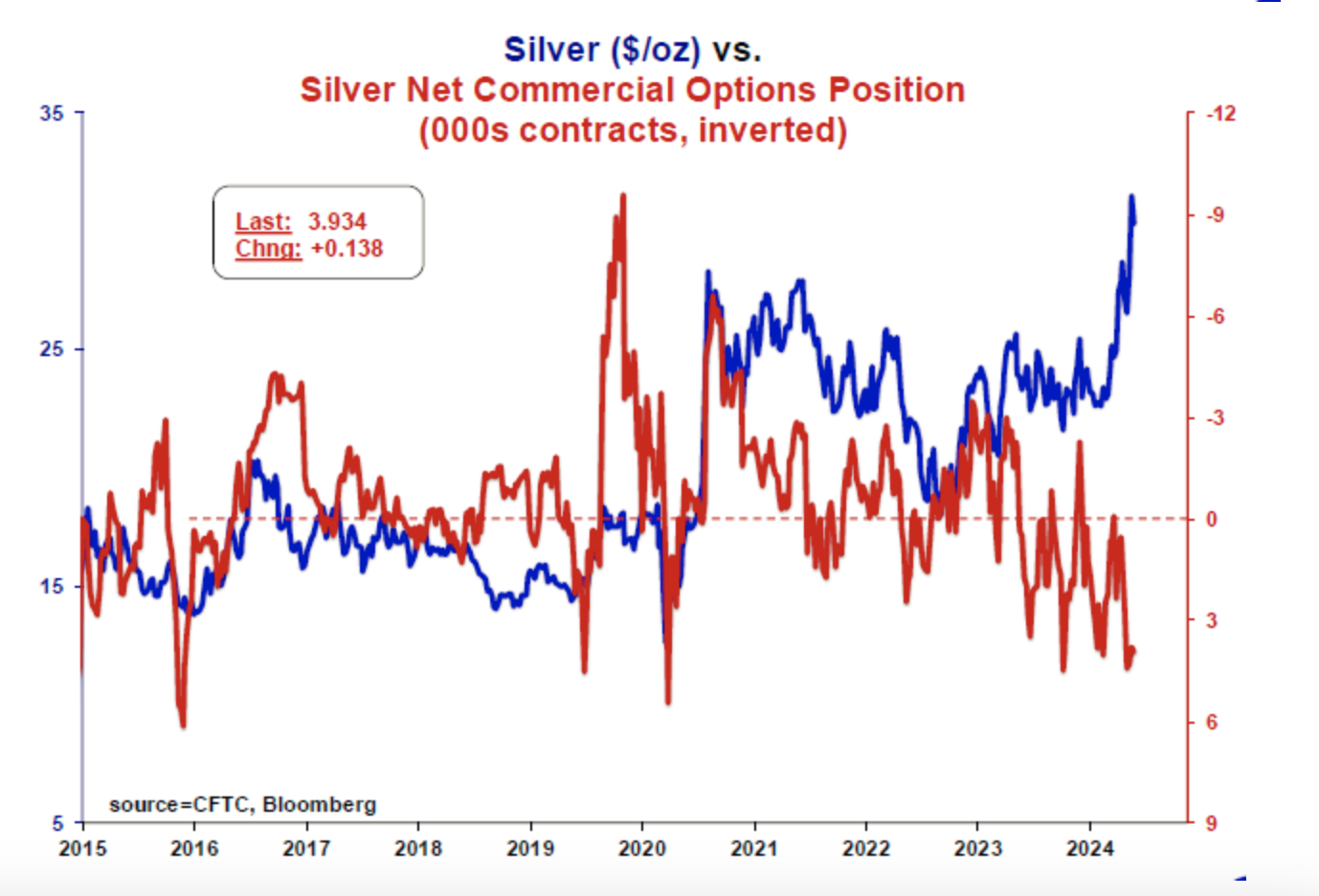

Gold & Silver: Breakout delayed

Gold and silver both suffered a pullback this week, similar to what happened a month ago. As with the late-April retreat, Eric Pomboy sees this as a rather small decline with a swift rebound to be expected. Of course, there may be a more concerted effort by the bears to hold the line at these levels, thus delaying a convincing breakout, but Eric says that the breakout is sure to come relatively soon regardless. Interestingly (and this may change with next COT update), Silver Net Commercial Options position remains in elevated/bullish territory just waiting for a breakout. In short: the spring is still coiled for the PMs and a break through resistance is expected to occur soon.

Global Mining Research

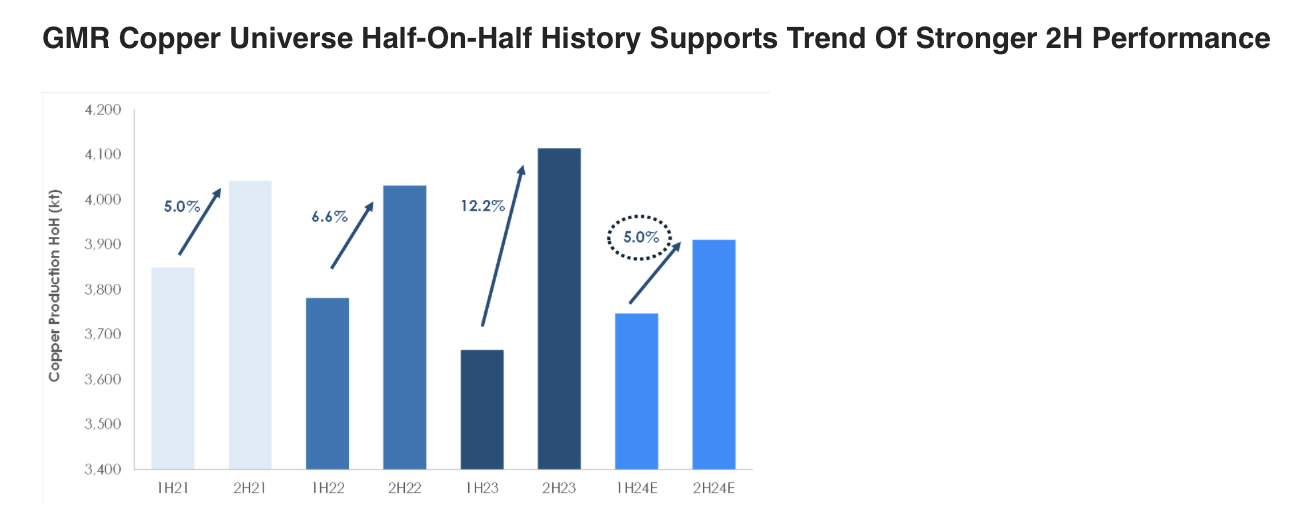

Copper: Risk to the downside

Copper prices had a strong start to the year. David Radclyffe’s review of the Q1/2024 performance versus 2024 guidance for the December year-end stocks helps put the market tightness into perspective. The key takeaway is that, as with gold companies, copper miners are banking on a strong H2/2024 to meet annual guidance figures. The risk is therefore to the downside, with once again copper producers struggling to either meet guidance or increase production appreciably. Only Hudbay Minerals, KGHM, Southern Copper, Freeport-McMoRan and First Quantum Minerals are tracking to 2024 production expectations. David’s preferred copper miners are in the small/mid-cap space on valuation grounds, including Atalaya Mining, Capstone Copper, Sandfire and Hudbay Minerals.