Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Geography

Europe

Iron Blue increased WPP's score to 27/60 (newly top quartile). This is a reflection of: 1. Bad debtor impairment provisioning ending FY23 at a decade low; 2. A new contingent liability disclosure relating to India tax audits; and 3. Whistleblower cases jumping +65% yoy. These factors more than offset the reduction in accrued income on WPP’s balance sheet. Stripped out one-off costs (mainly restructuring and asset impairments) remained elevated at 30% of PBT adj. Iron Blue is watchful about the potential for changes in accounting approach with the FY24 replacement of Deloitte as auditor following their >2 decade tenure. Of particular interest is £3.2bn accrued income on WPP’s balance sheet.

Vision sees risks for Allegro.eu (ALE.WA) shares due to rising competition. Despite slightly better-than-expected GMV and take rate growth, management's comments confirmed intensified competition, particularly from Temu, which is rapidly expanding in Poland. Allegro increased marketing spend to counter this, impacting future margins. 1Q24 revenue increased 6.6% YoY and adjusted EBITDA beat expectations at PLN 706mn, but net income missed at PLN 242mn. Vision believes increased competition from Temu, Amazon, and AliExpress, alongside rising delivery expenses, will pressure Allegro's profitability.

“New Cellnex” was defined at its Q3 2022 results, with a sharp focus on visible organic revenue growth, efficiency gains from rising tenancy and lease reductions, reducing capex and higher minimum dividends from 2025E. The dividend yield rises to 2.7% in 2027E and 16.9% in 2031E. Cellnex TP rises from €74 to €76 and is rated no.2 of their 24 Global Infrastructure stocks, having had the greatest change in corporate strategy in recent years. Cellnex projects an annual revenue growth of 5.4% for 2023-30E and 3.2% for 2030-40E from secure sources. With €4.1bn BTS capex winding down post-2027, returns and efficiency will be boosted. Strategic disposals will create value by narrowing valuation gaps. FCF is expected to rise, reducing debt and increasing dividends, with significant share buybacks planned.

Rheinmetall AG (RHM.DE) wins $325 million artillery ammunition order

Rheinmetall reported first quarter 2024 consolidated sales of €1.581 billion compared to the same period in 2023 of €1.363 billion, much of this has been driven by demand for artillery ammunition. Rheinmetall won a €300 million contract for artillery shells and propellant modules for a NATO country, with deliveries from 2024-2028. The company, vital in supplying Ukraine against Russian forces, has expanded its manufacturing capabilities, bolstered by the acquisition of Expal Systems and significant contracts with the German Armed Forces.

Telecom Italia Q1 24: First positive service revenue growth in 7 years - for shareholders willing to look across the divide to the post-NetCo world, New Street see an attractive story emerging, with a number of potential catalysts to help further deleveraging. Q1 saw 11% YoY EBITDA growth, with TI guiding 2-3% revenue and 9-10% EBITDA growth for 2024. Improvements are driven by higher ARPU in wireline and better wholesale mobile revenues, despite challenges in the broadband market where Open Fiber is gaining subscribers. Mobile service revenue growth turned positive for the first time since 2018, though subscriber losses persist. The NetCo sale to KKR is likely, shifting focus to ServCo’s growth. Several catalysts, including potential asset sales and debt reductions, could enhance ServCo's appeal and improve Telecom Italia's valuation.

North America

Summit believe the expanding SAM in the AI custom-ASIC and networking markets can drive further financial outperformance in 2H24. Their industry checks also indicate that the cyclical downturn in the carrier and enterprise end markets is now behind us. Summit believes the enterprise and broadband end markets will recover in 2025, driven by the upcoming new product cycle. They also see AVGO benefitting from a new product cycle for AI-related networking ICs and custom ASIC accelerators in 2025. AVGO remains well-positioned to outperform its peer group through 1H25.

The company lowered its guidance for FY 2024. They reported a slip in bookings and increasing marketing costs, with several major titles underperforming. They also delayed another game release. In addition, there is a general industry slowdown in gaming and weakness in the mobile gaming market. Sales growth was -6.7% last quarter, a third quarter of declines and Sales per employee have been flat to declining since 2015. Gross margins have increased 252bps over the past four quarters, and EBITDA margins have increased 330bps over the past four quarters on an annual basis.

Sales Pulse continue to pick up more positive views of the tailwinds for Nutanix and examples of deals that are driven by Broadcom’s acquisition of VMware however, channels are quick to state that the move from VMware is challenging, at least for large users. In Nutanix upcoming report we expect to see more evidence of growth from the Broadcom/VMware acquisition as well as the other catalyst that we have discussed in recent notes (increase in partnerships including Cisco, Dell and additional VARs), but rapid acceleration seems unlikely. Many speakers at Nutanix’ Next Conference in Barcelona discussed their move from VMware to Nutanix.

Alembic are reiterating their Overweight rating on shares of ESLT and are raising their target price by USD4 to US265. ESLT shares have been weak YTD, particularly recently, due, Alembic believe, to political factors. One manifestation of such factors is France’s recent decision to bar Israeli firms from the upcoming Eurosatory defense conference. Despite such issues, they do not believe the fundamentals support a weakening in ESLT shares and believe there is meaningful upside from here. As such, Alembic reiterate their Overweight rating. Their 15.5x terminal valuation is ~5% premium to the S&P 500 on FY1 EV/EBITDA and Alembic believe there is likely room for valuation upside should ESLT’s focus on margin rate and cash flow begin to bear fruit.

R5 made several adjustments that push their equal-weighted valuation estimate of Walmart’s equity to ~$100. First, R5 extended out to look at FY27 (CY26). They then added about $0.30 to their current forecast of $3.20 in EPS in FY27 and added ~$2 billion to EBITDA. For a frame of reference, the Street’s current average estimate for FY27 is approximately $2.90. Turning to R5’s DCF, they grow EBIT 8% until TV, when they lower growth to 3.3%. Currently R5’s average EBIT growth rate is 6.5%, and TV is 3.0%. These are undoubtedly very bullish assumptions, but possible, in R5’s view, if they are right about the building advantages of the company’s business model.

DOL-TSE shares have gained 33% YTD and now trade nearly 19x EV/ FY24E (Jan-2025) EBITDA. The stock gains have been in reaction to very strong traffic-driven comparable-store sales growth. This has combined with generous flow-through to the bottom-line. FY23 (Jan-2024) same-store sales jumped 12.8% on top of a 12.1% increase in the prior year. EPS in FY23 grew 29% on top of 26% the prior year. Quo Vadis attribute DOL-TSE's strong performance to the impact of inflation on the Canadian consumer, which has prompted value-seeking behaviour. DOL-TSE has been well positioned to benefit from this based on its assortment, primarily direct-imports, which is offered at a discount to similar items at other retailers.

Respondents that directly procure from Cognizant have noted spending levels marginally ahead of estimates. It appears that the re-acceleration in IT spending levels has been slower than initially expected. There has been a noticeable decline in spending on onshore advisory services, which was partially offset by growth in offshore services, particularly in the managed service space, which has largely played into Cognizant’s hands, which have been extremely reactive in pivoting to offshore delivery. Cognizant has bolstered its presence in AI and Cybersecurity.

Bombardier’s bonds have risen sharply after two ratings upgrades in the past month. While there is still progress to be made in improving margins further and demonstrating consistent free cash flow generation, Veritas is increasingly confident in management's 2025 target achievement. Dan Fong of Veritas forecasts a TP of C$112 (24% upside). Dan estimates that its stock could be worth C$210 to C$260 over the next four to five years, representing a ~150% to ~200% gain from the current price.

Footfall trends starting around May 20th will be paramount in evaluating the company's recovery in the coming months. Recall that headline issues began to mount for the company around this time last year and persisted throughout most of the Summer months leading to Target's negative 5.3% comp in 2Q23. Recall on monthly phasing… May, June, and July SSS declined approximately 3.0%, 7.0%, and 5.0%, respectively. YOY traffic continues to recover nicely with the 7-day moving average up 15.0% YOY.

Hawkshaw Research

Hawkshaw published a bullish report on Five Below (FIVE) in advance of their 1Q conference call. While they correctly anticipated a miss and guide down, the magnitude was worse than expected, and the stock is down an additional ~15% (and 45% from the start of the year). Comps this year are now expected to be down 3-5%, as the lower income consumer is pulling back on discretionary spending. Full year expectations have been meaningfully de-risked and the stock is trading near its all-time low PE (22x). On Hawkshaw’s revised numbers, which assume margins recover as the macro pressure alleviates, they see 50-100%+ upside over 12-18 months.

Japan

Nippon Seiki, one of Japan's cheapest value names, now at 0.38x PBR, net cash 65% of MCap, 3.6% yield, beat its 3/24 CoE of OP (Act +211% to Y8.5bn vs OE Y7.5bn) and forecast OP up another +10% in 3/25 (<13x PER). They also announced a 1.85% buyback, following on from their 2.9% buyback announced in November. While it is low margin auto-parts company with a chequered earnings history overly reliant on motorbike speedometers. The next phase of growth will be driven by heads up displays where they are global number 1.

Rakuten Bank is positioned to benefit from rising interest rates in Japan, with its low LDR, high cash balances, growing loan book and healthy capital ratio. The proposed FinTech reorganisation of the group around the bank should drive further potential shareholder benefits; higher ROE, lower customer acquisition costs, increased active account penetration and lower operating costs. Victor Galliano believe that there will be effective governance checks and balances in place to ensure fair valuations of the FinTech segments pre-reorganisation.

Soracom generates nearly 70% of its sales from recurring revenue which is expected to grow through an expanding customer base and increased mobile connections as existing customers develop their IoT businesses. The business is scalable across various industries, with use cases including smart meters for Nippon Gas, remote management for Mitsubishi Electric Europe’s HVAC products, LUUP rental scooters, SumUp payment terminals, and Sollatek refrigeration systems. Global scalability, especially in the US and Europe, is anticipated with minimal additional investment. Overseas revenue made up 36.4% of FY 3/24 sales and is growing quickly. The stock is undervalued relative to its long-term potential and minimal coverage suggests the stock price will rise as investors become more familiar with the potential of the company.

Emerging Markets

Propitious Research

Whilst the Chinese online games market has struggled since 2023, NetEase (9999-HK) has continued to gain revenue market share driven by the success of its mobile titles. Medium-term revenue growth will depend on the continued success of NetEase’s legacy titles and its robust pipeline of upcoming releases, including several highly anticipated launches. NetEase trades nearly 2 standard deviations below its 5-year historic average PE trading range, a level that has proved to be a very good entry point. A steady quarterly dividend policy, ongoing share repurchases, a strong balance, and cash flow generation should further support its share price.

The local services market in China enjoys a large TAM, a fragmented merchant base with few chains, and low online penetration rates. These all support Meituan’s bargaining power, allowing it to triple sales from ’19-’23 to RMB277bn ($38bn). Arete estimate Meituan will retain its #1 market share in its three key markets - food delivery/insta-shopping/in-store services. As competitive pressure in its four business lines eases and subsidies cut, Meituan can deliver revenue and profit growth. Arete initiate coverage of Meituan with a Buy rating and a ‘24E target price of HK$153 (39% implied upside).

ResearchGreece are positive assuming Fourlis will sell an additional 13.3% stake and deconsolidate Trade Estates, using the proceeds to reduce net debt and grow retail sales - mostly IKEA with new stores - at E715m with EBIT at E50m by 2027, both lower than guidance of E750m and E60m in 2026. Seasonally weak Q1 results were promising with sales rising +3.8% yoy and EBITDA turning positive at E0.8m from -E0.3m. RG estimate the retail business is currently valued at 3.8x EBITDAL 2025, +50% implied upside.

Macro Research

Developed Markets

Euro: Small rate cut, big implications

Wolfgang Münchau sees the ECB's recent rate cut as a bad decision. Apart from the ECB's delusional forecast, he sees no evidence whatsoever that inflation is headed toward 2%. What Wolfgang continues to see is significant co-movement in transatlantic inflation rates, despite different economic conditions, which suggests that other factors are at play as well. The markets will no doubt be cheering the rate cut and complaining that more is needed. What policymakers often fail to see is just how deeply unpopular inflation is. We are no longer living in an age where inflation is bad for middle-class savers but good for workers. A 3% inflation as the new normal will have profound effects on the way our economies and political systems are working, and it is the point where people could rationally claim that they would be better off outside the eurozone.

Canada: What the cut means for the consumer

Following the cut in the interest rate from 5.0% to 4.75%, the Bank of Canada is now into an easing cycle. Ben Rabidoux turns attention to what we might reasonably expect in the coming months for housing and the Canadian consumer. He forecasts a modest increase in consumer confidence from an abysmally low level; an upward drift in home sales through the summer, but affordability is still a massive constraint on demand; and a strong supply response, which may seem counter-intuitive, but many of Ben’s trusted contacts say that there are a growing number of owners and investors who have been waiting for a better opportunity to sell. Even with interest rates now coming down, debt service ratios will remain elevated through 2026, and arrears are only starting to rise.

US: The soft landing is already here

Brian McCarthy points out that the flow of incoming data continues to suggest that the Fed has already soft-landed the economy. Growth in the nominal economy is consistent with inflation at 0.5% above target - that’s little more than an annoyance from the Fed’s perspective and absolute nirvana for corporate equities that apply a bit of fixed-rate leverage to generate earnings. So, this is the soft landing. We’re living it. It doesn’t get any better for stocks, hence why they’re going up every day. It is now abundantly clear that there will be no pre-emptive easing; the Fed will do what it has always done and hold rates until it sees the whites of the eyes of recession. Once the economy begins decelerating from here there is no reason to expect it to stop, and Brian believes it to be underway.

US: Something fishy is going on

Michael Belkin suspects that something is amiss with US employment reports, with a difference of up to 2.3 million extra jobs in the payroll vs civilian report, almost as if 3 million phantom jobs have emerged. So what? Politicians on either side pull the levers of power as they see fit, and stock market investors are oblivious, but sector rotation is definitely taking notice. Cyclical sectors and groups have turned down in relative terms with a vengeance. Investors are trained to believe the prospect of Fed rate cuts is unambiguously bullish, but Michael’s model forecast is diametrically opposed to the consensus view, with recession soon arriving and slashing corporate earnings. He is LONG US Treasury bonds (30yr, 10yr, 5yr, and 2yr). The consensus view may see a T-Bond rally as bullish for stocks, but Michael disagrees, with big potential gains from selling and shorting stocks and buying T-Bonds.

US: The contradictions of the Fed

The FOMC held rates in a widely expected decision that was mired in contradictions. The median core PCE projection moved from 2.6% to 2.8%, and the FOMC delayed one cut from this year until 2025. Given the numbers, the Aurora Macro Strategies team push back against the hawkish narrative for the rest of 2024. Powell explained the discrepancy was because the FOMC is being conservative and expecting inflation to undershoot in H2/2024, yet m.o.m core CPI still came lower than any point since 2021, so the Aurora team expect rate cuts to start in September. The team point out that politicians appear to favour inflationary measures, making the prospect of 100bps of cuts in 2025 and 2026 appear overly confident on the dovish side. As the election nears and more of these risks are priced in, risks are skewed to the downside.

The warning sign in US labour

The latest Non-Farm Payroll report showed the US keeps adding jobs at a sustained pace, but Alfonso Peccatiello says this feels weird. It’s hard to square how the US job market can remain so resilient even as rates remain high for long. One of the most reliable long-term indicators of job market weakness is the Sahm Rule: when the 3-month moving average of the unemployment rate exceeds its 12-month low by 0.5%, the recession is here. The latest reading says 0.37%, often cited by bears as a warning sign. If the underlying labour market weakness gets more evident, the Fed needs to react fast. From a long-term asset allocation perspective, one can still remain invested in risk assets here but must be vigilant of surfacing labour market weakness and the Fed reaction function. If they play ball, buying bonds when 10-year Treasuries approach 4.6-4.7% offers great risk/reward.

Japan: Uncertainty among the markets

Manoj Pradhan’s decision to go long 30y JGBs was based on the fundamental near-term weakness in Japan that stands in stark contrast to the BoJ’s decision to allow bond yields to rise. The best rationale one can provide for the drift higher in 10y and 30y yields is a ‘market intervention’ to stem the weakness of the Yen. As long as JPY remains in the 155-160 range, the BoJ will likely see its job done for now. However, allowing yields to rise so much in sharp contrast with fundamentals must create uncertainty about the cost of capital. A 25bps rate hike is one thing, but 30y yields have gone up from 1.25% a year ago to a peak of 2.25 recently. Thankfully yields are falling but markets cannot like the volatility, particularly given where growth and inflation are going. Manoj is staying LONG JGBs.

Decoding YTD performance

Many investors Adam Parker speaks with are generating alpha, beating the S&P500 if they are long-only or even if they are long-short. Did investors manage to crack the code on outperformance and alpha generation? Probably not; more likely, size, style, substance, and momentum have mattered a lot. Adam studied the performance from Jan-May 2024 to examine the magnitude of these factors on performance. Style has not mattered much; mega-/large-cap growth stocks were up 6.7%, and mega-/large-cap value stocks 8.7%. Mid-/ small-cap. growth stocks were up 0.7%, and mid-/ small-cap. value stocks were up 2.1%. However, on a cap weighted basis, the performance has been quite different by style among the mega-/large-cap cohort. Mega-/large-cap growth stocks are up 14.7% vs. mega-/large-cap value stocks up 7.3%. Combining size and style has mattered as owning mega-/large-cap growth has generated strong relative performance.

Emerging Markets

Argentina is failing

It’s now been six months and the Milei administration is still touting its “success” in beating inflation and downsizing the administrative state, arguing the worst is over on the macro front. Jonathan Anderson claims the reality is simply one of failure. Headline annual inflation is 300%, with the monthly rate only having fallen due to an artificial re-pegging of the peso while the black market continues to blow out. The central bank can’t stop printing money; money and credit growth are spiralling out of control even as the authorities slash interest rates. The peso regime will collapse again, and more inflation is on the way. This way lies Venezuela, and Jonathan is selling.

Copley Fund Research

China’s all-time lows

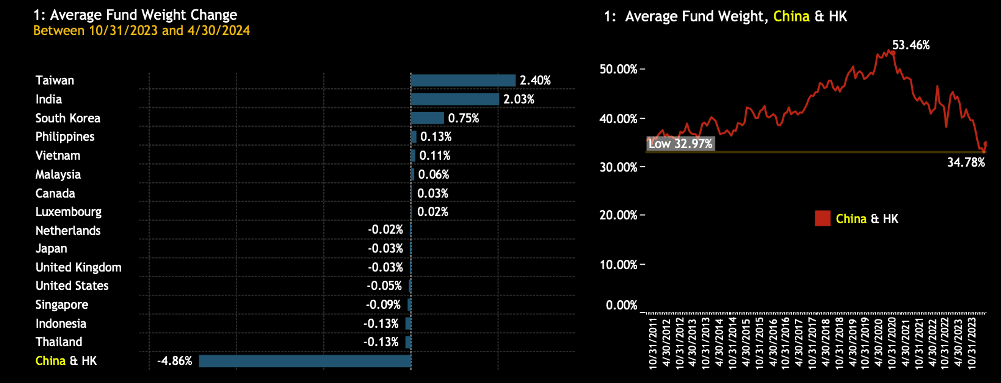

Steven Holden’s top-down analysis into equity fund positioning and performance in Asia reveals that China & HK weights fell among funds by -4.86% from the end of 2023 to the end of April 2024 (chart 1. The total weights have fallen from a high of 53.5% in 2020 to 34.8% today, just above the 13-year low of 33% (chart 2). Steven comments that the country’s positioning is at a critical juncture, reflecting broader concerns and cautious overall sentiment. But at times of extreme positioning is when managers may be more motivated to assess exposure, and as Steven shows in his extensive EM and Global analysis, China's low positioning is as extreme as it gets.

Israel and Palestine: On two fronts

Israel’s strategic dilemma has worsened over the last two weeks. Ceasefire and hostage negotiations have stalled. The fundamental dilemma remains: Hamas believes international pressure will force Israel into de facto capitulation in Gaza, while anything short of Hamas’s political and military destruction would be a defeat for Israel. Combat in Rafah will continue for at least four more weeks. Simultaneously, Hezbollah has significantly ramped up its operations against Israel. Several major incidents this week seem like milestones on the road to war, which Niall Ferguson continues to believe will happen before September. A two-front war is not Israel’s preference, but an emboldened Hezbollah may leave it with no choice—and the growing likelihood of a Third Lebanon War further reduces Hamas’s appetite to reach a hostage deal. Expect the impasse to drag out through June.

Mexico: Overly optimistic

Even before the election was underway, expectations were too lofty, claims Konstantin Fominykh. The economy is slowing down, the rate of investment in fixed assets is dropping fast and manufacturing is ailing. Everything appears to be on the down other than the budget deficit, which continues to reach even higher. Yet, despite misperceptions, corruption is improving. The carry trade in peso is also one of the best in the world and is likely to continue. International funds are still flowing into the country from other EMs, with a record $36bn in FDI in 2023. Konstantin initiates a fresh BUY on 30YMexico on June 6th.

Nigeria: Inflation battle could be impeded by minimum wage plans

Inflation remains a key source of political risk, with prices accelerating to a new 28-year high in April, hitting 33.69% y.o.y. However, the Central Bank’s ongoing battle to tackle the upward pressures could suffer a blow from plans to increase the national minimum wage. The decision stems from the country’s two largest unions leading disruptive strikes, with the potential for a 100% increase in the minimum wage from 20USD to 40USD per month. Although this is a far from the union’s 327YSD a month request, it is likely to be significantly above what is fiscally sustainable for both federal and state governments. If an increase goes ahead, enforcement may be uneven, leading to further strike actions in the coming months.

Russia: Good growth, but headwinds still present

Contrary to expectations, the Russian economy continues to demonstrate robust expansion, primarily driven by investments, manufacturing output, and consumer spending. But it is important to note that public funding has been crucial. The optimistic picture of the economy is dimmed by stagnation in other important sectors. The tight situation in the labour market has triggered inflationary pressures, complicating the CBR’s task of restoring price stability and prompting a warning of possible monetary tightening in July. In the post-election reality, the government appears to be returning to the pursuit of more prudent fiscal and monetary policies, which should cool down growth rates. However, the latest data suggests that inflation is showing no sign of moderation. Christopher Weafer has upgraded his GDP growth estimate from 2% to 2.8% y.o.y., whilst raising his YE24 CPI estimate from 5% to 5.7% y.o.y.

South Africa: The shocking decline of the ANC

It was widely expected that the ANC would lose its majority nationally and in KZN and Gauteng in the May elections. What was a shock was the extent of the party’s decline. In this note, Peter Montalto reflects on the results by delving into some key insights that the elections data provide. In particular, he is interested in the potential implications of these results for the 2026 local government elections and the 2029 national and provincial elections. If the MK party is able to maintain the momentum it has built until the 2026 elections, Peter expects it to win an outright majority in the eThekwini metro. In metros generally, he observes a decline of both the ANC and the DA and several other parties, including ActionSA. This points towards a fragmentation of the system and could mean that the country may not have a dominant party in the foreseeable future.

Commodities

The oil market is overly pessimistic

Andreas Steno remarks that the crude oil market panics whenever OPEC’s supply decisions are questioned, prompting traders to hit the sell button, even during periods of high economic activity. Weakness in soft data has also contributed to crude prices plummeting, yet the bearish sentiment has little data to back it up. The curve got more into backwardation last week after briefly hitting contango, thus the environment for crude to rise again is there if shorts start pulling their positions and markets buy the elevated inflation story both short and long term. Andreas argues for a tempting contrarian call to continue being LONG energy/oil versus metals in July, maintaining SHORT positions in copper and silver.

Digging for gold

A spate of new gold projects is about to be delivered after a period of subdued development, with nine new projects in David Radclyffe’s coverage ready to contribute to production over the next 18 months. With the potential to add over 2.5Moz AuEq per year by 2026, the projects will see a meaningful increase in production for the companies concerned. All projects are forecast with a by-product AISC below US$1,000/oz, offering healthy margins ahead. Overall, Côté is the most impressive of the new projects in terms of valuation, impact on the owner (IAMGOLD), and jurisdiction, despite the rocky road on the way. David favours companies with proven reliability to deliver together with lower risk, such as Agnico and Northern Star, and those with slightly higher risk, including B2Gold, Centerra, IAMGOLD and Perseus.

Gold Focus 2024

Metals Focus has recently published its latest flagship annual report on the gold market, featuring comprehensive historical supply and demand data for the previous decade and a 2024 forecast. Some of the key takeaways include gold’s total supply rising by 3% this year, as gains in mine production and recycling take the total to just over 5,000t. Demand will fall by 2%, with most demand segments posting modest losses. However, prices will achieve all-time highs in H2/2024, as the economic and political backdrop remains supportive, rising by 16% to a record high of $2,250 in 2024. Please contact us to find out more.