Company & Sector Research

Europe

ALEZOR Research

Alejandro Acosta believes the market is too focused on TE’s near-term prospects and underestimates the company’s longer-term potential. However, this sentiment will shift, and when it does, the share price will rerate accordingly. TE’s services include engineering for carbon capture, offshore wind, e-fuels, low-carbon hydrogen, petrochemicals and LNG, make it well positioned to benefit from the energy transition. While TE has been affected by the loss of its Russian business, it has compensated for this with new contracts, such as LNG projects in Qatar and the UAE. Alejandro targets over 40% upside for the stock.

Insight Investment Research

GMR's restructuring should be a catalyst for ADP with listing to clarify its market value. Robert Crimes sees 4 benefits: 1) Simplify the shareholder structure as “New GIL” will include all GMR’s pure airport assets. 2) Deleverage GIL’s balance sheet. 3) Provide more visibly of the listed value and liquidity for ADP’s stake in New GIL. 4) Serve as a platform for GMR Airports to capture new growth opportunities in India and globally. ADP shares are down >10% over the last year and are still significantly below their pre-Covid level. Robert believes ADP’s shares are over-discounting concerns over future Paris regulation, slow Chinese pax recovery, higher real bond yields and French elections. ADP is his top airport pick. TP €227 (95% upside).

the IDEA!

Announces launch of €350m bond offering - although BESI argues it will use the proceeds for general purposes, the IDEA! argues differently. The proceeds will be used, firstly, to continue its share back programme and, secondly, maintain its pay-out ratio in the range of 40% to 100%. In the past 8 years, BESI has issued 4 convertible bonds. In total the company raised €625m. Of this amount none was spent on acquisitions. It used the money to repurchase shares, i.e. to avoid dilution caused by the issue of the convertible bonds. BESI has such a strong FCF it does not need to issue convertible bonds to finance its operations or to make acquisitions.

Woozle Research

Woozle downgrades the stock to Sell following their latest channel checks - respondents reported that NEM’s sales growth in Q2 was marginally behind estimates. In some instances, deal cycles have become more complex and prolonged due to the ongoing transition from perpetual licenses to a SaaS model. ArchiCAD, NEM’s flagship BIM offering, remained a healthy performer this quarter. Respondents generally provided cautious outlooks for the next 3-6 months, with expectations of slightly stronger performance in previously weak regions like Europe, as deal pipelines picked up slightly during the latter end of the quarter, particularly for products under its Design segment. However, a lot of this optimism is largely contingent on respondents expecting interest rate cuts.

North America

Your Weekend Reading

Anatomy of a Private Equity train smash

Erik@YWR believes the most important driver of investment returns for the next 10 years will be avoiding the PE / VC crash and all its 2nd derivatives. Look at the growth of this industry. As recently as 2017 it was only $5.4trn. Then it rockets at an 18% CAGR for the next 6 years to almost $15trn. Returns boom which causes more money to flood into the asset class. Endowments like Princeton eagerly increase their PE allocations (from 15% in 1999 to 39% by 2024), but like all trends there are cycles and in Erik’s latest note he discusses the set-up for a big unwind which will play out for years.

Inferential Focus

AI challenges and timing

There is a lot resting on the growth of Gen AI, but there are some potential problems with anticipating its adoption including 1) Companies are struggling with how to use it. 2) Costs are dramatically escalating, but returns are not. 3) Challenges with training data. 4) Consumer wariness. 5) Significant impact on the electrical grid. Inferential Focus considers whether the current data centre buildout to support Gen AI adoption is similar to the broadband buildout in the mid-to-late 1990s. That did eventually facilitate Internet adoption, but not before some companies that had anticipated faster demand went bankrupt. The speed of adoption is critical. It could be slower than expected.

Behind the Numbers

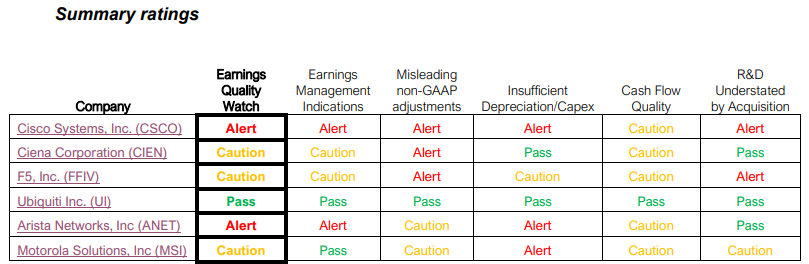

Communications Equipment: Earnings quality review

BTN’s Earnings Quality Watch industry reports provide readers with a quick way to identify the companies that are the most and least exposed to the risk of reporting disappointing results or guidance due to recent results being distorted by unrealistic, accounting-related benefits. Looking at the table above, only Ubiquiti received a ‘Pass’ rating in the Communications Equipment industry, while BTN sees meaningful risk that Arista Networks and Cisco Systems will disappoint on earnings in the next 2 quarters.

The Retail Tracker

NKE’s earnings release was a step forward despite management significantly cutting its forecasts. This should allow NKE to clear product and begin achieving estimates to restore confidence the company is at the bottom. The Retail Tracker has seen more colour added to assortments and some of the more recent drops have been very successful. In addition, trends are changing which should help basketball sales improve. They believe the shares are oversold despite visibility being uncertain, while their longer-term thesis remains intact.

Paragon Intel

CFO-Elect Monish Patolawala's ManagementTrack Rating* of 0.8 is in the bottom 4% of the 1,250 CFOs on the platform and is a significant downgrade to the 5.3 MTR of ADM's existing C-Suite. Patolawala destroyed (113%) alpha as a CFO at 3M; he has 9 "Level 2 & 3" career F.L.A.G. Risks (Financial, Legal, Audit, Governance Flags); a mixed incentive hit rate (achieved 50% of his incentive compensation targets 2020-2023); and is classed as an Inconsistent Sandbagger Guidance Forecaster (beats 51% and misses 28% of his financial guidance to investors).

*The MTR model employs a statistical ML algorithm to predict executive / company outperformance relative to their sector. It utilises 200+ signals and over a 10-year back-test a MTR long-short portfolio generated an average annual alpha of 8% with a 90% hit rate.

Portales Partners

G-SIB capital buffers under review

A regulatory attempt to massively increase capital requirements on the large banks, following amateurish behaviour by small banks that failed in 2023, has been delayed and watered down, given unprecedented opposition from banks / lawmakers. As a result, Charles Peabody anticipates a watering down and delay of Barr’s Holistic capital increases. In addition, he sees a possible reduction in G-SIB buffers which specifically benefits the large cap banks substantially (but not the regionals). While the main beneficiary is Citigroup, the bottom line of all this potential capital relief is that the major G-SIFI banks could emerge in 2025 with material excess capital. Thus, Charles expects a material step up in stock buyback programmes next year.

Veritas Investment Research

A materials company that behaves more like a low-volatility industrial - SJ needs limited investment to generate impressive FCF, which it can use to supplement organic growth with acquisitions, share buybacks and dividends. An earnings CAGR of 22% for the last three years improved ROE from 15% in 2021 to 20% in 2023. Veritas expects HDD EPS growth that is underpinned by risk-mitigating attributes, including contracts that lower volatility and commodity risk by passing through more volatile costs. With a lower three-year beta than comparable companies, the ~14x P/E and ~10.5x EV/EBITDA implied at SJ’s current stock price are appealing. 1-year TP C$120 (35% upside).

BWS Financial

ARLO recently announced it had reached 4m paid accounts approx. 4 months after achieving 3m accounts. While the pace of growth is most likely the result of catch-up calculations related to ARLO’s partner Verisure, this should not take away from the magnitude of the increase as Hamed Khorsand expects a portion of the sequential increase was the result of retail subscriber additions. He raises his 12-month TP from $17 to $24 (45% upside) ahead of the company reporting Q2 results supported by ARLO exiting 2024 with a higher ARR than he was originally forecasting.

Verbatim Advisory Group

Verbatim’s initial channel checks indicate that Q2 trends are drastically weaker on a Y/Y basis by 30% on average. Strong competitor offerings, lack of perceived need for advanced security solutions and budget constraints are reasons for lost sales. Q3 trends are also expected to be mostly weaker Y/Y. Verbatim also hears that there are no additional marketing efforts from CHKP to boost the sales pipeline. The company is either losing or having no changes in market share. While Fortinet seems to be gaining traction, particularly in the SMB space, they hear that Palo Alto is making headway in larger companies.

Boyar Research

Not only is SSNC trading well below precedent transactions and publicly traded comps, but with its proprietary AI technology its valuation also represents a sizeable discount to most of the other companies that are already capitalising on the AI megatrend. Boyar is also attracted to the firm’s significant recurring revenues, high margins, leading position in its field, less exposure to China, material inside ownership and strong FCF. They believe the earnings slowdown of 2022 and 2023 was a temporary lull in a longer-term growth story and therefore find the current valuation very compelling. Boyar’s intrinsic value estimate of $112 per share, offers ~80% upside.

Japan

JapaneseIPO.com

Despite its small size (¥76bn M/Cap), ESPEC dominates the environmental testing industry in Japan with a 60% domestic market share and a 30% global share. Environmental testing is often mandated by international standards, as well as national and industry regulations, and product development companies must conduct it. Thus, the company supports pretty much all new product launches. For this global niche status, ESPEC trades at a P/E of 14.3x and P/B of 1.3x. Its dividend yield is 2.5%. The test equipment leader, Shimadzu, trades at a P/E of 21x and P/B of 2.4x. In her latest report, Yuka Marosek looks at whether this valuation gap is justified.

Emerging Markets

Radio Free Mobile

Richard Windsor remarks on how Baidu is now the biggest & cheapest AI ecosystem in the world. While OpenAI is withdrawing from China, Baidu has already moved to fill the void as its users have jumped by 50% since Apr. There appears to be very little competition for the company in the world’s second-largest market, meaning that it could easily take the whole market and earn high margins on its revenues. Hence one would expect the shares to be riding high, but they are down over 15% YTD. No one right now wants to hear anything about investing in China which is exactly the time when one should consider buying.

CHA-AM Advisors

Fast food’s deflationary boom

Fast food has been a true nightmare in China in the past five years. First the pandemic then the inflation and then an odd period when menu prices were falling due to competitive pressures but costs were still inflating. However, these winds eventually swing around. Costs are now falling due to lower food prices. Add in increased efficiencies and more automation and margins are already recovering. The share price doesn’t seem to have noticed yet. David Scott's preferred play is Haidilao International, describing it as an "outstanding investment opportunity". However, he thinks the Asian industry as a whole now looks interesting. The average ROE of the 21 companies examined is 13% while the average EV/Sales is 1.8x. Other stocks flagged include MK Restaurants and Cafe de Coral.

Primaresearch

Primaresearch’s analysis reveals MRP’s traditional chains have had modest top-line growth despite considerable space expansion over the past nine years. They also calculate the chains’ trading densities (which MRP stopped disclosing from FY22) and find evidence of flat / declining results. These trends are surprising, considering the weak macroeconomic environment, which should have supported value retailers. Management is working on initiatives to exploit scale opportunities, but these may be limited considering the divergent business models of the companies. Primaresearch forecasts diluted HEPS of R13.17 for FY25 (+5.2% Y/Y) and downgrades the stock to Sell.

Alembic Global Advisors

MENA Chemicals: Street expectations are too demanding

During 2Q24, the average MENA petrochemical company’s share price declined 4.9%, outperforming the broader market by 1.2%. However, Hassan Ahmed’s analysis suggests that the Street’s estimates for Q2 are too demanding for the majority of these stocks. He expects tepid earnings growth Q/Q for most names and is meaningfully below consensus for Advanced Petrochemical Company and Industries Qatar. Similarly, he believes consensus estimates for FY24 are too optimistic. As a result, he lowers his 2024 earnings estimates for all seven MENA names that he covers and lowers his 2025 EPS estimates for six of the seven stocks.

Horizon Insights

China Tech: Survey feedback on semiconductors

The power semiconductor market is showing signs of recovery with Q2 seeing improved sentiment and Q3 potentially marking the bottom. MOS demand is rebounding for domestic manufacturers, while overseas firms are seeing eased inventory pressures. The rebound in consumer electronics is expected to benefit the likes of Yangjie Technology and JieJie Microelectronics. In the IGBT sector, as overseas inventory clears, new energy vehicle customers may increase adoption of domestic alternatives. Companies such as StarPower Semiconductor, CRRC Times Electric and Silan Microelectronics are well positioned to gain market share.

Macro Research

Developed Markets

Greenmantle

France: A minority government will not last for long

Niall Ferguson’s base case materialised in France, with voters electing a hung parliament. Yet, to everyone's surprise, the left-wing alliance NPF won the most seats in the second-round vote. The margin of victory is small and is the result of many triangulations in the last week when candidates dropped out to avoid splitting the anti-RN vote. Macron will now nominate a prime minister from the NPF alliance to head a minority government, but this might last only a couple of weeks before the new parliament votes it out again. Niall’s base case thus remains a technocratic caretaker government to take over this autumn and rule France until a new round of elections a year from now. Fiscal policy will remain basically unchanged and France will not throw the continent into a new eurozone crisis.

GFC Economics

US: Slower payrolls growth paves way for first cut

The case for a couple of Fed rate cuts is now cemented, according to Demetris Pachnis and Graham Turner. The pace of job creation is now in line with the ‘breakeven’ rate for payrolls. The jobless rate ticked up again to the highest number since November 2021, but this is a modest rise resulting from a supply-side shock rather than demand deterioration—big difference. It would be easy to get carried away, with many commentators likely to claim the Fed has fallen far behind the curve, but today’s backdrop is markedly different from previous cutting cycles. Given the clamour for lower Treasury yields, the bond market may overreact if there is another soft CPI print, but the secular trends driving long-dated bond yields higher over the coming years remain in place.

Steno Research

US: Three indicators to watch on recession risks

In Q4 2023 Andreas Steno laid out the roadmap to a recession, correctly forecasting that the re-acceleration in cyclical sectors would lead everyone to conclude that recession risks were off the table in 2024. Reality looks different. Andreas is watching three things to determine whether to be bearish on markets. First, the amount of withheld taxes has risen 7-10% year-over-year, something that he’s never seen before in a slowdown. Second, electricity output is on the rise. Third, the credit contraction is nowhere to be seen (see chart), with the SLOOS survey showing that credit conditions have bottomed out. Andreas strongly advises against betting on weakening markets when liquidity is improving. He remains SHORT USD, net LONG equity and crypto risk, and SHORT metals.

Beacon Policy Advisors

US: Reimagining the Presidency

Across the board, organisations on the right are calling to massively expand the power of the presidency. Should this come to fruition, large chunks of the institutional framework built up over decades to analyse how policies are made and implemented would no longer apply. One possible outcome of this would be for Trump to resurrect his previous attempts to use the rare tool of budget impoundment, a likely scenario given that Republicans will control both chambers of Congress. There are limits on a President’s ability to do this, but Trump has pushed against them before, including in 2019 with a deferral of funds intended for Ukraine. This is but one example of the many huge possible changes that the Beacon Policy Advisors team covers in their latest Spotlight Report.

CrossBorder Capital

Turning Japanese

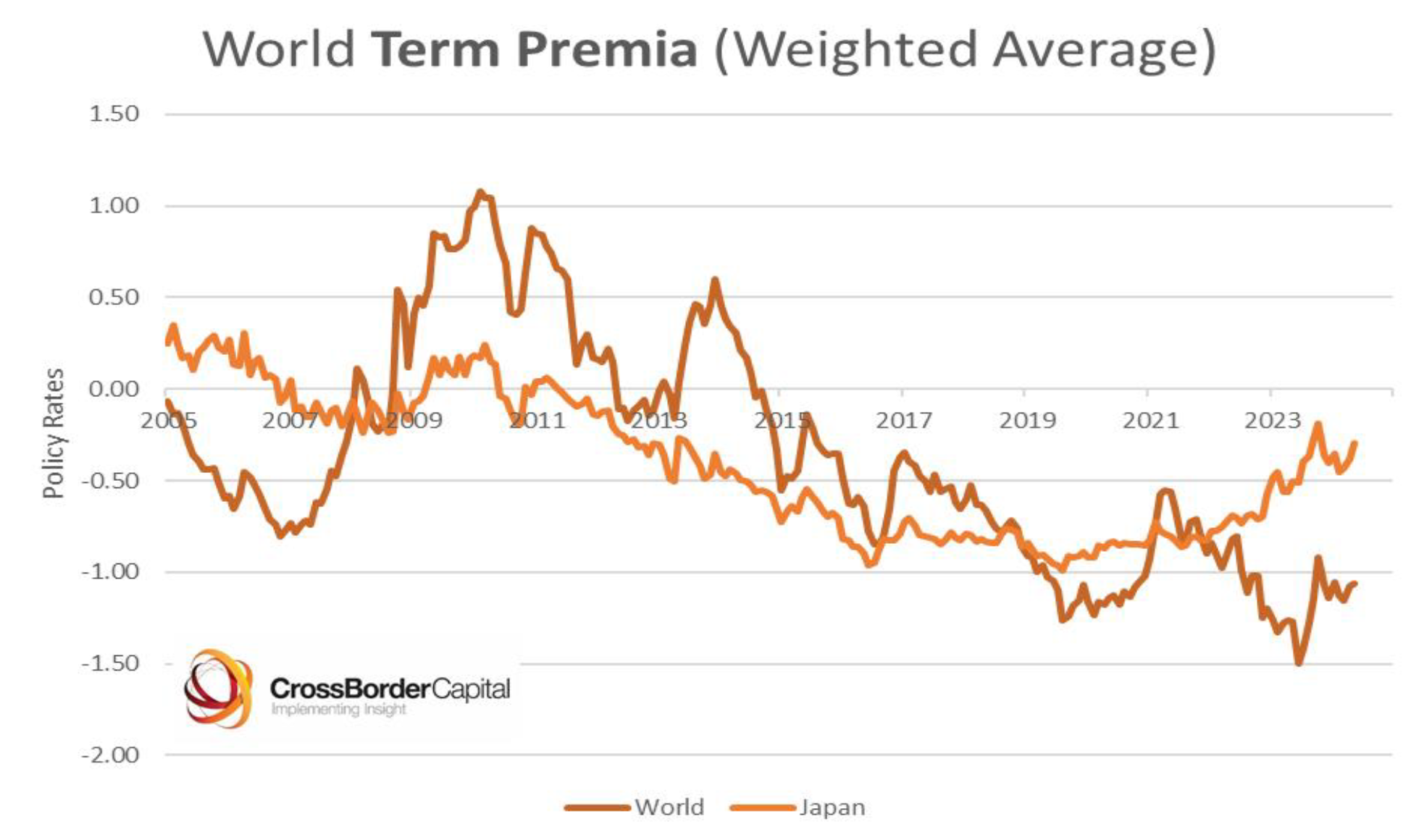

Japan’s skidding yen confirms a policy of monetary inflation. Japan was the first economy to plunge into deflation and it is now the first to deliberately re-start monetary inflation. Ageing, debt-burdened Japan is a bellwether for the West as the country’s fiscal needle pushes towards insolvency. The cost can be seen in the plunging exchange rate and fast-rising JGB yields, a result of a growing distrust of Japanese sovereign assets. Michael Howell argues that, despite the weak yen, monetary inflation will continue. 10-year JGBs could easily test 2-2½% yields and rising bond yields may spread internationally. Japan term premia often leads to world term premia (see chart); we’re all Japanese now, or will be very soon!

Japan Foresight

Japan: Tokyo elections deliver a warning

Tokyo Governor Koike Yuriko won a third term comfortably in July but a surprise second-place finisher points to growing public dissatisfaction with the politics. Both the Liberal Democratic Party (LDP) and the Constitutional Democratic Party (CDP) will have to adapt to this mood as they prepare for leadership elections in September. Although the LDP, along with its coalition partner Kōmeitō, backed the incumbent governor, the Tokyo elections were full of ominous portents for the ruling coalition, suggesting that voters could have an appetite for change that could result in surprising results in an election. In the immediate term, Tobias Harris says that the recent results will give a boost to politicians in the LDP calling not just for a leadership change, but for more fundamental reforms of the ruling party.

Emerging Markets

Totem Macro

Asian Financial Crises v.2.0

Whitney Baker believes North Asian financials will buckle under the one-sided mismatches they’ve built up in US assets, with losses buried under the veneer of tech-geared equity gains. Liabilities are being contracted by policymakers’ own misguided attempts to defend currencies. Shrinking monetary bases force bond sales, crowding out stocks. Asian sales of US bonds add duration back to the US, aligning with a shallow American recession. Despite ongoing investment in infrastructure, the Fed will overreact with rapid rate cuts, causing a rotation out of US stocks into bonds. As Asians repatriate funds, the dollar weakens, triggering asset declines. Eventually, renewed Fed printing sets the stage for a stagflationary recession. Bottom line: in AFC v.2.0, the Asians are the creditors with too many foreign assets, while the US is the EM with too many foreign liabilities.

Alberdi Partners

Argentina: Should we worry about the Treasury’s short-term debt?

The stock of zero-coupon ARS-denominated LECAPs soared in recent weeks, with the total outstanding value reaching ARS17.8trn. On top of this, the government is in conversation with banks to transform ARS13.3trn of reverse repos into a new note. Marcos Buscaglia examines the evolution of short-term ARS Treasury debt in the next 12 months. In the base case scenario, the evolution of short-term debt does not balloon. Even if the BCRA has to sterilise the equivalent of $300m per month, the debt is still not unstable. For instability to occur there needs to be either a new issuance in high quantities, a much higher increase in real interest rates, or a cessation of the upcoming devaluation.

Rosa & Roubini Associates

China’s wargames in the Indo-Pacific

Although the US and China seek to rekindle ties, Indo-Pacific security is a major flashpoint. China’s Digital Silk Road (DSR) is a multi-tiered mega-infrastructure project aimed at expanding Beijing’s influence and technological foothold in the Indo-Pacific. The DSR is representative of China’s hybrid warfare, fusing both traditional combat with covert intelligence operations. The emergence of new, pro-China leaders in the region delineates a shift in regional politics and a renewed trust in Beijing. China’s enormous investment in the Indo-Pacific states is shrouded in uncertainty and challenges the interests and sovereignty of regional nations. As the US and the greater Western order attempt to challenge China’s growing sense of hegemony, Beijing’s wargames continue to intensify in the region.

Signal Risk

Kenya: Protests run out of steam

Anti-government protests planned in several urban centres, including Nairobi, failed to materialise on July 4th. This comes after protests calling for President William Ruto to resign took place in multiple areas. Those protests followed mass demonstrations in June to denounce the Finance Bill 2024, which Ruto has since withdrawn. Several reasons account for failed demonstrations, including concessions put forward by Ruto, the lack of a coordinating body, apathy among activists and lack of public support. These factors and additional concessions by Ruto suggest that further major protests are unlikely in the immediate term.

Grey Investment

Korea: Adding to the long

The Kospi 200 weekly close above 385 is viewed as a breakout from a 14-week consolidation, targeting 410 (chart 1). Last week’s strong showing has taken RSI up to 69, just below overbought 70. Chris Roberts is now 100% long from 325.60 and is moving the stop on this position to a daily close below 344. He adds another 10% at market and 10% at 388.50, with the stop loss at a daily close below 355. Chris Roberts’ longer-term target stays at 500+, with the index remaining in a secular uptrend.

Copley Fund Research

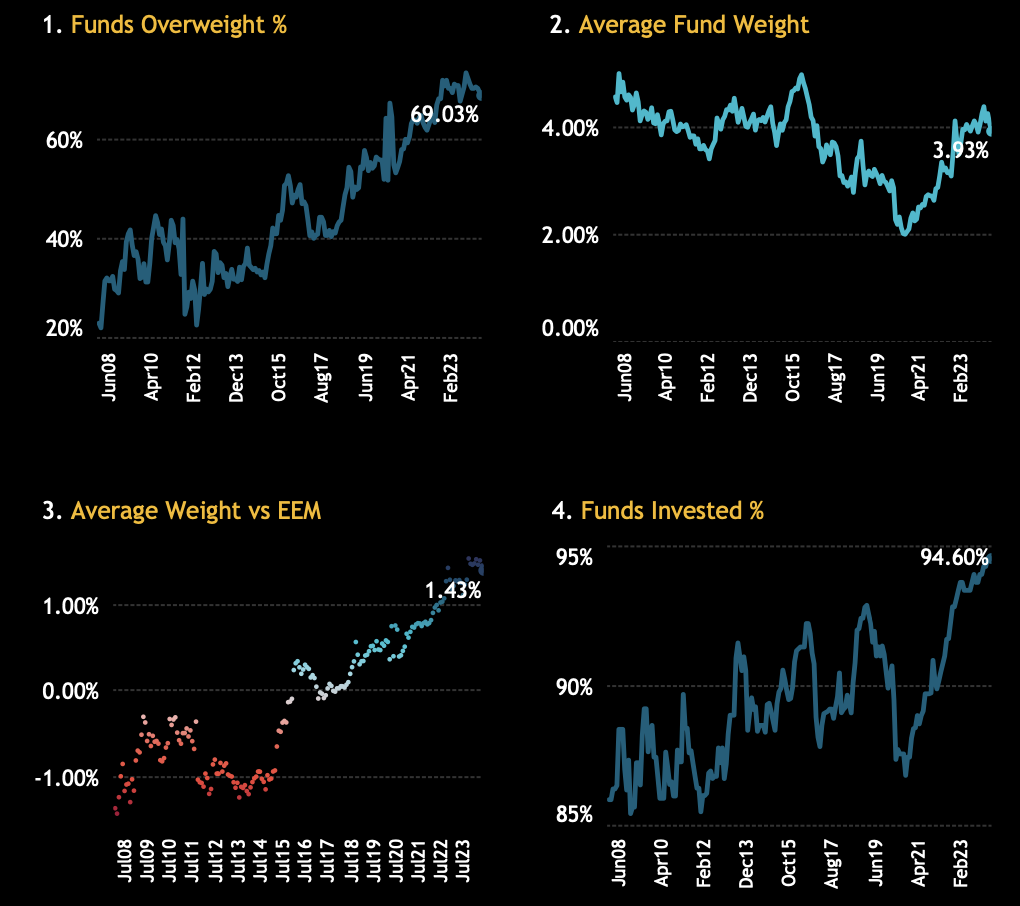

Mexico: GEM funds wrong footed after election results

Active GEM fund managers were caught off guard with their exposure to Mexico heading into the election. The nation had benefited from increased inflows and exposure over the past 3-4 years, with the percentage of funds invested reaching an all-time high of 94.6%. However, the country’s positioning against the benchmark is where it truly stands out, with the percentage of EM funds overweight the benchmark now at 69% compared to just 20% in 2011. This proved costly in the wake of the elections, with crowded stocks like Banorte experiencing big price declines. As it stands in the EM space, Mexico is the largest overweight by average fund weight and the second most common overweight after Indonesia.

Emerging Advisors Group

Kazakhstan: Next on the list

After Russia, Kazakhstan has the second strongest credit cycle in EM, with a clear surge in local demand and real activity. Just as in Russia, Jonathan Anderson believes the Kazakh economy is hitting peak domestic growth, as external incomes are flat, and the central bank is maintaining high nominal and real rates. In terms of markets, current KZT valuation looks supported by rates, and Jonathan also has no problem with current sovereign dollar yields, but he does have concerns about the recent massive surge in equity prices and multiples.

Commodities

Vanda Insights

Crude: Shook up

A bidding frenzy in the Platts North Sea crude assessment window that spurred a Brent rally ended up subsiding last week, but prices continued to crawl higher. Vandana Hari recently noted how the key elements of the market surrounding the prolonged rally were not adding up, making the continued ascent more mysterious. Market sentiment is split, with the bulls calling for $90 and sceptics seeing it as a stretch, but Vandana sees no clear factors on the horizon to sustain a price in the $90s and sees the risk as skewed to the downside. Meanwhile, the market will have to deal with the potential speculative positioning resulting from the unravelling of Biden’s campaign against Donald Trump.

10x Research

Bitcoin: Heading down

10x Research’s initial downside target of $55,000 has been reached, although a countertrend rally is expected as Bitcoin appears oversold in the short term. Additionally, the SEC may approve the Ethereum ETF, presenting a short-term but not medium-term buying opportunity. Should a rate cut arrive soon, the cryptocurrency may be pushed above $60,000, although prices will struggle to sustain above this level. The team’s short-term reversal indicators are deeply negative, suggesting a potential rebound before a possible second leg down. As long as it remains below $61,000, expect prices to drop to $50,000 during August/September, potentially falling significantly lower in the face of a US recession.

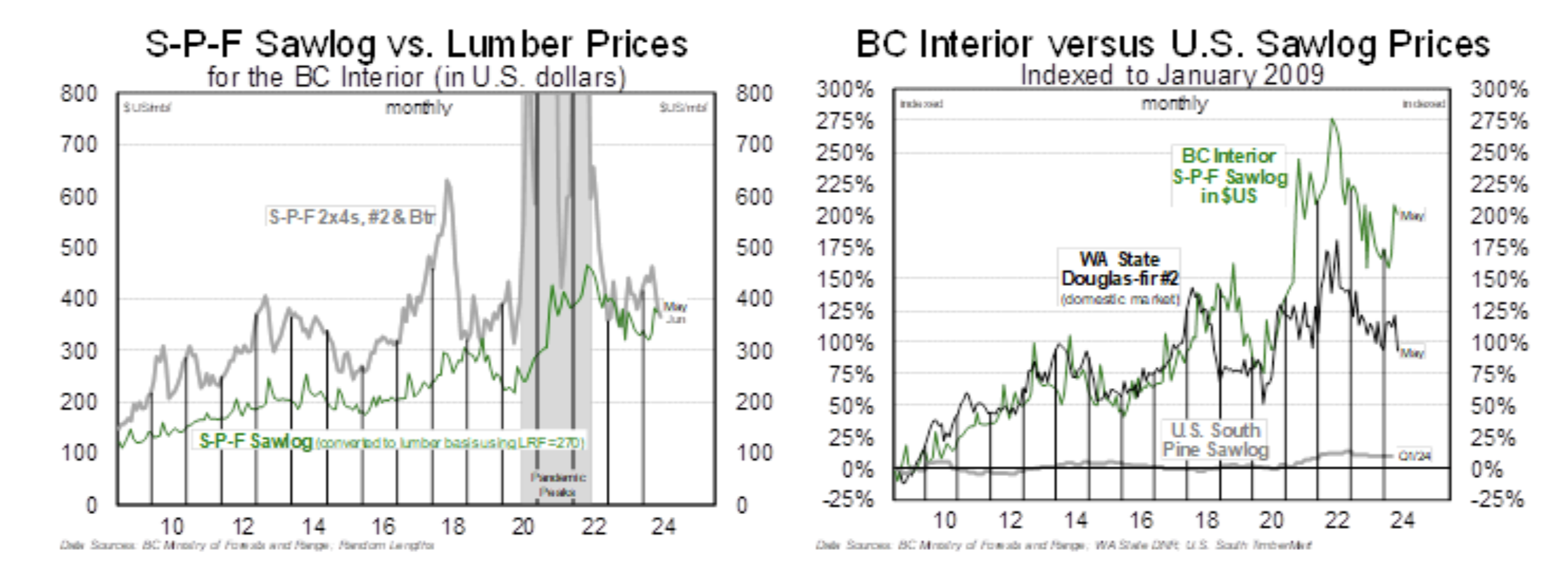

ERA Research

BC lumber producers facing it tough

BC log costs are moving higher again (chart 1), and with S-P-F lumber prices rolling over—2x4 prices recently declined to $332—the ERA Forest Products team believe that the majority of BC sawmills are losing money today. Lumber prices are slumping across all species and dimensions, but log costs in BC are significantly higher (chart 2). More downtime is needed in all regions to remedy the issue. How to trade it? Most names will see limited further downside from current levels and upside catalysts remain elusive for now. The team do see long-term value in Canfor ($18 target price), Interfor ($22) and West Fraser ($116) but recommends that investors wait until at least Q4/2024 before building long positions.

Futurestechs

Gold: Continued bullish outlook

Most of Friday’s gains were given back yesterday, but the bulls may be able to get this back on track to retake 2380.9. There is a lot of bearish divergence action on the momentum studies and a MACD sell signal, but the price hasn’t agreed in a sustained manner and now MACD is back to long. New all-time highs on May 20th haven’t been emulated or exceeded since, but key support around 2280-85 is holding. Buy dips. Bullish view, aiming for 2478-2500 next. [Published July 10th]

Astris Advisory Commodities

Met coal rally underway

Prices have rallied $30/t so far after supply disruptions in Australia and elsewhere served to tighten the market, even despite Indian spot buyers remaining largely sidelined by the monsoon season. With Anglo’s Grosvenor mine now likely out for many months, FM contract cancellations will leave the Indian mills needing to buy even more spot material when they return in coming weeks. Prices should continue to build through H2/2024. Indian mills usually start to return to the spot market around mid-July to line up the spot shipments to arrive post monsoon (Sept) when they ramp steel output, and while there will no doubt be many mini-cycles along the way, Ian Roper continues to look for prices to exceed $300/t in 4Q and potentially spike even higher into the new year.