Company & Sector Research

Europe

Propitious Research

Profitable growth, elevated discount - after effectively removing the cross-holding structure between PRX and Naspers and simplifying its holding in Tencent and other subsidiaries, there has been little impact on their respective discounts to NAV with the Tencent share price and continued open-ended share repurchase programme remaining the main share price drivers. Wium Malan has historically argued that PRX warrants a c.25% (and NPN a further 15%) holding company discount. In his latest report, Wium analyses this discount to NAV, the performance of its underlying consolidated operations, cash flow generation, capital allocation and valuation.

Smart Insider

Anas Abuzaakouk (CEO since 2017) purchases €2.2m of stock at €66.96. He has been a regular buyer with 22 previous purchases and while the size of this latest buy is in line with his history, it is notable given his good track record and the fact that he is buying into strength. He last bought shares at €40.72 in Oct 23 and he is now paying a price more than 50% higher. Furthermore, Guido Jestädt (Chief Admin Officer since 2021), who boasts a better than average record when it comes to share purchases, has also increased his stake in the company. As a result, Smart Insider ranks the stock +1 (highest rating).

Forensic Alpha

Forensic Alpha’s proprietary machine intelligence performs a detailed forensic analysis of a company’s financial accounts. They continue to categorise SOBI as Very High Risk, with the number of red flags staying consistently high over the past 6 months. The areas of greatest concern are Accounting (including DPO hitting a new high in Q2, +24% Y/Y to 76 days) and Governance (the CEO’s bonus scheme is >50% weighted to revenue which is highly unusual and is likely to encourage a “growth at any cost” mentality; and concerns re. the independence of the Audit Committee members). Forensic Alpha has also identified issues with Earnings Quality, in particular relating to OCF.

Iron Blue Financials

Following publication of the company's FY23 annual report, Iron Blue increases their SECUB score from 23/60 to 26/60 (now top quartile / fertile grounds for shorting). This reflects: 1) Sustained elevated stripped out costs. 2) Trade receivables days outstanding compressed at a decade low. 3) One third of debt scheduled to mature during FY24. 4) Sizeable fair value adjustments applied to Stanley Security’s balance sheet. 5) A new contingent liability concerning a US government investigation. 6) Another increase in the rate of employee injuries.

Messels

FTSE 100 stocks & sector review

Messels currently has 19 long positions in their FTSE 100 Momentum portfolio having closed their position in Rio Tinto after it pulled back in the five-year range and broke medium term relative support. They remain overweight Retail and in particular, Howden, Tesco and Marks & Spencer which maintain uptrends and JD Sports and Kingfisher which renew base formations. Other stocks highlighted in their technical review this week include Informa, which has rallied back to the highs and rallies from relative uptrend support; while M&G finds 18-month uptrend support and develops a base at the bottom of the relative range.

North America

280First

AI driven 10Q / 10K text analysis

Since there are always reasons when companies change the wording in their financial filings, being alerted to these changes allows investors to realise potential risk factors and opportunities before they are reflected in the market, ideal for idea generation and portfolio monitoring. Recent alerts include: 1) Broadcom - considering a dividend cut? 2) Costco - worldwide renewal rate may be adversely impacted. 3) Eagle Materials - takeover target? Customer consolidation concerns; long term financing needs. 4) Haemonetics - material reduction in per unit pricing by its largest customers. 5) Intuit - rethinking the trajectory of service revenue?

Periphery Research Partners

New tactical short idea from Hesham Shaaban - the key metric here is North American APRU, given not only the materially higher ARPU differential vs. International, but also because there is limited if any DAU growth. Hesham doesn't believe SNAP has shown enough to suggest that it is about to hit the new reported high in second half ARPU that consensus is expecting. The company likely can't get to Street 2H24 revenue estimates without doing so. The only reason he is not fundamentally bearish is because it is still possible that SNAP could eventually find a way to drive meaningful engagement beyond chat (although there is little evidence of this so far).

JJK Research Associates

Janet Kloppenburg’s latest assortment reviews have increased her confidence that both A&F and Hollister can deliver meaningful 2Q24 revenue / margin upside, driving EPS results nicely above expectations. At Hollister, she is encouraged that summer clearance levels and discount rates appear to be tracking well below 2Q23, while recent new assortment flows are much improved. At the A&F brand, assortments remain well differentiated and fashion leading; Janet sees continued success in the brand’s diversification strategy into multi/use-occasions. She raises her 2Q24 EPS estimate to $2.35 with FY24 forecast of $10.15.

Portales Partners

Charles Peabody discusses the 33% Q/Q jump in NII to $2.2bn, drawing attention to the $815m figure in the Global Banking & Markets unit (which could have added as much as $500m to revenues, or $1.15 a share to EPS) and questions the sustainability of the bank's financing revenues. The bottom line is that Charles believes that the stock is nothing more than a momentum play and will unwind quickly once the capital markets prove hostile. Contrary to management's commentary, its earnings stream is still very cyclical and not deserving of a premium valuation.

Ben Jones Investments

IBKR has $497bn of client assets which it has grown at a 27% CAGR over the last 15 years. Its advantages over competitors include paying higher rates on cash deposits, a wider range of traded products and being among the lowest cost brokers. IBKR maintains 70% operating margins while paying 4.83% on USD deposits. No competitor can pay such rates without making losses, because they offer additional wealth management services that are lower margin. In other words, it has a niche that can't be matched. Ben Jones expects IBKR to continue growing client assets and cash flow in excess of 10% p.a. and believes the stock trades at a significantly lower valuation than such cash generation deserves.

Huber Research Partners

It was a great quarter with MCO beating expectations and raising its FY24 adjusted EPS, but management’s guide still appears conservative vs. Craig Huber's Street-high estimate of $11.60. Heading into the print, he had already increased his 2Q24 and 2024 EPS estimates given ongoing better than expected debt issuance trends in US and Europe. For 2025 and 2026 he estimates EPS of $13.80 and $15.70, respectively. Craig retains his long-held Overweight rating on MCO which is in a long-term secular uptrend in Ratings and Moody’s Analytics. His revised 12-month TP is $500.

Thompson Research Group

TRG has long stated that JELD does not have a sales problem but a cost problem. Years of mismanagement has created a huge internal investment and operational improvement opportunity, this sets up a compelling opportunity for investors. JELD sells at ~6x FY24 EBITDA guidance, which TRG believes is a low multiple on the low point of EBITDA. At this moment, Europe EBITDA virtually offsets corporate expenses. Valuing JELD on its North America segment alone on future EBITDA of $441-466m (using a conservative assumption that in 2-3 years the housing market has improved and sales rise 10-13% at a margin of 13.5-13.9%) could yield substantial upside in the stock price.

Kailash Capital Research

Investors seem to believe the business is more cyclical than it is causing OC to trade at a far steeper discount to the market than it deserves. Management has successfully raised prices and controlled costs meaning its financial results look more like those of a growth company. Yet its shares trade at <14x earnings and an EV/Adjusted EBITDA of just 7.3x. Both figures represent >40% discounts to the S&P 500 Index. KCR also finds it notable that both their Large Cap Value and Large Cap Core models rank OC in the top 100 despite significantly different loadings. When a stock is highly ranked across models with divergent mandates, it signifies greater potential interest across the investor base.

Hedgeye

Given his recent supply chain checks and conversations with industry players, Felix Wang believes the company’s liquid cooling backlog and revenue expectations are too high. While supply bottlenecks are improving, he is particularly worried about some of the new liquid cooling technology out there. As a result, VRT's price-cost tailwinds of >$65m for FY24 may become harder to achieve. Felix also argues VRT's relationship with Nvidia is not really a game-changer and tracking new data centre construction he notes the pace has slowed in 2Q24. The stock looks very expensive at 34x FY25 P/E and 23x EV/EBITDA. While the long-term picture of liquid cooling is constructive for data centres, there is uncertainty on when / how it will play out. 35% downside.

Pernas Research

The future digital manufacturing leviathan - XMTR came to market too early and at too high a price, which has contributed to a near 85% sell-off over the last 3 years. Sentiment has clearly soured. However, the market is being overly punitive re. its business fluctuations and is even mischaracterising its business model. Investors are missing the fact that the company is a major lever on the massive digital transformation silently underway in non-contract manufacturing. XMTR will continue to scale and exhibit operating leverage as it grows revenues. The stock is already up 25% since being added to the Pernas Portfolio in early July, but plenty of upside remains.

Off Wall Street

NUE “beat” a much-lowered bar for 2Q24 EPS, but gave weak 3Q24 guidance. Street estimates are still too high for 2H24. Off Wall Street’s thesis is playing out. Since peaking at ~$200 earlier this year, the stock price is down more than 20% in an up market. The problem for bulls is that, even as the stock price has been dropping, NUE isn't getting any cheaper, because EPS estimates are dropping just as fast. The shares trade at 14x consensus EPS for calendar 2025, but OWS thinks those 2025 consensus estimates are probably a chimera. Their TP of $110 (30% downside) implies a similar 13.6x multiple on their own $8.08 EPS projection for 2025.

ETR

Technology Spending Intentions Survey

ETR’s July 24 TSIS saw participation from 1768 IT Decision-Makers, including 293 Fortune 500 and 419 Global 2000 organisations. Highlighted vendors include:

Equinix (EQIX) - rising sector and vendor-level spending intent places EQIX in a dominant position among peers, as the vendor seems well-aligned with broader IT spending and ML/AI trends, warranting ETR’s first-ever positive outlook on the data set.

Salesforce (CRM) - souring spend intent for its core Enterprise Apps business, in tandem with overall Net Score in Cloud Computing registering sharp declines, warrants a negative outlook.

Varonis (VRNS) - Negative outlook. ETR has observed a clear declining trend in spending intentions for two years, with an even lower Net Score among the Global 2000 and a sharp rise in Replacement intentions among existing customers.

Japan

Galliano's Financials Research

Kyoto Financial’s stakes in 3 key listed Japanese corporates are valued at over 85% of its market cap with its total equity holdings accounting for 130%+ of its market cap. However, management intends to retain the bulk of these positions, opposing the growing trend for Japanese listed companies to unwind crossholdings. Given this decision, combined with underwhelming fundamentals (e.g. not as well geared into rising domestic interest rates as peers; neither is it well exposed to potentially rising benchmark rates through BoJ deposits; and unattractive valuation), Victor Galliano is negative on the stock, preferring the likes of Resona, Mizuho and SMFG instead.

Asymmetric Advisors

At 0.65x PBR with balance sheet net cash and on 12x CoE of OP +25% Y/Y after +80% last FY, this still looks good value despite its rise from 0.4x PBR at the start of 2024. Foster is the global No.1 supplier of car speakers on an OEM basis and is entering an upturn as car makers switch from prioritising investment in EV batteries to improving interiors and the numbers of speakers per car is rising whilst speakers are being incorporated for non-entertainment purposes such as proximity alerts which are becoming semi-mandatory. Foster has also fully exited and taken close down losses from its consistently loss-making i-Phone earphone business.

JapaneseIPO.com

A global leader in wafer reclaiming with a 33% market share - RST is a less cyclical semi stock, as its low cost reclaimed wafers allow semiconductor manufacturers to continue investing even during industry downturns. The company has also expanded into the alternative energy battery sector, which is poised for significant growth. The stock trades on a P/E of only 12.6x and a P/B of 1.7x, while RST is still small with a market cap of ¥92bn which explains some of the discount to peers, Yuka Marosek thinks the stock is too cheap to ignore.

Emerging Markets

Blue Lotus Research Institute

2Q24 results to beat consensus forecasts driven by resilient catering demand and easing competition. Catering is the bright spot under the current weak consumption environment and Blue Lotus expects Meituan’s on-demand orders to increase 15.5% Y/Y in Q2 with average profit per order up 2% Y/Y, following successful marketing campaigns via Shen Qiang Shou and Pin Hao Fan. They also observed two catalysts that positively impacted the OPM of Meituan’s in-store business: 1) The competitive environment further eased as Douyin began to raise commission rates. 2) Integration of its “super membership” started to convert users from low margin food delivery into high margin in-store. Meituan is their top pick in the e-commerce / O2O sector. TP HK$160 (50% upside).

Arete Research

Arete raises their TP to NT$1,437 after increasing their estimates for both FY24 and FY25. Key points post Q2 results include: 1) Sales from AI processors are expected to triple this year and with AI players planning to shift to leading-edge over the next few years, Arete believes TSMC will make N2 family capacity much larger than for prior nodes. 2) Expects TSMC to raise wafer prices 3-8% for N5 and N3 customers starting 1st Jan 2025; can deliver 55%+ gross margin in FY25E. 3) Potential upside from AI PC and AI smartphones in 2025. 4) Geopolitics - outsourcing chip manufacturing to TSMC at leading-edge is clearly an economic win for US companies - a point at odds with recent Trump comments.

Macro Research

Developed Markets

Vermilion Research

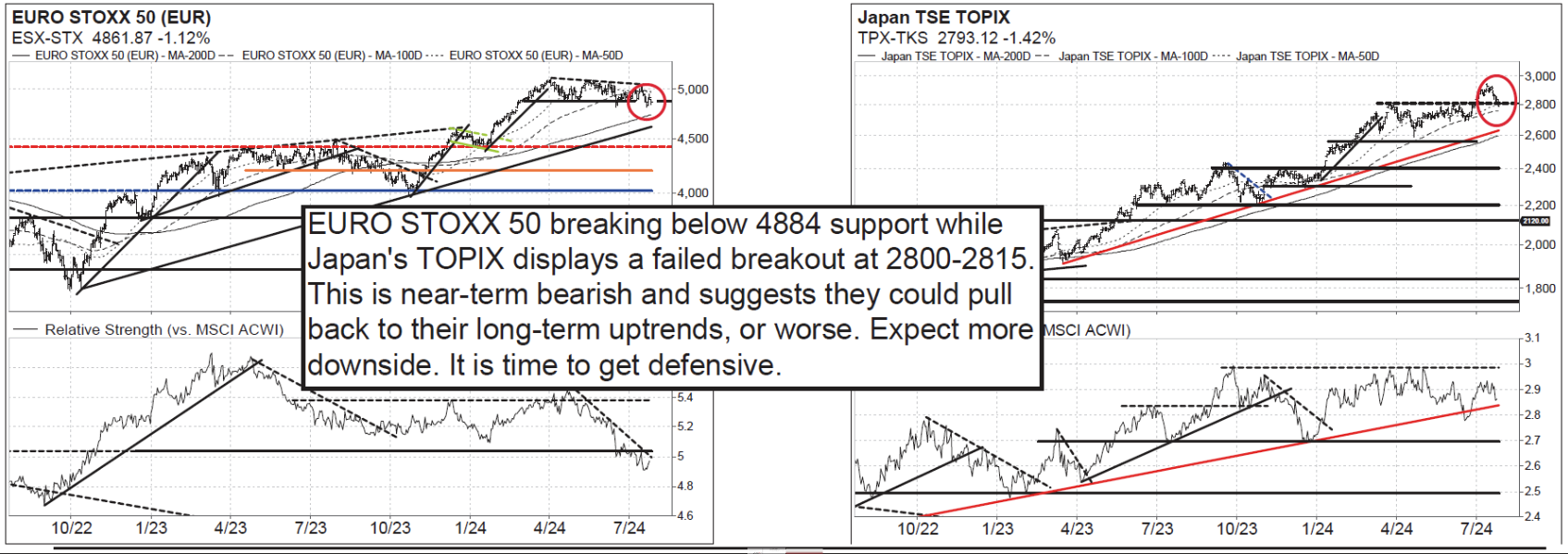

Pullback Underway

Vermilion’s long-term bullish outlook since Nov 2023 remains intact, but the team believes a 1-3 month pullback has begun. Supports to watch are at $110 on MSCI ACWI (ACWI-US) and $41-42 on MSCI EM (EEM-US), and whether these levels hold or not will determine the severity of the pullback. The S&P 500 is violating its 20-day MA, Europe's EURO STOXX 50 is breaking below 4884, and Japan's TOPIX appears to be staging a false breakout at the 2800-2815 level. This all points to more sideways to lower price action in the near-term. Global value sectors have continued to outperform in recent weeks and this area remains the team’s main focus. They are interested in defensive sectors as global equities pull back.

Radio Free Mobile

AI: The disconnect

Richard Windsor suspects that genAI services make up only a tiny percentage of the revenue in companies like Alphabet, despite massive investments. This is a more serious problem than the overinvestment in internet capacity in 1999-2000 because the dark fibre sat there until it was needed. In contrast, AI technology evolves so rapidly that it could become obsolete by the time it's needed. 2020 was supposed to be the year of realised AI revenue, yet there is little sign of this—Richard’s research concludes an absurd going rate of 142x revenue to sales. He remains content with his AI adjacencies of interference at the edge, where he owns Qualcomm, nuclear power, and a basket of physical uranium funds, ETFs, and uranium miners.

Eurointelligence

US/EU: Further across the pond

With Biden goes the last of the great US trans-Atlanticists – Wolfgang Münchau points out that there are no more Democrats who will follow in the same tradition. The EU needs to prepare for the shifting US political landscape on both the Republican and Democrat sides. Interests are diverging, and as fiscal constraints kick in, the US will be even more reluctant to engage in international ventures that carry no domestic political pay-off. The discussion about Europe’s self-sufficiency often narrows down to defence spending, which is certainly important, but Wolfgang believes Europe’s reliance on US technology and the fragmentation of economic policy, including capital markets and services, is far more critical.

ACG Analytics

US: Democrats hit reset!

By declining to run for a second term, President Joe Biden has breathed new life into the Democratic Party. As Biden’s replacement, Harris will be able to retain the money raised thus far for Biden’s re-election. The proverbial next piece of the puzzle is who Harris will select as her running mate. Will she go with a centrist like Gov. Steve Beshear (D-KY) who could go head-to-head with Sen. J.D. Vance (R-OH)? Does she make a play for the Tar Heel State—a state which Republicans cannot afford to lose—by choosing Gov. Roy Cooper (D-NC)? Does she double down on abortion and turning out women by picking Gov. Gretchen Whitmer (D-MI) who happens to lead another competitive state? The choice will reveal just what strategy the newly energised Democrats choose to employ in defeating Trump.

TenViz

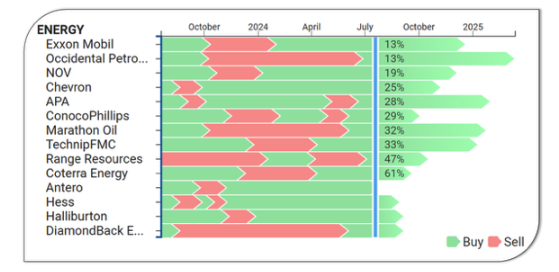

US: Investing in a Trump Presidency

Tenviz has an impressive record of forecasting unexpected political outcomes before they happened, including Brexit, the Covid lockdowns, the WTI oil price drop in 2023, and growing political tensions in France along with their subsequent reversal before the election surprise. Konstantin Fominykh advises investors to follow markets to forecast politics, not the other way around. His recent BUYs reflect a possible Trump win. Energy is an obvious contender, and Konstantin has new buys on the likes of Exxon Mobil and others (see chart). He also sees positive upside for Big Pharma, which will be subject to fewer price controls, and a preference for mid and small caps as they benefit from higher tariffs and lower interest rates.

AAS Economics

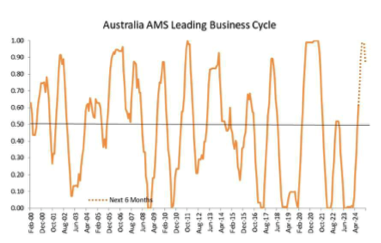

Australia: Cyclical down under

The Reserve Bank of Australia is now running one of the most aggressively contractionary policies among the major central banks, but money supply (AMS) growth has turned positive, driven by bank deposit growth. Overall, the economic growth outlook is flat to modestly positive, and Frank Shostak expects unemployment to move slightly higher. CPI inflation should continue its steep decline, possibly moving into deflation next year. Frank sees the RBA as likely to commence cutting target rates in the near future and asset allocations are – for the next few months at least – pro-cyclical.

ABCG Research

New Zealand/Canada: On the fall

In the previous week, NZD/CAD experienced a sharp decline due to a combination of weaker fundamentals, bringing it to a critical support level around the 0.8200 area. Despite the steep fall, the RSI has not yet reached oversold territory. NZD/CAD is also trading below the 50-day SMA and has crossed below the 200-day SMA, indicating a larger, longer-term trend reversal. The outlook remains bearish in the short term, but investors should consider capitalising on opportunities if it manages to hold the 0.8200 area.

Emerging Markets

PRC Macro

The post plenum mood

At the close of the Third Plenum, William Hess believes that a key question is whether the contradictions in the published Resolution will cut in favour of animal spirits, value creation, and productivity, or the expansion of regulation and bureaucracy in the name of reform. For example, there is encouraging language on preventing the government from improperly interfering in price formation in the utilities and transport sectors, yet some level of intervention is still implied, and it is unclear what for. Additionally, all areas slated for reform will be subject to the creation of “mechanisms”, code for new bureaucracy. The resolution also mentions the need to strengthen Party leadership, military, and social risk prevention/surveillance as preconditions for realising “Chinese style modernisation”, and this reality has to be weighed against the call to liberate social productive forces.

Horizon Insights

China: Risk aversion

Amid a weak recovery and challenges in the overall economy, equity fund managers demonstrated significant risk aversion in Q2, heavily favouring cyclical/value stocks and the electronics sector. The fragmented market can be categorised into three main styles: cyclical and value, growth and technology, and pharmaceuticals and consumer goods. From the Q2 public mutual fund performance reports, fund managers have a mixed outlook on China's economy and equity market, expressing concerns over short-term risks and challenges while also maintaining optimism about policy adjustments and long-term economic transformation. The stability of the real estate market and high-quality development will be key areas of focus moving forward. As the economic cycle ascends, market sentiment towards growth stocks will recover, with corporate profitability and market valuations likely to resonate upwards.

Emerging Advisors Group

South Africa: The endless wait for SARB

The economy continues to flatline in real terms, with nominal growth at an all-time low. Rates are stuck at record highs, with long yields at record levels and SARB keeping short rates at a 15-year high as well. As a result, South Africa’s public debt ratio continues to rise at a rapid pace despite a very conservative fiscal stance. Unlike Brazil, where the policy onus now falls equally on the central bank and the treasury, in South Africa the ball is almost completely in SARB’s court, waiting for a combination of rate cuts and QE measures to rein in long yields. Until that happens, Jonathan Anderson sees the main silver lining of the current high rates/no growth combination is that the external balance is back in surplus, the rand is stable, and fixed income and carry returns are very attractive.

Aurora Macro Strategies

Ukraine: Debt restructuring deal is ambitious

Ukraine’s preliminary sovereign debt restructuring deal balances short-term downside risk protection for creditors against substantial debt relief for Kyiv. However, the restructuring is also clearly ambitious given its reliance on unrealistic IMF growth and debt sustainability forecasts, setting the stage for a potential second restructuring around 2027/2028. Max Hess continues to consider the GDP warrants effectively worthless - a view reinforced by the fact that the deal removed cross-default provisions to those warrants. Meanwhile, Russian forces continue to make creeping advances on the front across Ukraine’s Donetsk region, particularly in its south. Max believes that it is likely that Russian forces will control almost the entirety of the Donetsk region for the first time ever by year’s end if the current pace of Russian advances continues.

Greenmantle

Venezuela: Maduro’s last stand

Opposition Edmundo remains on the ballot with a high polling lead and Niall Ferguson sees a low likelihood of him being removed ahead of election day. President Nicolás Maduro’s likely strategy of electoral fraud runs contrary to all reliable polling. If there is no fraud, Edmundo should win by a landslide, with clear upside for Venezuelan bonds—Niall does not expect secondary bond trading sanctions to be implemented regardless of the outcome. If Maduro chooses to steal the election, Niall believes he is unlikely to succeed. In his base case, he would expect Venezuelan assets to rally as markets price in the political transition away from Chavismo. This represents a huge opportunity for the country and its assets over the coming years.

ESG

Adelwise

Investment trends in seaweed startups

Interest in the global seaweed startup sector has surged over the past 20 years, driven by the recognition of its vast potential and numerous opportunities. Given the complexity of the industry together with lower investor interest in sustainable solutions, it has shown signs of fatigue in the past couple of years. However, Sophie Biro-Rouillon sees this as a transitory phase of a strong secular trend. Seaweed can address the triple crisis that encompasses climate change, pollution and biodiversity loss. Sophie has previously identified 27 publicly listed companies worldwide with exposure to seaweed and with a market cap >US$500m. The sector remains predominantly a private equity asset class.

Sustainable Market Strategies

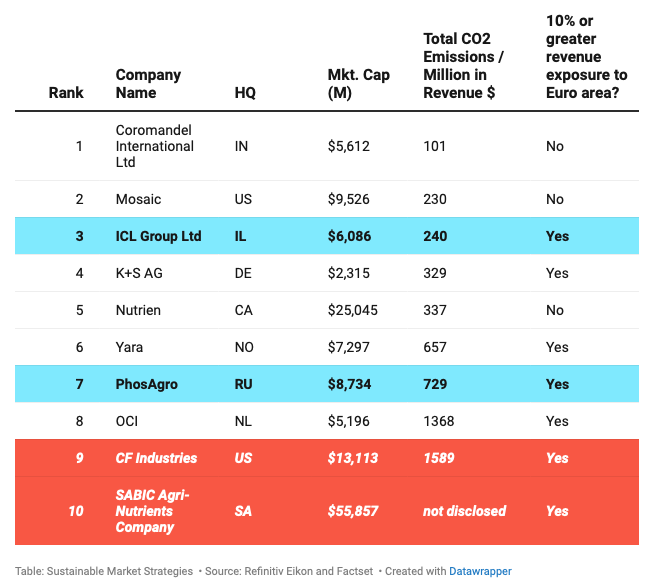

The winners and losers under the EU’s Carbon Border plan

The Carbon Border Adjustment Mechanism (CBAM) is an EU policy tool designed to address carbon leakage – when companies relocate their production to countries with less stringent climate regulations – and to promote carbon neutrality. CBAM has been in a “transitional phase” since the end of 2023 when importers of steel & iron, aluminium, fertilisers, cement, electricity and hydrogen became required to report carbon emissions. In 2026, importers of these goods will also need to buy CBAM certificates. The CBAM will erode any competitive advantage for companies that are not currently subject to paying a carbon price on par or above the cost of carbon in the EU. Only the fertiliser (see chart), aluminium and steel industries are likely to see considerable disruption, but there are still a handful of long and short candidates for investors to consider.

Commodities

Vanda Insights

Oil: Low appetite

Unforeseen influences have surprised crude prices to the upside, with each occurring in bouts but some having left a longish tail of risk premium in crude. Vandana Hari correctly predicted that although there has been an undercurrent of support in recent months, from renewed expectations of a soft US landing and two 25bps Fed rate cuts, this wasn’t enough to sustain Brent in the mid- to high-$80s. European and Chinese oil appetite also remains lacklustre and an entrenched manufacturing contraction on both sides of the Atlantic is feeding into a structural decline in diesel consumption. Vandana is mildly bearish in the near term, expecting Brent to edge closer to $80-81, and is neutral for late-July and H1/August.

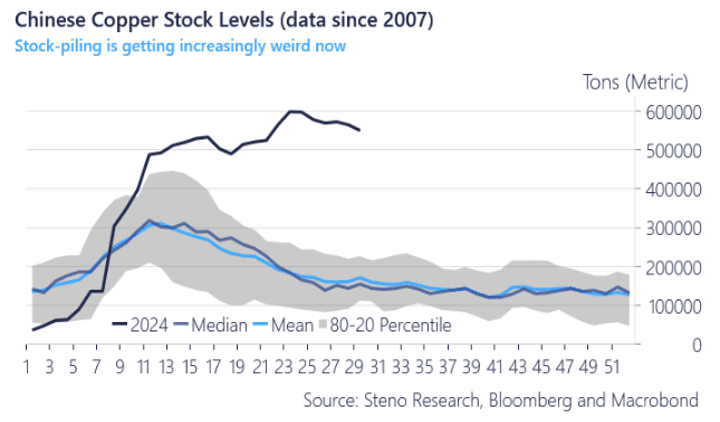

Steno Research

Copper: More pain to come

The copper outlook is cloudy and grey with supply looking to flood markets. Forward-looking indicators appear strong, but in the short term, fundamentals can’t cope with supply floating westwards from China. While the manufacturing cycle shows signs of improvement, domestic copper consumption in China has likely plummeted (down 30% according to Steno’s metrics). The lack of concrete stimulus measures from the CCP Plenum, aside from some vague guidance on the use of funds from the recently issued ultra-long Treasury bond, is another letdown for the real estate sector. China remains inundated with refined copper, which suggests that this surplus will now head westward. As a result, the improving cyclical dynamics in Western economies are likely to be overshadowed by an influx of import supplies in the coming months.

Astris Advisory Commodities

Base sell-off overdone and iron ore to break soon

China’s Plenum gave little hope for a near-term boost to the economy. Ian Roper points out that with stimulus hopes fading and weakness in construction activity continuing, steel prices are now trading at multi-year lows. He says that it now seems only a matter of time before iron ore finally breaks below $100/t, a level from which it has bounced six times in the last two years, given rising supply pressures amid abundant seaborne supply growth and the notable rise in port inventories. Base metal prices have seen sharper declines in the past couple of weeks as prices are once again being driven by more pessimistic global macro sentiment and a stronger US dollar, much as they did through most of 2023. However, the sell-off is beginning to look overdone, with aluminium and nickel both nearing cost support.