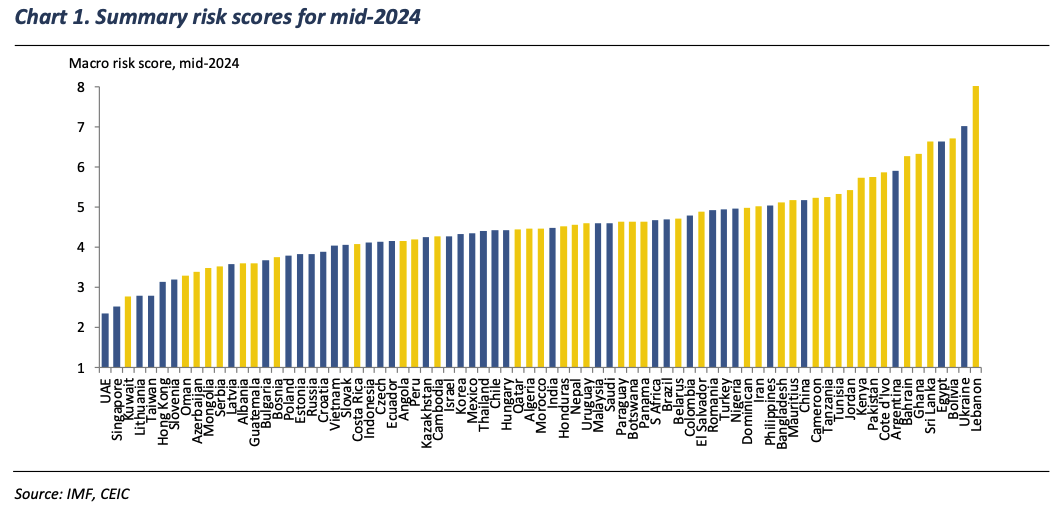

Frontier EM risk

Jonathan Anderson’s latest report examines the safest and the riskiest frontier EM economies. Frontier EM nations lead the way in riskiness, with debt ratios frequently exceeding 100% and current accounts often in deficit. The safest frontier markets come in the form of Kuwait, Oman, Azerbaijan, Mongolia and Serbia. They tend to score well on external risks, all have low public debt ratios bar one, are all running outright budget surpluses and all but one are coal exporters benefiting from the commodity rally. Scores on the financial front are more mixed, but none of their banking systems have significant external liabilities and most are net external creditors. Riskier countries include Lebanon, Bolivia, Ghana, Sri Lanka and Bahrain - riddled with high public and external indebtedness, wide fiscal deficits, banking systems dependent on foreign funding and low FX reserve coverage.

China: Fiscal stimulus is bigger than you think

Report by

Enodo Economics

Investor consensus expects around Rmb2trn of fiscal stimulus to be announced at the upcoming National People’s Congress (NPC) meeting. However, Diana Choyleva’s analysis suggests a much larger figure of Rmb4trn to Rmb12trn, potentially providing a positive surprise that could fuel another leg up in the equity market. Several key factors point to a more substantial package: Finance Minister Lan suggesting the largest debt measure relief in recent years, suggesting a local govt debt swap of at least Rmb2trn; reports indicate that China may raise an additional Rmb6trn from special treasury bonds over three years; the NPC meeting could announce new special purpose bond coverage to cover Q1/2025. Yet, when it comes to the overall size, Diana believes that the stimulus goes at least two-thirds of the way to what China actually needs.

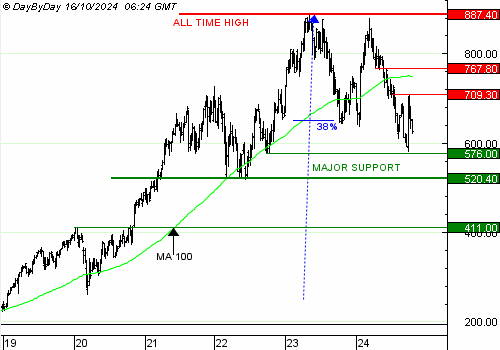

Hang Seng Index: Major base formation

The HSI has surged to the top end of a 22-month base. Resistance at 21,000+ has been a barrier for 32-months. The 3% weekly close breakout above at the top of the base would be signaled by a weekly close above 23,380, with the measured move target at 35,300. Chris Roberts believes that a major base formation is occurring, which opens up the possibility for the measured move target to be significantly exceeded. A buy alert signal may be issued soon.

Indonesia: Calming the nationalist

According to Bob Herrera-Lim, several members of President Joko Widodo’s cabinet are likely to stay on in the administration of President-elect Prabowo Subianto. The most notable of the prospective appointees is Finance Minister Sri Mulyani Indrawati. No official announcements have yet been made, but Prabowo has met with dozens of cabinet officials, allies and party representatives over the past few days, providing an indication of those who have likely been offered jobs in the next government. Prabowo’s willingness to reappoint Indrawati will also be taken to suggest that the president-elect has mellowed into a more pragmatic politician and no longer represents the fire-breathing nationalist and populist of previous election cycles. However, this risk cannot be fully written off for the next couple of years, although for now these concerns will be sidelined.

MENA: The big payback

For nearly twenty years, Israeli Prime Minister Benjamin Netanyahu has warned about the perils the Iranian nuclear program poses to the Jewish people in particular and to the world in general. In the coming months, he may finally have an opportunity to destroy the program, leveraging the momentum of Israel’s recent successes to achieve his life’s goal. Despite serious logistical obstacles, Niall Ferguson thinks Israel could manage a conventional strike, the odds of which are elevated (40% probability by year-end). However, he anticipates that an attack on the nuclear program would come at the end of an escalation cycle rather than at the beginning of one.