Company & Sector Research

Europe

Revelare Partners

Investor Idea Event highlights several exciting opportunities

Revelare hosted a Buyside Event in London where long theses were shared for the following companies: DSV based on an acquisition of Schenker; BFF Bank on an upcoming regulatory approval from The Bank of Italy; Adyen beating consensus estimates; DO & CO lapping capex investments and seasonality; Carvana transitioning to a growth stock with potential for 500% upside; and FTAI Aviation stock doubling from growth and execution. A short thesis was also presented for Edenred which focused on accounting issues and tech disintermediation. Please contact us if you would like to discuss any of these ideas in more detail.

Alumbra Research

Another successful short idea from Alumbra - VTY’s share price is down c.50% from its Jul 24 peak after management announced additional charges for cost overruns on 8th Nov following the company’s initial profit warning on 8th Oct. In Alumbra’s May report, they raised concern that a significant increase in VTY’s unbilled project receivables and WIP was likely indicative of significant cost overruns on ongoing development projects that would negatively impact margins in upcoming periods. In their 24th Oct report, they cautioned that based on the size of the increases in VTY’s unbilled receivables and WIP in 1H24, the company may still have to recognise significant additional charges for cost overruns in upcoming periods.

Forensic Alpha

While operationally the company is encumbered with a number of issues, the balance sheet is still seen as reasonably robust and a source of strength. Nevertheless, there are some signs of increasing concern. A key issue for VW is that the balance sheet of the finance division may need to continue expanding to absorb excess production. Unless capacity can be cut rapidly, this means the group may be running through cash faster than implied by the cash flow of the automotive segment alone. While VW needs to reduce costs urgently, in practice this is likely to be drawn out over several quarters. In the meantime, concerns around cash flow and the balance sheet are likely to intensify.

ResearchGreece

PPA reported strong 3Q24 results, prompting ResearchGreece to upgrade their earnings estimates for the second time in the last 30 days. The shares trade 6.6x EPS (ex-cash) and 4.3x EBITDA 2025E, with FCFE and dividend yield at 8% and 6%, respectively. TP increased to €48 (60% upside). If you think such a valuation is demanding, then consider the implied market cap of €1.2bn puts the shares on 6.5x EBITDA 2027, on ResearchGreece’s mid-single EBITDA growth estimates. If the shares stay at current levels, they will trade 3.3x EBITDA 2027E, with net cash at 38% of market cap.

Kolytics

REITs are not just a Rates play

On the back of recent rise in bond yields, REIT market performance has fallen off a cliff in the past two months in Europe. The Trump win has only exacerbated this trend. However, underlying operating metrics have stabilised and look poised to improve into 2025...the three main drivers of total returns are attractive: 1) current AFFO yield; 2) growth momentum building; 3) and contracting multiples set to reverse should all lead to a sharp re-rating in pockets of the market. Kolytics’ bottom up quantitative approach identifies these opportunities.

Woozle Research

Slowing sales - Woozle’s latest channel checks reveal a weaker than expected Q/Q performance, particularly in North America. Resellers highlighted tighter budgets for SMBs, leading to extended deal cycles and deal spillage into 1Q25. Stronger performance in Europe, especially the UK, provided a partial offset. SGE implemented a 6% price increase on Intacct as of 1st Oct, significantly lower than prior years. Larger deal sizes were noted as the company moves upmarket, though deep discounts up to 30% were often required to secure deals. Woozle’s Q4 revenue estimate is +9.5% Y/Y.

Messels

FTSE 100 Technical Review

Messels' weekly Stocks & Sectors report highlights continued improvement in Services, Media and Banks, while reducing exposure to Consumer sectors. New Buys include Ashtead (broken out of 2-year price and relative ranges) and Barclays (renews the uptrend and has broken out of 8-year price and relative ranges). They have also closed longs in Whitbread (lacks momentum in the short term), Imperial Brands (maintains the uptrend but is reaching the top of the relative range), Howden Joinery (lost momentum and developed short term price and relative tops) and Marks & Spencer (reaching medium term price and relative resistance). Following these changes, Messels’ FTSE 100 Momentum portfolio now consists of 16 stocks.

North America

Trivariate Research

Do you worry about stocks at 50x earnings?

According to Trivariate's analysis, companies that reach 50x price-to-forward earnings for the first time in 3 years consistently see their multiples begin to contract on average back to 37x earnings 12 months after the initial “eclipse”. Although the data suggests that there is no need to panic sell, it does appear that beginning 6-to 9-months later, the odds of outperformance start to deteriorate. Unless earnings explode to the upside, Trivariate’s advice would be to trim these positions 6 months after the initial eclipse of 50x earnings occurs. Recent examples of companies joining the “50x” club include Costco, Carvana, Albermarle and Iron Mountain.

Periphery Research Partners

The underlying assumption between DKNG’s guidance releases for 2024 and 2025 are the same - that it can achieve EBITDA flow-through at a rate exceeding its highest level of gross profit flow-through in its reported history. However, the only way to get there is declining customer acquisition costs and / or reducing promotional intensity, and management effectively walked that assumption back on each of its 2024 EBITDA guidance cuts. Why would this suddenly change in 2025? DKNG’s fundamental story is so structurally broken that Hesham Shaaban may just leave his short on indefinitely.

Gordon Haskett Research Advisors

Chuck Grom expects to see FIVE return to its roots with a heighted focus on offering trend-right products at a compelling value in a fun store experience that the company has deviated from post-Covid. The Five Beyond strategy may get completely shut down. Meanwhile, GHRA’s proprietary data checks show trends seem to have bottomed and are even showing signs of some modest improvement. While the shortened holiday season, uncertainty around tariffs and overall consumer malaise remain high-level concerns, Chuck believes the risk / reward is favourable and upgrades the stock to Buy, setting a TP of $120, which implies ~40% upside from current levels.

The Retail Tracker

The company is moving forward with an energy and confidence that has not been seen in a very long time, according to analysts at The Retail Tracker. Despite a lacklustre share price performance YTD, the Gap brand has been showing improvements, while recent collaborations have also impressed. Old Navy looks great. It had a very good BTS and its relaunch of denim with a powerful message was excellent. The ramp up in marketing will only help. Meanwhile, Banana, which had pushed pricing and design too far, seems to be settling back. Although Athleta continues to lag, the stores are cleaner and when they drop a new line, or colour, it is selling. They expect the stock to move higher over the next few months as GAP continues to gain momentum.

Behind the Numbers

KO’s guidance looks like a stealth cut - coming into the year, the group guided to $2.80-$2.82 EPS for 2024, up 4%-5% from $2.69 in 2023. So far, KO has beaten forecasts by 2 cents, 3 cents and 2 cents YTD, but guidance is only up to $2.82-$2.85. BTN believes investors should be concerned about the following items: 1) A wide spread in pricing between what KO is taking in Latin America and North America vs. PepsiCo, who has seen pricing growth become much more muted. 2) The tax issues on transfer pricing are getting worse. 3) At the same time KO just paid $6.0bn to the IRS, payables and accrued expenses keep rising and BTN cannot find much explanation for it.

Fighting Financials

Following the US election, the team at Fighting Financials continue to like the shares of MS on a 6-to-12-month view. Whilst consensus expectations into 4Q24 are reasonably high, the team think FY25 expectations are overly pessimistic. Indeed, consensus has not yet modelled the impact of Trump tax cuts or the indirect uptick in deal and trading activity resulting from the new administration’s deregulatory tilt. On FFL estimates, the shares yield 5.2% on FY24e dividends and buybacks. Such distributions should provide some near-term support for the shares into year end. Other catalysts include continued headlines on Trump’s new team and broader US equity market beta.

Bios Research

Aaron Fletcher made his second appearance at our Best Equity Short Ideas Conference, pitching SPRY as Bios’ short idea (his previous recommendation was CureVac which generated significant alpha). While SPRY's share price is up more than 200% over the last year as the company prepares for the commercial launch of its nasal spray alternative to compete with EpiPen, Aaron flagged several areas of concern ranging from competition, pricing, TAM, insurance issues and product effectiveness. Click here to listen.

Northcoast Research

The share price of AXON shot up nearly 30% following the release of Q3 results where revenue grew 32% and adjusted EBITDA margins hit recent record highs. The company has experienced sustained growth that few businesses could ever replicate and investor’s confidence is growing in AXON's ability to profitably invest in its future as well as the line of sight for sustained growth for the next three to four years with DraftOne, AI Era, Dedrone, Fusus as well as the market expansion opportunities with legacy products. While logic suggests there could be a pullback over the next few months, Northcoast maintains their Buy rating as they believe the shares will be even higher a year from now. Looking out to 2025 and 2026, consensus numbers remain too low and by a good margin.

ERA Research

Lumber prices are already showing signs of improvement and as interest rate cuts continue into 2025, ERA anticipates that ramping demand and constrained supply will drive prices meaningfully higher. On supply constraints, potential Trump tariffs on US lumber imports from Canada and Europe could limit supply in the US, leaving the US South as the sole source of growth next year. Prior sawmill closures and lingering labour challenges will be headwinds as the south looks to ramp up output. IFP is relatively well positioned compared to its Canadian lumber peers in terms of softwood lumber duty exposure (same goes for any additional US tariffs). Meanwhile, stronger FCF generation in 2025 will allow IFP to address investor concerns re. net debt. TP $30 (55% upside).

Verbatim Advisory Group

Overall trends for 1Q25 are weaker Y/Y, according to Verbatim’s latest channel survey. The majority of respondents reported that they are not meeting their internal goals, while their sales activity for PANW is also below their expectations. Price sensitivity, delayed projects, negative market environment, and competition from Fortinet and Cisco are the major headwinds for the current period. The average sales cycle is either the same or slightly longer (ranges between 4-18 months). Deal sizes are mostly either flat or up Y/Y. A North American system integrator also mentions that new product launches are having no impact on overall sales.

Australia

Influidence

This equipment maintenance company exemplifies exceptional management execution with a ROIC consistently exceeding 20%. Established in Australia’s mining sector - where it engages ~70% of sites - the company is now targeting substantial growth in North America (only ~3% of the sites in the US). With Trump’s election, anticipated regulatory support for domestic resource development could boost the group’s US expansion. MAD’s employee-centric culture empowers local managers to act on direct insights from operations, ensuring agile responses to market needs. The company is also diversifying into energy, rail and infrastructure, in order to continue capturing growth in its home market.

Emerging Markets

Smart Insider

China insider trading trends

There was a dramatic shift in China insider sentiment in Oct, likely in response to the sharp increase in stock prices from late Sep to early Oct. Last month saw 85 insider purchases, down -57% MoM, while insider selling was up +9% to 194 sales. As a result, the Sell/Buy Ratio deteriorated to 2.28. Insider sentiment in China is now neutral having been bullish since Jan 24. Smart Insider upgraded 4+ stocks and downgraded 2-, ending with 24+ ranked stocks and 9- ranks. Stock of the month was Seres Group, where 4 executives bought a total of US$3.1m of stock at CNY92. In each case they had either not made a previous purchase or if they had it was significantly smaller size than this latest buy.

Blue Lotus Research Institute

Blue Lotus expects Kuaishou to report Q3 operating profit and net income above consensus (+5.9% and +7.0%, respectively) with revenue in line. The quarter has been marked by robust advertising (+21% Y/Y, driven by enriched content offerings such as summer Olympics, budget recovery from game and tourism advertisers, and improved ads matching capabilities from GAI), but moderated GMV growth due to weak consumption, leading to a decline in basket size. However, solid traffic growth has laid the basis for faster growth ahead. A reduction in e-commerce subsidies will also boost margins. Trading at 12x 2025 PE, Blue Lotus maintains their Buy rating and TP of HK$75 (50% upside).

Galliano's Financials Research

BBNI is Victor Galliano’s top pick among the Indonesian banks, based on its compelling value and growth credentials. It has the lowest PEG ratio of the big four, undemanding prospective PE multiples and the best PBV ratio to ROE combination. Return trends continue to improve; pre-provision returns have risen after bottoming out in 3Q23, which combine with declining cost of risk to drive better post-provision returns. In addition, the bank’s efficiency ratios have begun to improve. With its CET1 ratio of 19%, BBNI has bridged the gap with Mandiri on capital adequacy and on credit quality it also has the second highest NPL coverage of its peer group, after Permata.

CHA-AM Advisors

India: Real Estate Bubble

David Scott thinks this is the 2009 moment for the Indian house builders. Yes, it is that bad. The BSE Realty Index’s ROE barely beats the Indian 10-year government bond yield of 700bps, even with high leverage. These companies are not making their Economic Cost Of Capital which is why they need to issue so many new shares. And why not? Look at the valuations. The EV To Sales - the value of the firms in this index relative to one-year sales - is now at 15x which is at a record high. David suspects no real estate sector has ever been as aggressively capitalised as this one. The Chinese names never traded on anything like these multiples! As Indian real estate resumes its disinflationary boom, David expects some big earnings disappointments in the next year. Stocks highlighted include DLF, Godrej Properties and Macrotech Developers.

Macro Research

Developed Markets

Radio Free Mobile

AI: At the edge

Now that LLMs are starting to show the limits of their performance, as Richard Windsor has long predicted, attention is starting to turn to use cases of running inference at the edge of the network as opposed to in the cloud. There are multiple reasons why it’ll come out on top, but economics is the main driver – companies won’t have to pay for all of the cost of running cloud services. The Edge AI Ecosystem is currently in the early stages of being built, which is the offering that chipset providers will make to developers in terms of making it easy to run their models on hardware. At the moment, Qualcomm is leading but others are chasing. Richard continues to own the stock and exposure to the nuclear fuel industry as the best long-term way to play the AI theme without being forced to pay for bubble-like prices.

Topdown Charts

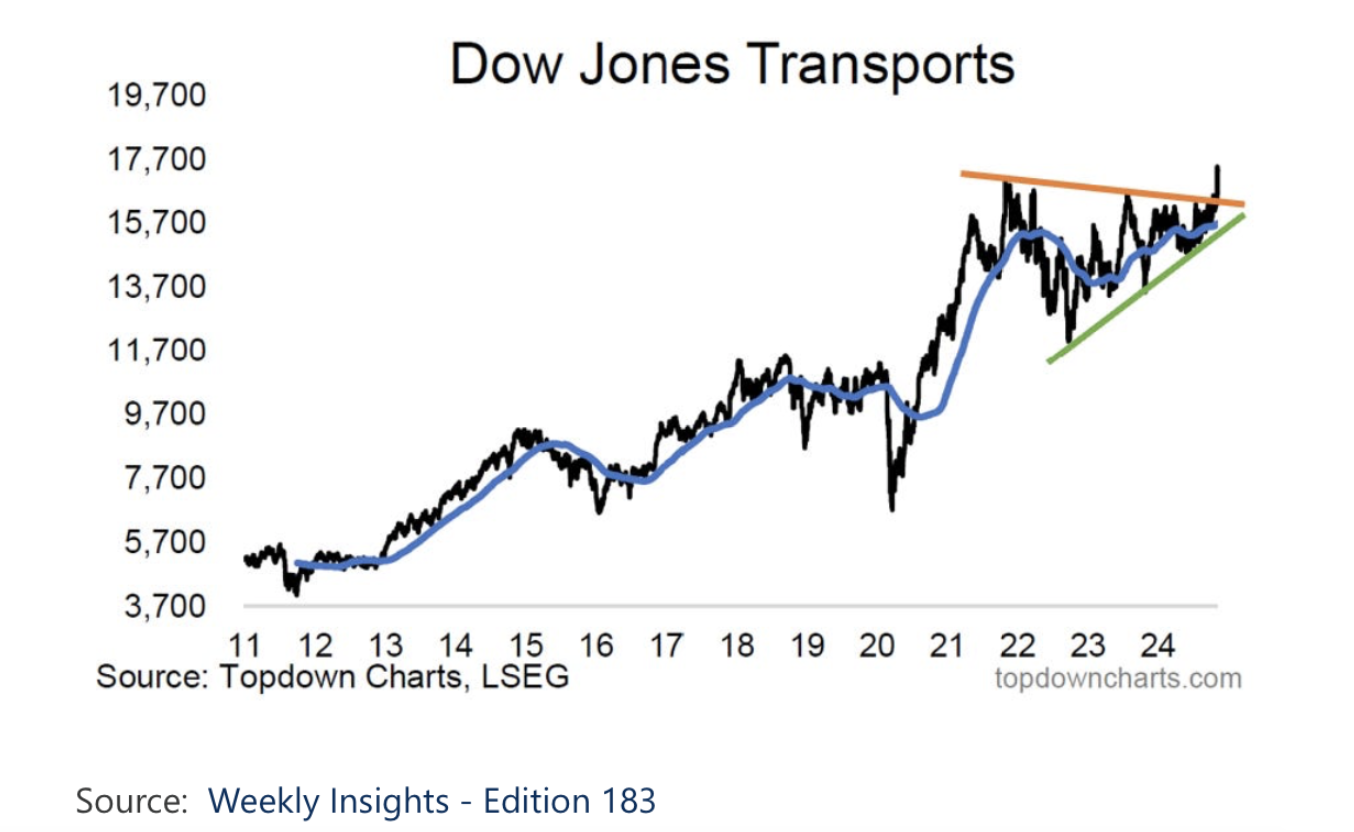

It’s time for risk-on

The mood is well and truly risk-on, claims Callum Thomas. Part of this is a reversal or unwinding of the de-risking and caution in late October, an element of “stealth corrections” resolving to the upside, optimism for a repeat of 2016-17 run in stocks, and a generalised continuation of the underlying market mood of bullish euphoria. Other indicators of the developing risk-on theme are present, including transports making an initial breakout of a huge triangle formation against the backdrop of an underlying overarching uptrend through the period (see chart). However, there are a few key conditions that are quite different now vs 2016 and Callum advises investors to rethink how to navigate things in the coming years…

Lazarus Economics

UK: Forecasts for 2025

Darren Winder points out that the projections in the Autumn Budget 2024 put real GDP growth at a little over 1.0% in 2024 and 2% in 2025. This is around 0.25 percentage points higher than forecast in the Spring Budget. Taken together, the measures announced in the Autumn Budget are expected to boost demand by around 0.5% in 2025 and help lift overall real GDP growth to 2.0%. As these effects fade, growth is projected to slow to 1.75% in 2026 and 1.5% in 2027, settling at around 1.5% thereafter. Darren notes that on the MPC’s latest projections, maintaining the bank rate at 4.75% would result in real GDP growth of around 1.0% in 2025 and 0.75% in 2026. Assuming that energy prices remain close to current levels, his estimates show CPI inflation averaging around 2.25% in 2025.

WaveTrack International

US & European stock indices

There’s a new dynamic which the stock market hasn’t quite understood yet as the Trump-trade has created a FOMO surge amongst investors. That dynamic is inflation and interest rates. The US10yr yield completed a zig zag downswing from last year’s peak into September’s low and is on its way higher again. The weight of rising interest rates may be too much for the current advance in maintaining current upside momentum. Furthermore, the entire recent advance in the major US indices is approaching the upside completion of double zig zag patterns. Most of the pattern is complete with only marginal space for stretching higher ahead of multi-month declines. The small-cap Russell 2000 has hit tops today, meaning that the large-caps aren’t too far behind. Europe’s indices have been declining since the US election although some short-term rallies are expected.

DayByDay

US: Stagflation risk increasing

The US Dollar appreciation since early October matched a rapid widening of short-dated yields between Germany and the US. 2-year yields gained almost 90 bps in the US, but less than 30 bps in Germany, where it really is a matter of when you measure the variation, as yields have been mostly stable. At the same time, and despite the Chinese stimulus, industrial metals fell heavily. Valerie Gastaldy says this is not pointing at a recovery scenario anywhere, but rather an increased probability of a stagflation trajectory in the US. Valerie asks: has the market priced the worst of that stagflation risk? Maybe not. The short-term trends may take a breather for a few days, but medium-term trends are not at key levels not particularly stretched.

WilmotML

US: Powell plays it straight

According to Jonathan Wilmot, markets will take their cue from how growth, inflation, corporate profits, bond yields, Fed policy and geopolitical risks might change under a Trump administration. Market participants are now frantically looking for clues from his cabinet choices as well as trying to gauge how the Fed might respond. On that score, Chairman Powell played with a straight bat last Thursday: the FOMC cut rates, so policy is still restrictive and may become more so if bond yields keep rising. (And he’s staying in the job). Jonathan’s weekly update on underlying US GDP growth confirms that growth is already peaking, while his Taylor Rule variants suggest that policy probably is restrictive (don’t forget the “extend and pretend” problem in commercial real estate). Trump needs the bond market to stay on side, but will it?

Westbourne Research

US: Trump triumphs

Sharmila Whelan reckons that Trump 2.0 will be better than Trump 1.0 and is a positive for the US economy, corporate earnings growth and equity markets. She believes that many in the markets are making the wrong assumptions. Take tariffs for example, which the administration has indicated it will use as leverage rather than old school protectionism. Among the changes will be more favourable treatment of the AI and cryptocurrency sectors, and Sharmila predicts that Bitcoin will become part of the Fed’s official reserve assets before the mid-term elections or by the end of Trump’s term. BUY Bitcoin and US equities – banks and energy companies. Consider SHORTing European stocks.

Pennock Idea Hub

How to trade the Trump euphoria rally

Cam Hui expects the US stock market to rally into January, driven by corporate tax cut expectations, FOMO performance chasing and buybacks as the post-earnings season window re-opens. Weakness in the performance of defensive sectors is another signal that the surge in stock prices may have further to run. Tactically, the S&P500 is currently testing the top of a rising trend line, so don’t be surprised if it cools off in the next few days. That doesn’t mean a significant decline is underway, Cam expects further gains once the pullback is complete – sentiment readings are not bullish, allowing more room for upside. Just before inauguration day, expect the mood to change as the unknowns of the Trump Administration’s initiatives become better defined.

Emerging Markets

Emerging Advisors Group

The South-South trade

The share of South-South trade has risen steadily over the past two decades, now exceeding 50% of total trade turnover in the EM universe. However, Jonathan Anderson points out that this is all due to China. If the country is excluded, the internal share of trade between the rest of EM has actually fallen. Jonathan claims that China is a coloniser, not a leader. It likes to portray itself as a partner for mutual growth, but the opposite is true. Its relationship with the rest of EM is marked by a rapidly increasing surplus within the South and an overwhelming level of purchases for raw materials while selling higher volumes of industrial products – effectively using the South as a “vent for surplus”.

CrossBorder Capital

The debt concern

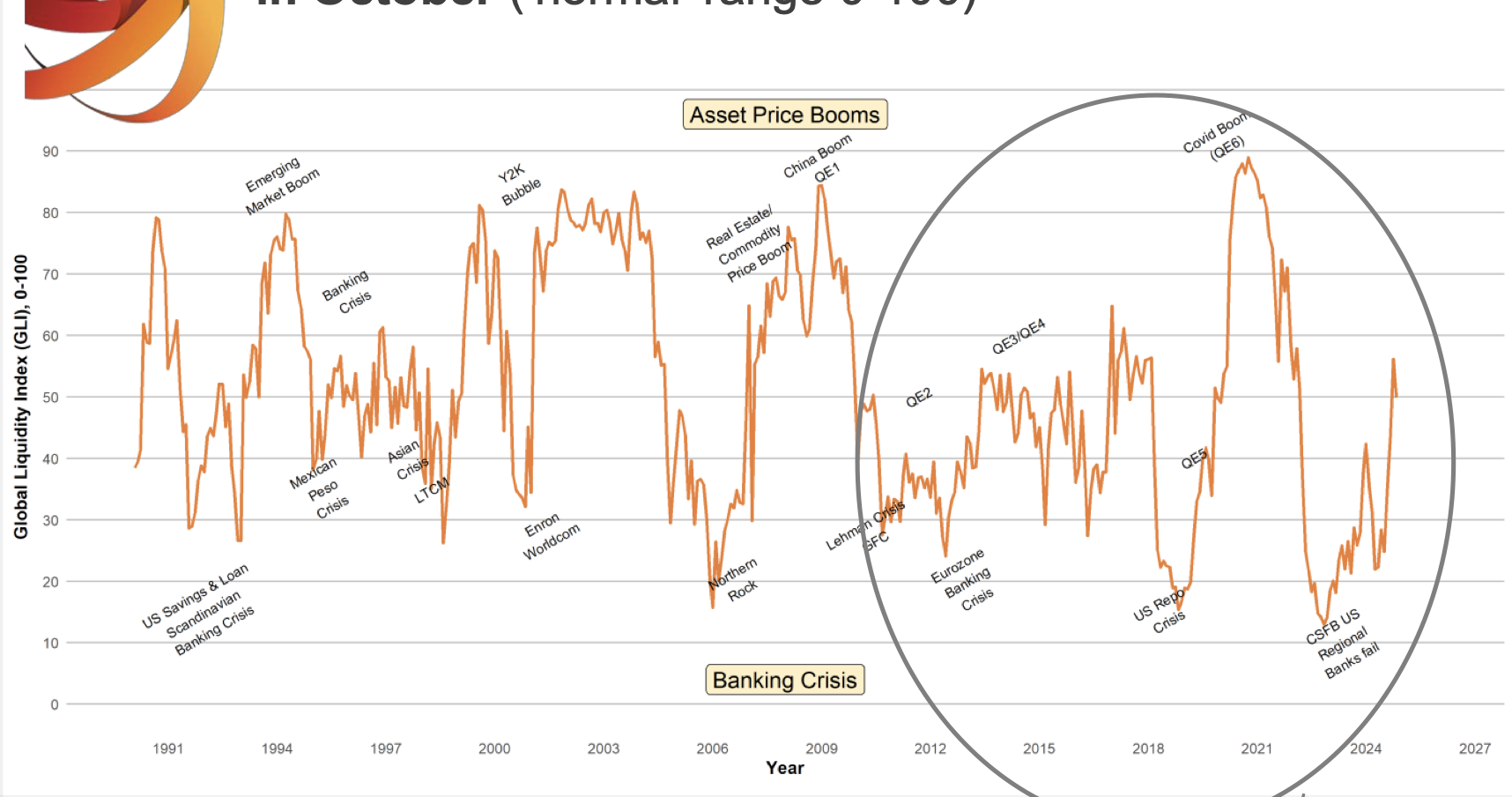

Global Liquidity posted a GLI™ index reading of 49.9 at end-October 2024, paced by strength in World Central Bank Liquidity (index 65.3) and private sector cash flows (43.5). October proved to be a small dip from Michael Howell’s significantly upgraded September estimates, which benefited from the national holiday-delayed release of key Chinese data. He examines China in depth in his latest report, but the bottom-line for both China and other economies is that World debt continues to rise, and more debt ultimately demands more liquidity. Despite their outward rhetoric of ‘QT’ and tightening, policymakers have been secretly easing via, what Michael calls, ‘not-QE, QE’ and ‘not-YCC, YCC’. But this is done at the cost of stoking ‘hidden’ inflation. He also mentions that given the challenges in 2025, risk markets seem ahead of themselves. The euphoria may last for longer, but bear markets appear out of blue skies.

Topdown Charts

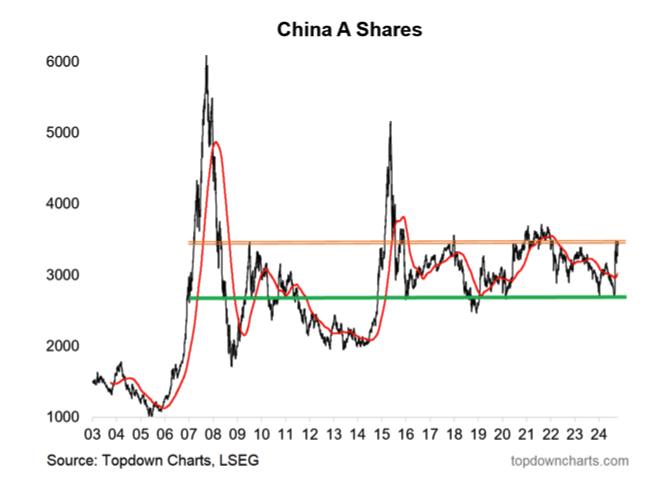

China: The obvious loser?

Conventional wisdom says one “obvious loser” (i.e. China A-Shares) will suffer the second coming of Trump. Callum Thomas says that there’s obviously some truth to this as the country deals with its worst property downturn on record, local government debt, soft employment growth and more… However, this typically would be dog whistle to a traditional central banker to start full blast into monetary easing. More stimulus may also be underway in response to a new trade war. That’s the kind of thing that would drive follow-through in what may well be the start of a new and significant bull market in Chinese stocks. On the technicals, Callum has seen a sharp rally off a key-long term support level. Importantly, the surge has stuck. Should it go-on to clear that major overhead resistance zone there’s no telling how far it will go.

Greenmantle

Mexico’s political regime change

A month into her presidency, Mexico’s Claudia Sheinbaum is struggling to contain the fallout from her predecessor’s judicial reform. With its supermajority in Congress, her party Morena is keen to advance former President Andres Manuel López Obrador’s agenda, no matter the cost. Meanwhile, the economy has proved surprisingly resilient in 3Q24, but the ongoing constitutional crisis at home and Donald Trump’s re-election to the US presidency will increase the doubts about the coming years for Mexico. Local sources seem optimistic that energy reform will end profligate spending by the state oil company Pemex, with its bonds rising in value ahead of a possible rating improvement. Niall Ferguson expects MXN to depreciate further in the coming year, with lower domestic rates, and is SHORT MXN/USD.

Krutham (formerly known as Intellidex)

South Africa: Inside the ANC

The status of the relationship between the ANC in Gauteng and the national ANC has become an important sovereign risk determinant since the party’s failure to strike a coalition deal. In his latest note, Peter Montalto tackles some of the questions concerning this relationship. The Gauteng leadership of the ANC has demonstrated reservations about working with the DA. Personal tensions and leadership ambitions have fuelled speculation of disharmony and some leaders have become reluctant to confront the DA as it now has a big say on who becomes president of the country. Overall, Peter remains relatively sanguine that the Gauteng situation will not derail the National or KZN coalitions for now. However, as internal leadership succession issues in the ANC accelerate towards 2027, noise will certainly rise further still, but also real risk. The baseline expectation that the GNU will last five years remains unchanged.

Macro-Advisory

Tajikistan: The awakening of a forgotten country

After decades of being of little interest to all but adventurous geologists, Tajikistan is now a country of great interest because of an abundance of critical minerals (CRAM) and its potential to be a major supplier of electricity to Central Asia. In his latest 50-page report, Christopher Weafer dives deep into the country. There are some concerns, including security and domestic stability. Yet, positive signs are emerging, with both Moody’s and S&P upgrading their risk assessment based on the more promising growth and investment prospects as well as low debt. Additional opportunities are beginning to appear in consumer sector investors, for healthcare, transport and logistics, and elements of a digital economy—all of which are poorly developed today.

ESG

Sustainable Market Strategies

The green agenda hits a red wall

The re-election of Trump marks a significant shift for sustainability-focused investors. Anticipated regime changes include higher bond yields and resurging inflation, and some changes to the fiscal tailwinds coming from the soon-to-be defunct Inflation Reduction Act. The fundamentals tied to the energy transition remain unchanged: demand for power is growing fast, and clean energy is cheaper and quicker to build than fossil fuel power plants. The recent devaluation of green equities creates opportunities for savvy investors and the Sustainable Market Strategies team suggest investors take a back seat for now and look for opportunities to acquire undervalued stocks. In the short run, they should look for companies with a limited exposure to the US and who still have strong businesses outside the country. Over the medium term, they could also look into re-entering into renewable companies with a strong business pipeline in the US given the current trends in the country’s power demand.

Commodities

Queen Anne's Gate Capital

US dollar strength is a headwind for metal demand

The US election surprised by delivering a decisive winner. An insurrection has been averted and the macro picture has cleared through year-end. Additional events from the past week - including several central bank policy developments, the German government collapse and the China NPC stimulus damp squib - were steamrolled by the Trump trade: higher DXY, rates and risk assets. If personnel is policy, administration and cabinet appointees signal full MAGA ahead… Lower precious and industrial metals prices are directly related to the US election. The resulting DXY strength is a headwind for metal demand. Further, the medium-term outlook across the metals sector is increasingly uncertain, dependent on the scale and timing of tariffs slapped on China and elsewhere (European autos?), as well as potential reciprocation and the net impact on overall consumption. Easier permitting and regulation for commodity production (beyond merely energy) will bolster metals supply.

Vanda Insights

Implications of Trump 2.0 for oil

Financial markets went into a tizzy this week, trying to price in Donald Trump’s victory in the US election. Crude was infected with some volatility too, but there were a bunch of influencing factors in the mix, making the net impact of the US election result hard to isolate. Big picture: Brent reversed the previous week’s losses, trekked up to the $75 handle and tentatively hovered around it. In the coming weeks and months, Vandana Hari expects Trump’s moves on the international stage - including efforts to end the Gaza and Ukraine wars and potential tightening of oil sanctions against Iran and Venezuela - to have more bearing on oil fundamentals in the short to medium term than upstream or environmental policy changes at home.