Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Geography

Europe

EVO was one of the ideas pitched at Revelare’s recent Investor Idea Event - the presenter's bear thesis focused on both fundamental and regulatory concerns. Growth is slowing, yet the multiple remains in the high teens. ~60% of the company’s revenues are derived from unregulated markets, but there is a movement afoot to regulate EVO and others like it in China and Japan, which is what is impacting growth. Furthermore, the presenter believes evidence exists that EVO has been receiving compensation from aggregators’ transactions to customers associated with illegal activity and that heavy restrictions will be placed on its business soon. 40%+ downside.

CFO Nik Jhangiani will help spur the company’s rebound with his technical skills and ability to drive change. He previously worked at Coca-Cola Europacific Partners, where he streamlined operations, oversaw large acquisitions, and ensured those deals and other investments earned value-creating returns. He also excelled at investor relations, which will be helpful for a company that has underperformed for two years under CEO Debra Crew’s tenure as COO and CEO. Paragon’s analysis includes interviews with former colleagues of Jhangiani. Sources were universally positive. The only reason he will fail, they said, is if others in the DGE organisation actively resist his programmes.

Woozle initiates coverage with a Short recommendation - channel survey respondents reported 4Q24 European revenue declines of -1.5% Y/Y, missing the flat growth market expectation as consumers shifted to competitors like Coca-Cola. Americas revenue grew +3.6% Y/Y, but fell short of the +11% consensus forecast. Market share losses were noted in both regions. Overall sales relied on increased discounting to offset price hikes, reflecting weak demand. Inventory issues and underperforming products like Juices hampered growth, while Indian Tonic Water remained a bright spot in FEVR’s portfolio.

Iron Blue initiates coverage on the stock with a score of 27/60, which is top quartile (fertile grounds for shorting) and their equal highest score in the Capital Goods sector. They highlight 1) Reliance on percentage-of-completion revenue recognition. 2) Sustained stripped out restructuring charges. 3) An ageing debtor book (China construction). 4) Widened gap between capex and depreciation. They also note governance out of line with best practice (elevated non-audit fees, non-independent chair, board & remuneration committee and narrow CEO variable compensation payout metrics) as well as many areas of imperfect disclosure.

Robert Crimes raises his valuation for Vinci Energies by +35% from €14.5bn to an EV of €19.6bn. Two global megatrends continue to support demand in the medium to long-term: the energy transition and digital transformation. Furthermore, the market is still highly fragmented and there is an “endless deal flow” for continued small acquisitions as it continues to roll out its easily scalable business model. The share price underperformance YTD provides an attractive entry point as Robert upgrades the stock to Buy and increases his TP to €175 (75% upside). His long-term model forecasts are available on request.

North America

12x earnings is cheap, but 6x is not

Trivariate studied stocks whose price-to-forward earnings appear to be optically cheap. Their findings reveal that the performance of stocks that dip below 6x earnings is far worse than those dipping to 8x, 10x, or 12x forward earnings. On a beta-adjusted basis, the average stock dipping below 6x earnings lags by more than 900bps over the next 10 months. The stocks that first dip to 8x earnings outperform for a few months, but then on average also lag over the next 24 months. Stocks that dip to 10x earnings perform close to the market over the next nine months. Stocks that dip to 12x earnings perform in line with the market over the next two years and then subsequently modestly outperform.

Following WMT’s latest results, Scott Mushkin doesn’t think so. With market share flowing to WMT and AMZN at a quickening pace, which he sees being aided over the next few years by efficiency gains in distribution and logistics, as well as a growing high margin advertising business, other retailers will be pressured. At the same time, the increasing buying power of both companies could weigh on the margins of suppliers. Considering this backdrop, Scott sees slim pickings for investors owning other retailers, however, he does highlight the natural and organic grocery sector, as one that can grow quickly; he currently has a Buy on Natural Grocers, whose share price has risen 170% YTD.

AirDNA data points to nights pacing in line with consensus estimates, but Robert Mollins thinks the forecast will be downwardly revised once Dec is in the books. Comps will be more challenging this month than in the first two months of Q4 and with AirDNA's forecast methodology assuming QTD Y/Y performance holds for the entire quarter, Robert is comfortable with his room night estimate (107.7m) sitting below AirDNA's forecast (109m). He reiterates his Underperform rating (TP $108); sees risk greater than reward with ABNB trading at a material premium to peers and uncertainty around margins heading into '25E with planned investments from 2H24 expected to persist into next year.

4Q EPS guidance came in well below consensus, reflecting a $0.09 FX headwind and -150bp to -200bp Y/Y gross margin deterioration tied primarily to a heated up promotional environment in the US. Janet Kloppenburg views this outlook as a red flag that brand performance maybe deteriorating since she has not witnessed ramping promotions across the DTC or wholesale channels in 4QTD. Thus, while North American wholesale revenue improved to +LSD in 3Q, she worries that margin trends in the quarter maybe under pressure, particularly in the CK brand. For FY25, she was surprised by management’s outlook for 50bp of gross margin pressure as 20% of the GIII business is brought in house. As a result, Janet has cut her EPS forecast for next year as well.

Trump transition, FDA/RFK risks & Medicare Advantage/Healthcare Services outlook

The Trump transition, Cabinet Nominations and Republican healthcare agenda are front and centre for healthcare services, managed care and pharma / biotech investors. With near-daily headlines from Washington driving sentiment in healthcare equities, Aldis Institutional's policy-focused events provide investors with timely and actionable insights into the DC landscape. This differentiated platform combines small group conversations with key stakeholders and policymakers, with real-time market commentary from Aldis' senior team. Recent and upcoming event topics include the outlook for Medicare Advantage, Hospitals, FDA Changes Under the Trump Administration and near-term catalysts such as FDA compounding policy impact on Hims & Hers Health, Novo Nordisk and Eli Lilly.

MYST highlights bearish views on the stock, with one Buyside client saying they would be astonished if there isn’t a short report out on FTAI in the next year as they do not believe the accounting. FTAI is depreciating the asset on the Leasing balance sheet, transferring it to the Aerospace balance sheet, and selling it and reporting a gain-on-sale. That is ~90% of earnings, it is a farce. All these Aerospace multiples are “nuts”. AerCap is the right comp for FTAI - these types of businesses trade at 10x EBITDA (vs. FTAI at ~19x FY25 Street EV/EBITDA).

Hassan Ahmed argues that the recent uptick in methanol prices is sustainable in the near-to-medium term based on cost curve support, potentially higher oil prices and tightening supply / demand fundamentals. Marginal methanol producers are making razor-thin margins at current prices, suggesting limited (if any) pricing downside. Beyond 2024, Hassan expects limited new methanol capacity builds, with demand growth outstripping supply growth and global utilisation rates tightening. He also anticipates that MEOH’s FCF generation will accelerate post-2024 as a result of the Geismar 3 start-up. Over the next five years, MEOH can cumulatively provide over 65% of its current share price in excess cash flow (excl. the acquisition of OCI's assets). 12-month TP $60 (30% upside).

Retail REITs: #Retail5.0 & the outlook for supply and demand

Key factors explored by Brian McGough include: 1) The 5 Megacycles in Retail and how this affects the supply / demand balance of the Malls, Shopping Centres and Outlets. 2) The next burst in e-comm growth needs to come from same day delivery and what it means for retail landowners. 3) The importance of physical retail space is underappreciated. The best retailers and brands will pay up materially for the right space…what it means for REIT pricing trends. 4) The bankruptcy cycle and where it is headed from here. 5) Could the peak occupancy levels we are seeing in Retail REITs grind higher from here? And what kind of pricing strength could we see if / when demand outstrips supply? 6) Key modelling assumptions behind Hedgeye’s calls for 14 tickers, including Simon Property Group, Macerich and Tanger.

The “ouster” of Pat Gelsinger will almost certainly result in INTC being split up, meaning the once all-powerful brand may soon be just a memory. With the company’s future very uncertain and its once great engineering culture in poor shape, INTC is easy pickings for its resurgent competition. Richard Windsor expects to see Qualcomm, AMD and MediaTek redouble their efforts in PCs and the data centre. He has often said that at 10x earnings, one should shut one’s eyes and buy the stock, but because of the falling EPS estimate the valuation has never gotten there. With the company in this much trouble, there is no price at which he would want to buy it.

Three weeks ago, with SMCI trading at $21, Lynx rolled out a $45 price target and opined that the odds of delisting were not as high as many thought. Their view was based on belief that the company held a uniquely critical position in the all-important business of installing AI infrastructure. They also argued that the likelihood of Dell taking market share was overblown and called for the run-up in the stock to fade. For the next couple of months, the event-driven volatility is likely to wind down while investors turn their focus to SMCI’s fundamentals. And that is reason enough for Lynx to raise their TP to $60 (based on 20x their FY25 EPS estimate of $2.93).

Japan

The company has recently seen its share price rise after a stake build by activist Effissimo. However, with higher semiconductor production globally, increased chip stacking and with the US set to cut out Chinese EV battery materials suppliers under its IRA, it looks like we are at the start of a major run up in earnings. KD has high global shares in certain etching and cleaning gases, and earnings here have already started to jump, but this has been obscured by losses from its battery materials. However, as the US forces more production domestically and KD being one of only two non-Chinese suppliers, those battery losses could reverse sharply. With just two local Japanese brokers covering the stock, the coming earnings surge looks largely unrecognised.

Emerging Markets

While this deal has been well flagged, finally getting it done is positive and bodes well for overall Indonesian ARPU. Valuation of the combined entity is better than it might have been from an XL Axiata perspective. Synergies targeted appear surprisingly large and while the market is likely to be sceptical this means that there is significant potential upside if management can deliver, especially given the relatively low pre-synergy multiple (4.6X EV/EBITDA). New Street has a Buy rating on Indosat (TP IDR 3,125), Telkom Indonesia (IDR 4,500) and XL Axiata (IDR 5,000).

EM Spreads initiates coverage on Argentina’s state-owned oil and gas leader, with an Outperform recommendation. In their view, improving macroeconomic conditions in the country will likely support YPF’s operations. This, combined with management's strategic focus on expanding unconventional, lower-cost production and investing in infrastructure, particularly export capacity, is expected to enhance YPF’s credit profile and drive outperformance in its bonds over the next 9-12 months. They favour the YPFDAR (Caa3/CCC/CCC) 8.500% 2029 unsecured bonds, YPFDAR 9.000% 2029 unsecured bonds and YPFDAR 9.500% 2031 secured bonds. These bonds are trading wide to the overall YPF, LatAm BB, and EM BB curves. Additionally, they offer an attractive yield pickup compared to sovereign debts of similar duration.

High conviction financials for 2025

Bradesco, Hana Financial and Bank of Baroda are Victor Galliano’s top picks amongst the GEM banks due to deep value with positive returns catalysts, while his sell on premium-valued Nubank is due to fundamental return headwinds emerging. In the Japanese banks, Victor identifies Mizuho and Resona as key beneficiaries of higher benchmark rates going forward, alongside very attractive valuations and supported by strategic share portfolios. CME Group is his 2025 pick in global exchanges, as a "flow monster" with a very strong competitive position. PagSeguro is his deep value, contrarian pick in payments.

Macro Research

Developed Markets

It’s risk on

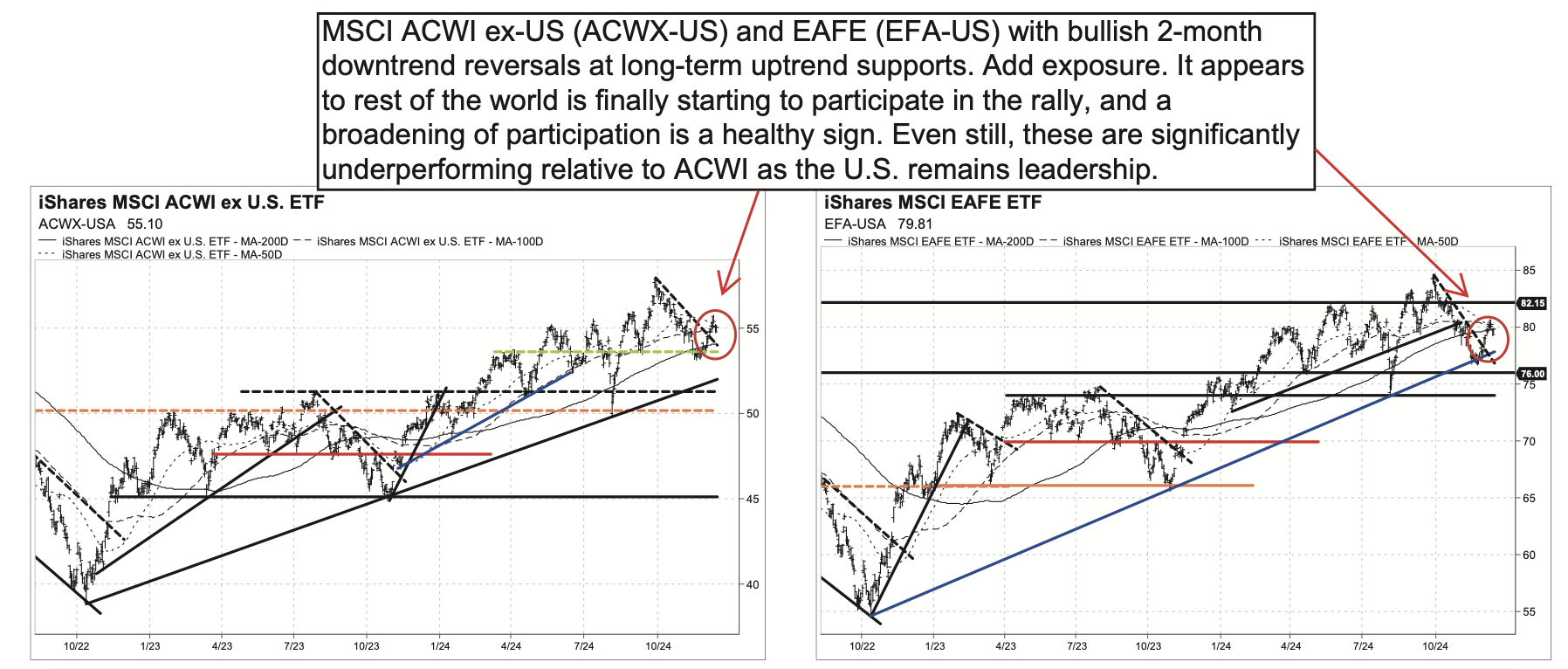

US and European high yield spreads remain at 3+ year narrows. Global sovereign 10-year yields and the US dollar (DXY) remain below critical resistance levels, and have been moving lower recently, as expected. US interest rate volatility (MOVE index) has collapsed following the election. MSCI EAFE and ACWI ex-US display bullish 2-month downtrend reversals. MSCI Emerging Markets (EEM-US) remains above its 200-day MA and the critical $41 level. Mainland China (Shanghai Composite) remains bullish. Global cyclical Sectors are outperforming (Consumer Discretionary, Technology, Financials, and Communication Services) while defensives are underperforming (Consumer Staples and Health Care). The global Discretionary vs. Staples ratio (RXI-US vs. KXI-US) is breaking to all-time highs. All of this strongly points to a risk-on environment (see charts).

Euro: Running behind

For the fourth time in 2024, the ECB cut rates by 25bps. At 3.0%, the deposit facility rate is down 100bps from its peak and approximately half-way down to what many believe to be the neutral rate of ±2.0%. PMIs now suggest that the Eurozone economy may barely grow, so concerns over undershooting inflation have risen. They should, according to Niall Ferguson. However, calls for accelerating the pace of rate cuts are unlikely to gain traction until there is a clearer signal of inflation undershooting and hard data on growth stagnating or even being negative. The ECB could also be prompted to consider a larger than 25bps move if Trump’s trade threats materialise. Nevertheless, Niall’s baseline is that the ECB will cut by 25bps in January and March. In short, they will remain behind the ball. He remains short EURUSD.

US: Welcome to the Hotel California

“This could be heaven or this could be hell” - the US economy (on the face of it) appears relatively strong and likely to remain that way for the foreseeable future. With Trump’s early-November election win with a clean Republican sweep of the House and Senate, the market is betting the goldilocks economy continues, but while the large and growing budget deficit is broadly acknowledged as an issue, it’s getting little more than lip service – this should be concerning because, without a meaningful market protest, there is limited urgency to address the elephant in the room. Kolytics' latest report includes a detailed analysis of Trump’s proposed policies on tariffs, taxes, immigration and deregulation.

Canada: Taking the under on growth and inflation prospects

Danielle DiMartino Booth points out that Canada’s unemployment mix is weakening, and the trend rise in unemployment flags downward revisions to GDP growth are in train. Annual changes in Canadian unemployment and real GDP have a stout -0.92 correlation going back to 2003; notably, Canada’s 1.087% rise in unemployment over the last year to 6.841% suggests real GDP should be running flat, not at its current 1.6% YoY pace. Mortgage delinquencies are already rising, a move that will be amplified as joblessness keeps rising. In addition, the share of Canadian consumers expecting rising real estate values has been cooling since the spring, as has the Teranet House Price Index; both should contribute to further cooling in Canadian Shelter CPI, adding fuel to the fire that supports the BoC’s easing campaign. Long Canadian government bonds, anyone?

Australia: Bond markets need to reprice expectations further

This week’s data didn’t come as a surprise to Craig Ferguson, but it did to bond markets that had rushed to price in a 70% change of an RBA cash rate cut come February. After this week’s data release, expectations have been cut towards 50%. Yet Craig believes that the RBA is unlikely to think about cutting rates anytime soon, and that markets may reduce the 50% probability to zero over time. A May cut could be a slight chance if inflation, jobs and GDP weaken but August looks more likely. As such, as cuts gets priced out, the AUD and AU 10yr yields could find support, although the AUD will also be driven more by USD direction moving higher and AU 10yr yields could be more driven by global yield trajectories moving higher rather than the RBA.

From Tokyo to Seoul

Niall Ferguson’s team spent two weeks in Tokyo and Seoul and spoke with high-level policymakers, diplomats, economists and investors. Both countries are looking to reduce their US trade surpluses ahead of President-elect Donald Trump’s anticipated tariffs, including by purchasing more US LNG and increasing US FDI inflows. Niall is increasingly confident that the Japanese economy’s wage-price growth cycle and the BoJ’s continued policy normalisation will continue into H1/2025. In Seoul, even President Yoon Suk-yeol's own People Power Party wants him to resign. If he does not resign in the coming weeks, he expects the National Assembly to impeach him. Either way, a snap presidential election in H1/2025 is Niall’s base case. He maintains his bearish outlook on South Korea’s export-dependent economy, which is driven primarily by structural factors rather than political risk, though defence makers will likely return as a bright spot in 2025.

Never a dull moment in Korea

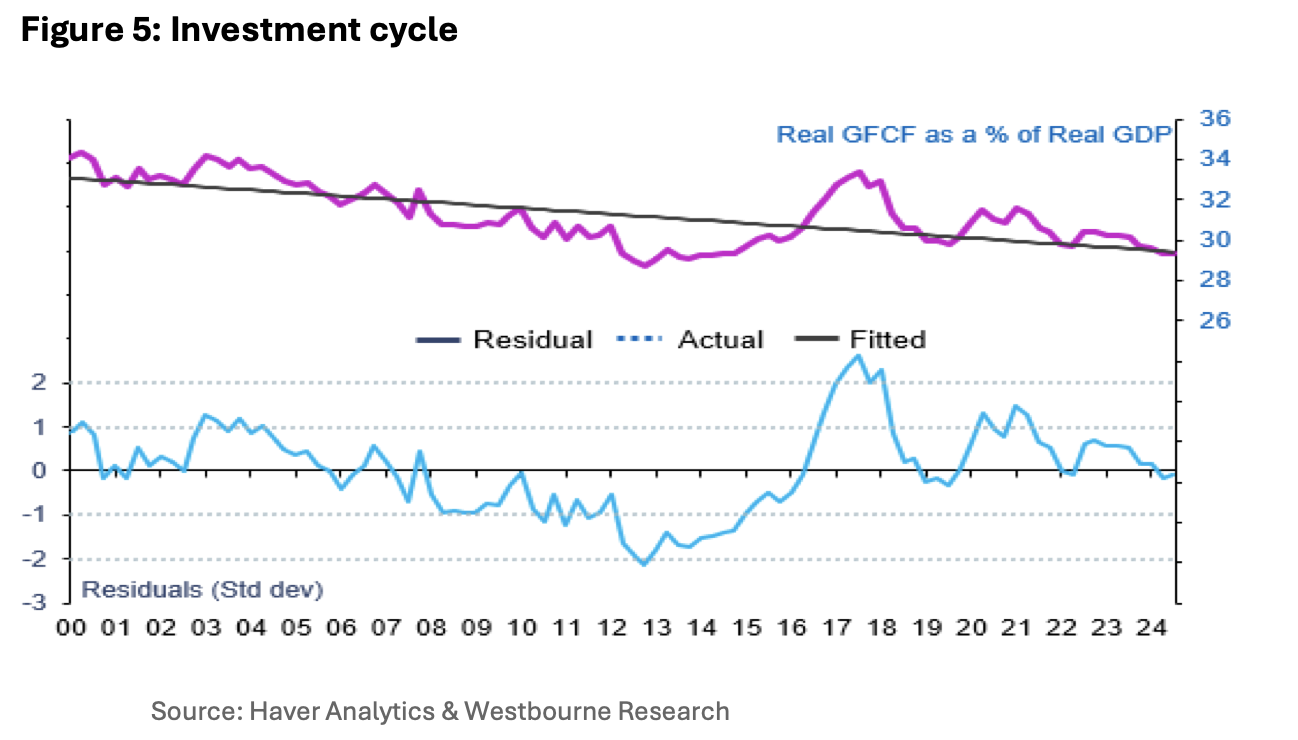

The Korean economy has lost broad-based momentum and the corporate business cycle has turned, which are some of the key reasons why Sharmila Whelan is turning neutral on equities. Expect investment to slow further and the investment cycle to move into downswing (see chart). It’s not all doom and gloom though; the credit upcycle is strengthening again and gives confidence that there is no risk of an outright recession. This also bodes well for consumption spending and related stocks. Despite the ongoing political crisis, government finances remain robust and Sharmila maintains an overweight position in government bonds. When it comes to the won, the fundamentals indicate no reason why it should be under pressure. In reality, it has been weakening against both the USD and on a trade-weighted exchange rate basis since October, and there is an increasing risk of capital flight, so Sharmila advises investors to hedge against weakness.

Global earnings expectations are still high

Global earnings expectations over the next 12 months are still high at +12%. Charles Ekins notes that there are six Global Sectors with expectations of double-digit growth: Technology (+23%), Healthcare (+17%), Communication Services (+16%), Materials (+16%), Industrials (+12) & Consumer Discretionary (+12%). Energy is the Sector with the lowest expectations of growth (+1%). Overall there hasn’t been much change in earnings expectations in recent months, but there been a difference at the Sector level. Over the last 12 weeks, expectations for the level of earnings have fallen 8% for Energy, 5% for Materials, and 4% for Industrials, Consumer Discretionary and Real Estate. At the Regional level, growth expectations for the US are still high (14%), with UK at 5%, Europe at 8%, Japan at 8.8% and Asia generally very strong too. European earnings expectations have fallen the most (-7%) over the last 12 weeks.

Japan: Solid data again

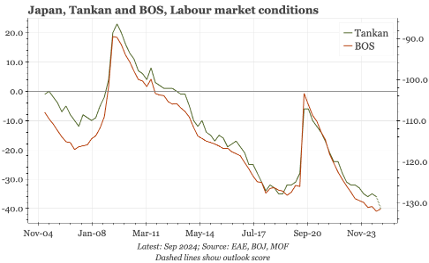

Paul Cavey notes that the latest data releases were constructive: the December Reuters non-manufacturing Tankan recovered from recent weakness with the outlook looking strong; the Q4 business sentiment survey from the MOF was solid, with the labour market tight; and PPI inflation rose again to the highest in more than a year. While manufacturing sentiment remained soft in the Reuters Tankan for December, non-manufacturing sentiment bounced back towards cycle highs, and respondents were even more optimistic about the next 3M. That helps allay concerns, driven by the recent weakening in both the Reuters and PMI surveys, of a real slowing of non-manufacturing activity. In addition, anecdotes in the Reuters survey suggest that the BOJ's hoped-for virtuous price-wage cycle remains intact.

Emerging Markets

China: The shift we’ve been waiting for?

Anyone with a Bloomberg Terminal can see that the Chinese economy stinks, remarks James Aitken. Yet some people have been calling for the big pivot in the economy for two years – is it finally here? The last time Beijing employed the phrase ‘moderately loose’ was in the aftermath of 2009; since then, policy has been described as ‘prudent’. We’re also seeing top officials making direct pledges to stabilise property and stock markets, and they have for the first time promised ‘extraordinary’ counter-cyclical policy adjustment. It appears that leadership is acknowledging the need to do more to underwrite the economy and restore domestic consumer confidence. Yet, James’ opinion remains unchanged. If you want to go long, go for it, but keep in mind the problem isn’t monetary nor fiscal, it’s communism.

China: Long live stimulus theatre!

The Q4 Politburo meeting delivered a significant shift in macro policy, reinforcing confidence in achieving the 5% growth target for 2025. William Hess claims that on this basis alone, the short-term market reaction is justifiable. However, investors should be realistic about the magnitude of stimulus in the pipeline. Consumption stimulus, for example, is a slow-moving variable with a 3-6-month lag. William is also still waiting for further proof of tangible injections into the system to believe it will actually occur. Nevertheless, he is most bullish on equities, claiming that a 1x increase to the forward multiple implies ~8% upside to the CSI300; joined with a 10% improvement to earnings expectations, this would see an ~18% increase. The backdrop is also bullish for government bonds and developer stocks and bonds in the short term.

China: Buy gold… in yuan

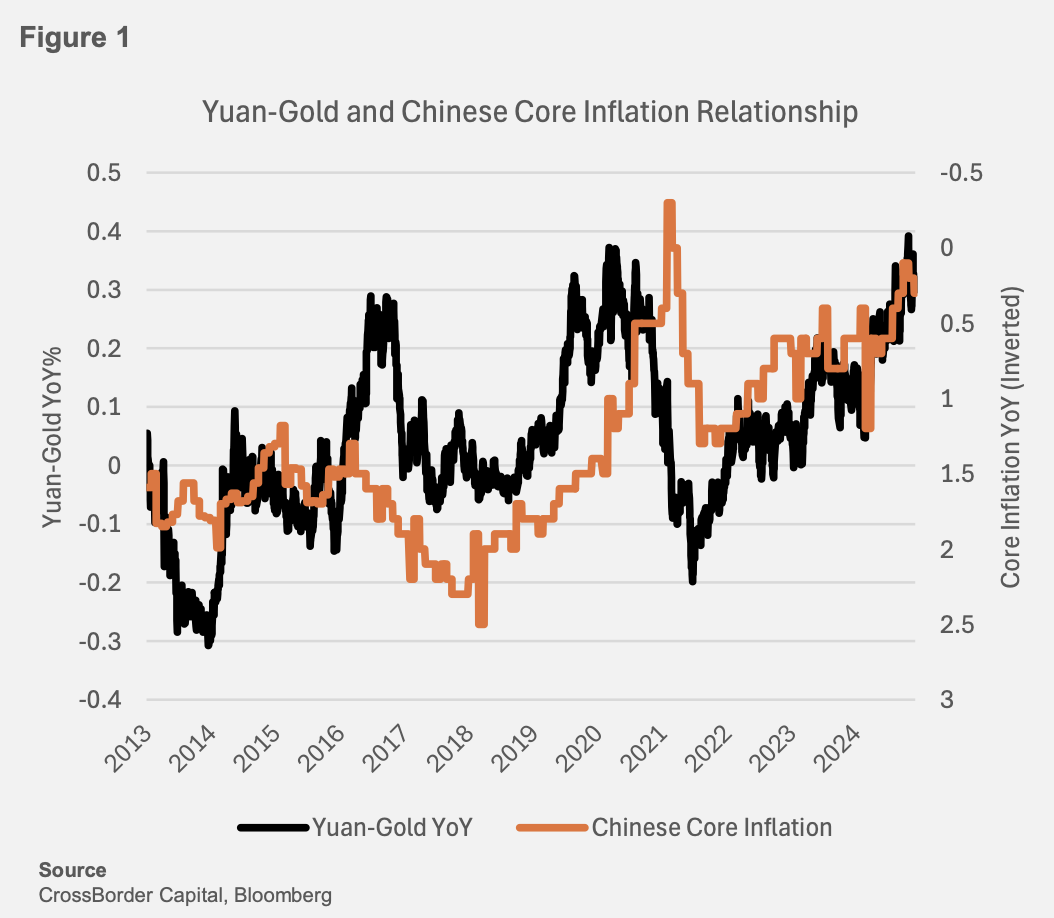

Michael Howell’s latest report revisits his thesis that China’s mounting debt-deflation has forced the country into an unconventional monetary strategy, using gold as the conduit for currency devaluation. With the Yuan-dollar exchange rate tightly managed and capital outflows constrained, Chinese investors increasingly turn to gold as a hedge against financial instability. Granger causality tests confirm that Yuan-gold prices now lead US dollar gold prices—a structural shift driven by domestic monetary stress and Beijing’s policy choices. This evolving dynamic positions China as a central player in global gold price formation, with profound implications for international markets.

Colombia remains neither fish nor fowl

The peso is not in the clear. Colombia has been caught all year in the regional FX sell-off - and with nominal and real rates that are lower than Mexico or Brazil. The external position ok, but not exciting. Current account deficits have narrowed, and the basic BOP is in balance, but adjustment momentum has faded without leaving Colombia much wiggle room. The big downturns in durable auto sales, retail spending and cement usage all occurred in 2023, and demand is clearly rebounding this year. This is good for underlying growth and earnings, but also threatens the external position going forward. Jonathan Anderson doesn’t see an equity or dollar credit story at this juncture and sees sovereign dollar bonds as fairly priced.

Ghana: What does Mahama and NDC election win mean?

The Election Commission of Ghana released the partial results of the Dec 7th general elections. With the bulk of constituencies counted, the main opposition NDC party and its flagbearer, John Mahama, won the respective legislative and presidential legs of the ballot. The ruling NPP and its flagbearer and vice president, Mahamudu Bawumia, have accepted the results and officially conceded defeat. Mahama’s administration will assume office in January. In their latest report, Signal Risk assesses how a change in administration might prompt significant shifts in the country’s economic and political trajectory, or if debt restructuring commitments and an IMF programme will render the medium-term environment static.

Commodities

Lumber: Cracks in the market

The North American lumber market continued to weaken last week as price declines, initially concentrated in Southern Yellow Pine (SYP), extended to Spruce-Pine-Fir (S-P-F) and other species. Benchmark S-P-F 2x4 prices dropped by $8 to $462, while SYP 2x4 prices fell an additional $20 week-over-week to $338. With wintry weather affecting Canada and the northern US demand is slowing, and buyers are expected to manage inventories cautiously, particularly in states with year-end inventory taxes. The ERA team anticipates further near-term price declines across all species. However, with SYP prices now at or below cash cost levels for many southern mills, additional market-related sawmill downtime, potentially aligned with the holiday season, is likely.

Gold: Rangebound in a consolidation phase

According to Sohail Yousaf gold continues to exhibit range-bound behaviour, with critical resistance at $2,660 and support firmly positioned at $2,630. A breakdown below $2,630 could trigger a deeper correction, targeting $2,560 as the next major support zone. The broader bearish outlook remains intact, particularly as gold trades below the descending trendline, highlighting the persistent downward pressure. As Sohail forecast earlier, the $2,450-$2,480 level could be a key area for accumulation before another potential bullish leg upward. Price action within this range suggests a cautious approach until a breakout occurs. Alternatively, a selling opportunity can be considered from the current price level, but with a strict stop-loss just above the descending trendline. This strategy ensures protection against potential breakouts while allowing for participation in the prevailing bearish momentum. Patience is key.

Oil market 2025 may be better than forecast

Prince Abdullaziz bin Salman, the Saudi oil minister, recently stated: “we honestly believe that the market next year would be better than what is being projected”. William Brown agrees, i.e., not a major market surplus as currently anticipated by the consensus. Prince Abdullaziz bin Salman went on to state that the primary reason for OPEC’s deferral of the production increase to the start of the second quarter is the fact that the first quarter in any year is a weak consumption period. Adding “the first quarter is not a good quarter to bring volumes. That quarter is known to be a quarter for building stocks.” William could not agree more. Innumerable times of the last 40+ years he has reiterated this phenomenon, and it is always reflected in his price forecast.

Is Bitcoin entering the death zone?

The death zone on mountains comes at 8,000m, where the air thins and oxygen becomes scarce. Markus Thielen ponders if Bitcoin is entering an equivalent zone, where momentum begins to wane. Long-term holders have resumed selling, and the Bitcoin Value Days Destroyed (BDD) multiple has risen from 0.5 to 2.0, signalling that older coins are being sold. Markus expects a brief consolidation phase before the market regains momentum. However, traders should now pay close attention to which positions are outperforming and which are underperforming, as the rally enters a phase where not everything will continue to rise. On-chain data highlights an increased risk of profit-taking, signalling caution. A true breakout above $100,000 could signal a strong buying opportunity, but exercise caution if it falls below the critical support level of $95,000. The air gets thin in the death zone, but that doesn’t mean you’re at the top yet.

Gold and silver: Medallion pricing and China’s economic push

In this presentation, Jeffrey Christian discusses the recent performance of gold and silver and his expectations for the markets going forward. The video begins with a look at China's economic strategy, and the country’s ability to leverage massive financial resources to stimulate its economy during times of global and domestic strain. Jeffrey then takes a look at silver bullion and medallion pricing, and on why some investors are finding it difficult to sell medallions at good prices. He explains the distinctions between various silver products and warns about the pitfalls of investing in non official forms of silver. The presentation concludes with a look at the recent surge in gold and silver prices, and the geopolitical tensions, increased global risks, and investor uncertainty driving prices.

Click here to watch.