Europe

Betaville smokes out £1.5bn Wood Group takeover bid

On Feb 22nd Betaville broke the news that the FTSE 250 company was at the centre of a takeover rumour. Later that day management confirmed they had received an approach from Apollo. The PE firm has recently made a final offer at 240p a share; a 60% premium from when Betaville first broke the story. Since then, Betaville has published several other alerts about UK, European and US-listed companies. These stories include takeover rumours surrounding INWIT - where Reuters subsequently followed up that story, suggesting PE firm Ardian has appointed bankers from JPMorgan to work on an offer. Other alerts include One Swiss Bank and US-listed Paratek Pharmaceuticals.

Do get in touch if you would like to read these alerts or have any enquiries about subscriptions.

Consumer Discretionary

FY23 guidance (sales +5%, EBIT +10% Y/Y) is overly cautious and should be revised upwards mid-year (AIR forecasts sales +10%, EBIT +15%), following strong 1Q23 activity, new price hikes of +5% in May 2023 (inflation pass-through), and re-opening of China. Active management of store portfolio should reduce operating costs to 19% of sales by 2025 (vs. 26% last year) and lift gross margins above 62%. The company’s 2025 targets (sales of €4bn, EBIT margin of 12%) should be reached in 2023. TP €90 (35% upside).

AIR’s 2023 Top 10 European Best Ideas Portfolio was +19% in 1Q23 and has outperformed the Euro Stoxx 50 by +205% since launching in 2012.

Consumer Discretionary

Woozle upgrades the stock to Buy following their latest interviews with dealers across Europe and the US - RNO prices are +6% Y/Y in 1Q23 following the launch of several higher margin midsized and compact vehicles in 2022. Volumes are +13% Y/Y (vs. consensus of -8%) driven by a 27% increase in sales in Europe, where RNO has gained market share and its Dacia Spring is now the second most sold EV in Europe, behind Tesla. Elevated raw material / energy prices, rising wage pressure and logistical problems are the main risks to look out for 2023. A lack of truck drivers in Europe was also flagged, but this has mostly impacted Volkswagen and Stellantis.

Technology

Report by

AlphaBox Advisors

AL

M&A looks imminent especially given the latest round of banking industry turmoil - AlphaBox upgraded the stock to Buy earlier this year with a 12-month TP of CHF77, valuing TEMN at 20x FCFF on their normalised 2023E of CHF280m. However, in their initiation report they also stated that there could be material upside from a takeover. At a buy-out multiple of 10x EV/Sales (which is reasonable given that over the last 12-18 months, M&A in the tech space has occurred at 9-15x EV/Sales), TEMN would be worth CHF110 per share (70%+ upside).

UK Mid Cap Technical Review

The FTSE 250 index finds support at the bottom of the 2023 range but is still losing relative momentum vs. the FTSE 100 index. Messels continues to see selective improvement in IT Services stocks such as Computacenter (renews price and relative bases at 2020 peaks), Kainos (has rallied from support at the bottom of recent ranges) and Softcat (finding 6-year uptrend support). They have a new Buy on Playtech (reaches support from the prior range and holds the relative base). In Real Estate, they highlight opportunities in Big Yellow and Safestore. They have also closed their long in Plus500 after the stock found resistance at the highs and lost relative momentum.

North America

Consumer Discretionary

Negative consumer sentiment continues to gain momentum for OLPX. Ulta partnership is showing cracks and the once disruptive category-killer bonding proprietary technology has lost meaning as lower-priced "dupes" and higher-end competitors invade the transformative hair treatment space. Unannounced retail launches are popping up across all channels. New marketing and store selling initiatives have yet to show up at point of sale. Replenishment at retail and in salons continues to be at risk. Getting back to launching new innovation and re-establishing trust with the consumer could turn this story around, but new turnkey B-grade launches are a distraction and the consumer continues to read company messaging as stubborn and tone deaf.

Consumer Discretionary

Brian McGough thinks the brand is growing too quickly and outright recklessly. ONON’s model reminds him of when Kors blew up in 2015 - it sold indiscriminately into wholesale, resulting in discounting, and a slowdown in high margin DTC sales. Brian also thinks the situation is reminiscent of early cycle Under Armour which was billed as “the next Nike”. At least UAA was a real brand, he is not convinced ONON is. To date, the company has managed to keep discounting to a minimum, however, this will change in 2023 as 190% inventory growth flows through the channel. Brian sees 50% downside and would pair a short position here against longs in Deckers and NKE.

Consumer Discretionary

Misperception around the extent to which SCI continues to benefit from the pull-forward of excess deaths due to Covid - management is guiding to a MSD % decline in deaths for FY23, but the Presenter of this short pitch (at MYST's Bear's Den Idea Forum) suggests a 15-20% drop is more likely. Even more troublesome, imminent new regulatory reforms are expected to create significant long-term headwinds for SCI and the industry overall. In 2018, when UK Regulators forced funeral homes to fully disclose pricing, the stocks subsequently declined more than 50% as margins were impacted meaningfully. Forecasts FY24 EPS of $2.00 (vs. consensus $3.88). TP $40 (40% downside).

Consumer Staples

MO will launch a heated tobacco capsule called Swic and a new addition to its existing nicotine pouch brand, On! Plus. The tobacco giant said that both products are in development. It has yet to file premarket tobacco product applications (PMTAs) with the US FDA. MO is also considering including cannabis and caffeine pouches in its offering of non-nicotine products as part of its growth strategy.

Consumer Staples

2023 guide is $9.5bn in FCF - dividend is $8.0bn + $1.5bn in repurchases to hold shares flat. Tax dispute on transaction splitting may need to be appealed soon. KO estimates it will need to post $5.2bn in cash and the dispute involves $14bn in potential payments. Interest cost may rise and share buybacks fall. Furthermore, inventory DSIs finally jumped 10 days and could pressure gross margin more than forecast as management says pricing will be hard to gain in 2023 and Latin America. Pricing exceeded FX hits by 10-20 points of late.

Consumer Staples

A burgeoning growth story - market share gains should accelerate, margins should improve, and earnings will likely exceed Scott Mushkin's prior estimates over the next few years. His revised FY24 and FY25 EPS estimates are $6.07 and $7.24, respectively. Scott has increased his long-term sales growth over the 10-year forecast period to ~4% (c.100bps higher than his previous forecast). Comp growth in Walmart US (ex fuel) averages ~3.5%. As far as profitability, he has modelled expansion to a 6% operating margin for Walmart US by FY28. Scott sees a good chance of the share price eclipsing $200 over the next 12-18 months.

Financials

Effectively insolvent - Neeraj Monga does not believe that the so-called deposit lifeline changes the underlying economic reality of the bank. Interest expense will rise exponentially, while the liquidity problem is further compounded by an asset-liability mismatch of immense proportions. Moreover, 90% of the loan book of $148bn is dedicated to real estate, of which non-amortizing single-family loans are $51bn and multi-family loans are $11bn. Thus, 43% of FRC’s book of loans is to a sector under intense pressure with the Fed trying to control inflation. FRC is a living and currently breathing Murphy’s Law in action; anything that can go wrong will go wrong, and at the worst possible time.

Healthcare

Abacus expects Grail to be divested in 2023/24 and the regulatory mess to clear over the next 12 months - this leaves the core ILMN business, which looks attractive given the current instrument upgrade cycle and high elasticity of demand should allow mid-teens revenue growth in 2024/25 with 25-28% operating margins and enable ROCE to recover back to >14%. Increasing competition is not considered to be a major factor as it will be hard for newcomers to grab a meaningful share, especially in the high-throughput segment. They see the core business generating EPS of ~$10 sometime in 2026 vs. consensus estimates of $5 in 2025. TP $350 (50%+ upside).

Broad-based strength in non-residential construction

Industrials

TRG continues to receive feedback that non-res construction is performing strongly and go-forward indicators are equally positive. The main concern from industry contacts is centred on project cancellation (which is very low to non-existent) and higher rates reducing owner willingness to pursue new projects (minimal impact thus far). Otherwise, sizable backlogs and the quantity of large projects gives them confidence on 2023 non-res and public-funded (e.g., roadwork) activity being strong. This supports their bullish stance on equipment rental (seen entering a “golden era”), agg & cement producers, distributors, equipment manufacturers, contractors, and service providers.

Materials

Q2 results are the latest in a series of disappointing earnings announcements, yet the stock continues to trade at a high PE multiple as investors expect the brand to remain protected in a soft economic environment. Hamed Khorsand would agree if it were not for inventory and accounts receivable at high levels. Furthermore, WDFC is adding to its debt balance to repurchase shares and issue a cash dividend, which he does not believe is sustainable when the business is facing unit volume challenges. Hamed expects WDFC’s stock to come under pressure as investors reassess the fundamentals of the business vs. purely relying on brand recognition. 12-month TP $88 (50% downside).

Technology

Report by

Inflection Point Research, LLC

IN

Could report an in-line Mar quarter, but IPR expects AAPL to guide down as it faces headwinds on softening demand across multiple product lines - IPR’s US carrier store checks suggest iPhone 14 inventories increased in Feb / Mar. While China iPhone sell-through checks suggest ~10% growth for the quarter, the tech giant could find recent improvement difficult to sustain on normalising demand post-reopening. Checks on Macs are consistent with last quarter, showing continued weakness with no end in sight. Checks with Apple watches, Air Pods, and other accessories paint a grimmer picture of forecasts down up to 50% Y/Y, indicating significant inventory build due to very weak end markets.

Advanced AI: Sink or swim time for cybersecurity vendors

Technology

Report by

Blueshift Research

BL

How are AI advancements and hype affecting the cybersecurity industry? What are data security vendors doing with AI/ML and cybersecurity automation, and can they protect their market from the major cloud operators with their investments in AI-driven security for their own platforms? During the interviews conducted by Blueshift, industry sources were also asked how they would play the sector near to mid-term and out over time. Companies discussed include Amazon, CrowdStrike, Cisco, CyberArk, Fortinet, Google, IBM, Microsoft, Okta, Palo Alto and Zscaler.

Developed Markets

Pause, not pivot!

More central banks are appearing comfortable in pausing hikes. Is this mission accomplished on dispatching inflation? No matter what markets assert, says James Aitken, a pause is not a pivot, and we may be shifting to a new phase where central banks face a difficult trade-off between growth and inflation. He remains concerned that markets are positioning upfront for the luxury of the ‘inevitable’ rate cuts later in 2023, with inadequate or no reflection on the damage incurred by what might trigger these ‘inevitable’ rate cuts. Investors should remain disciplined. James recommends allocating capital to well run, high cash flow generating companies.

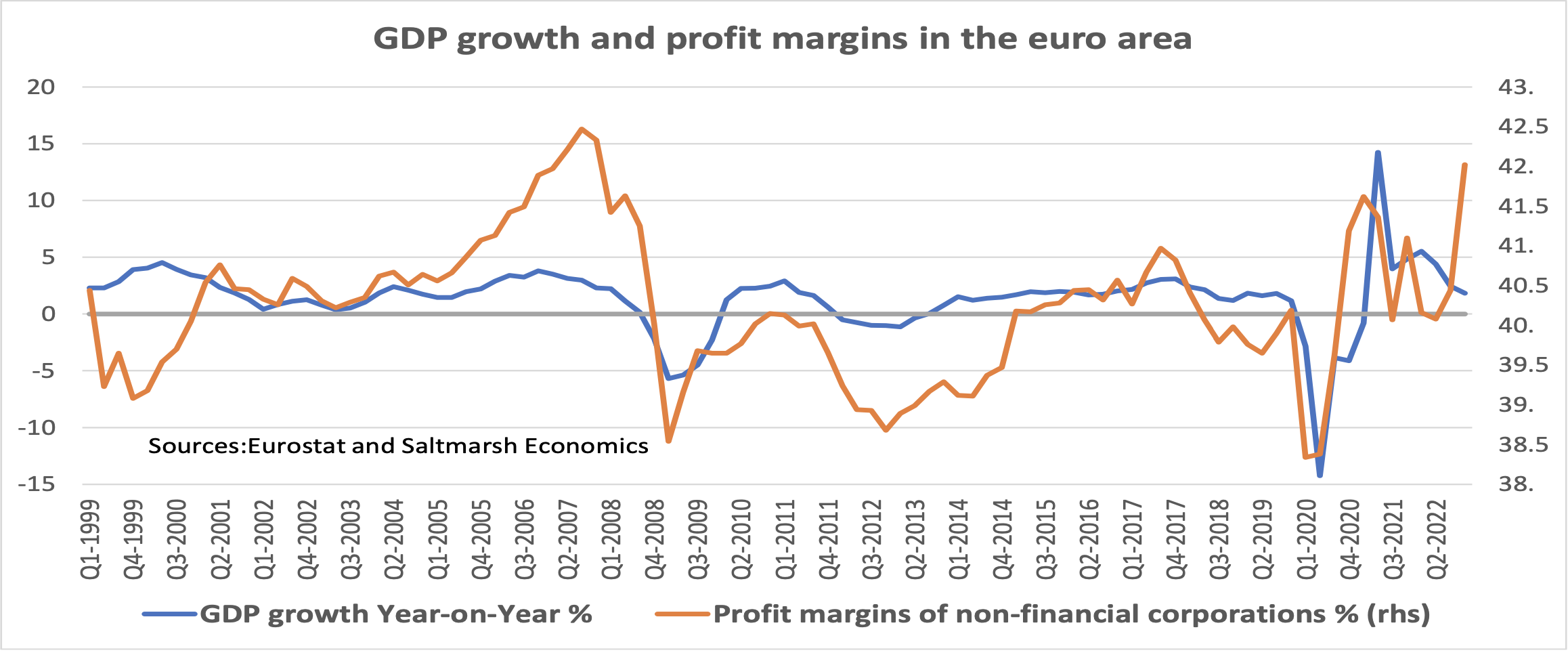

Eurozone: Profit margins and inflation

For quite some time, the ECB has been warning about rising profit margins driving inflation higher. Normally, peak margins occur near the peak of an economic cycle, not at what might be nearer the start of a long, drawn-out recovery; latest data suggest there was a significant rise in profit margins of eurozone non-financial corporations in 4Q/2022, taking them to levels last seen in Q4/2007 (see chart). As a general rule, rising profit margins might be seen as favouring equities over bonds, especially if we are still not near the peak of this economic cycle. Indeed, David Owen and Marchel Alexandrovich both expect economic growth to surprise on the upside.

Falling inflation to bring down the Dollar in 2023

US inflation will continue to decline at roughly the same pace as it rose in 2021 and H1/2022: historically, there has been scant evidence of downside stickiness in inflation, even if there is evidence of downside price and wage level stickiness. Goods price inflation in the US, in fact, could turn negative later this year. As long as the world does not fall into deep recession, the USD will lose the cyclical support that has propelled it some 20% deep in overvalued territory vis-à-vis the G10 currencies – expect a substantial (10-15%) depreciation in the coming 4-6 quarters. European inflation will also likely decline sharply this year, albeit with a six-month lag to the US.

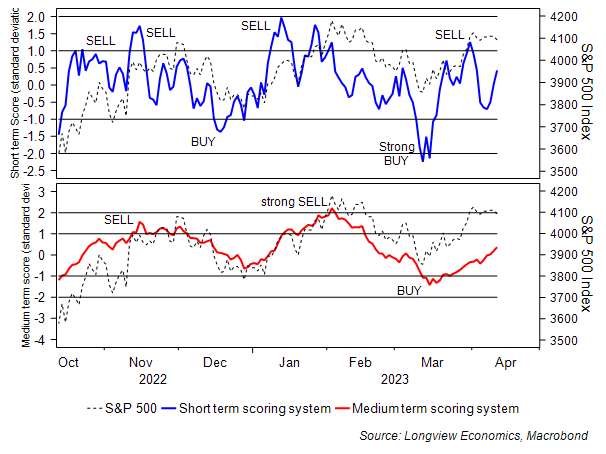

US: Building short S&P500 positions

Report by

Longview Economics

The case for building short positions in S&P500 futures is growing (on a short term 1-2 week basis). S&P500 futures rallied hard on the release of benign CPI data but failed to hold onto these gains. Whilst currently it remains within the trading range of the past 8 sessions (since April), the index did generate a bearish key day reversal, a technical price pattern that often signals the end of a bullish run in an index. Move ¼ SHORT S&P500 June futures at 4,150, implementing a stop loss 2% above entry.

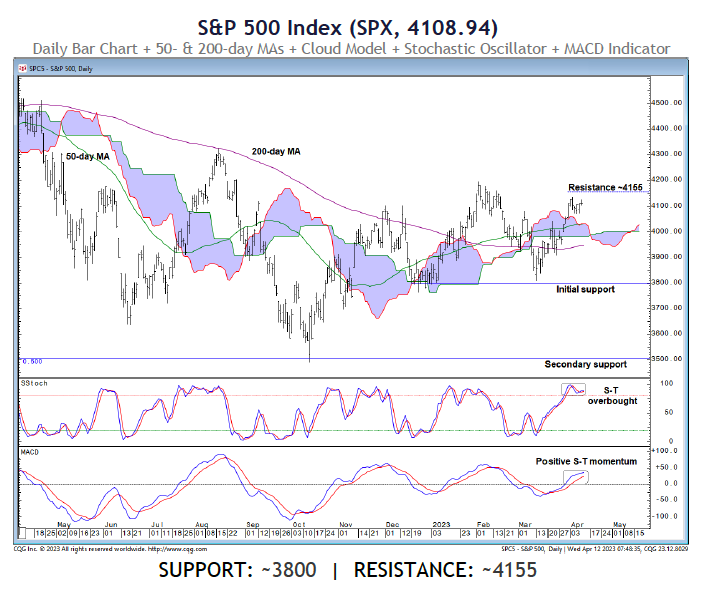

SPX: Major shift may be underway, but indicators support a bear market cycle

Report by

Fairlead Strategies

FA

Short-term momentum is likely to wane for the market as a whole, with the Fairlead Strategies’ team noting the mega cap stocks now showing daily MACD sell signals – maintain a bearish bias. Resistance looms near 4,155 with initial support near 3,800. Should the SPX post consecutive weekly closes above ~4155, its downtrend would be reversed, dictating a bullish intermediate-term bias. Should the CBOE VIX break support at 18.45 decisively, that would be another bullish indication, reflecting a major shift in market sentiment. Barring these developments, the team would respect the posture of the monthly MACDs, which remain supportive of the bear market cycle.

A rotation the market is oblivious to

The second phase of the bank crisis that started one month ago has now arrived, claims Michael Belkin. This secondary credit crisis stage isn’t about banks failing, it’s about a decline in lending and a slump in economic activity. Sector, industry group and stock rotation are beginning to reflect the approaching recession, yet this profound shift is nowhere to be seen in the financial press. For asset managers, it’s risk-off all the way, and a complete reversal of the investment theme of the past five months. Looking for alpha? Go overweight utilities, staples, healthcare, energy and gold stocks. Michael also adds the NYFANG+ index as a new SHORT recommendation.

US employment is far above the sustainable level

Gerard Minack stresses that the core of the Fed’s inflation problem is wage growth lifting service sector prices. Now, labour market data is as important to the Fed as inflation data. The labour market is shifting from excruciatingly to very tight conditions, employment growth is far above what is sustainable and there is no case for easier Fed policy to be made. Of course, history says if you use backward-looking labour data to set forward-looking monetary policy then cyclical accidents are almost guaranteed. Services prices are the key to core inflation, and the key to service sector inflation is wage growth, which is now key to understanding Fed policy.

Be careful, some safety plays may not work

Report by

Harlyn Research

Simon Goodfellow continues to see the positive correlation between equities and bonds as a threat. The top-down consensus is rightly gloomy about the outlook for earnings estimates and equity benchmarks in the US, yet the market refuses to go down. An additional catalyst is needed to shake us out of the current trading range. A mild US recession is not the main risk to balanced portfolios, provided bonds rise while equities fall; instead, Simon worries about a bear market in everything if the current relationship between the two continues. Investors can mitigate this by lowering the beta in equity portfolios and increasing exposure to Europe, cash and money market funds.

Emerging Markets

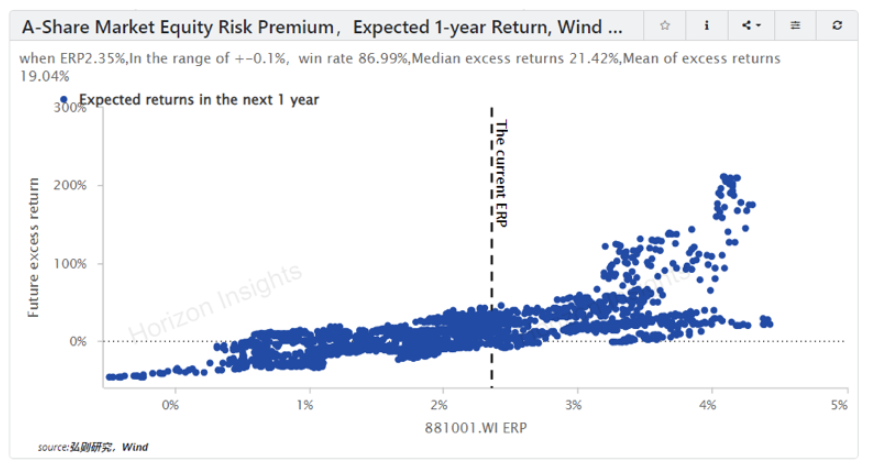

China: A-share market strategy

The A-share market’s valuation remains in a low range with a very large possibility of seeing a decent return in the one-year horizon. Most importantly, the market’s valuation multiples have not yet fully reflected the sector’s improving fundamentals and we could be seeing the start of a new bull run. However, investors should expect a 10% correction of the recent AI-driven market rally before the bull is finally let out the gate.

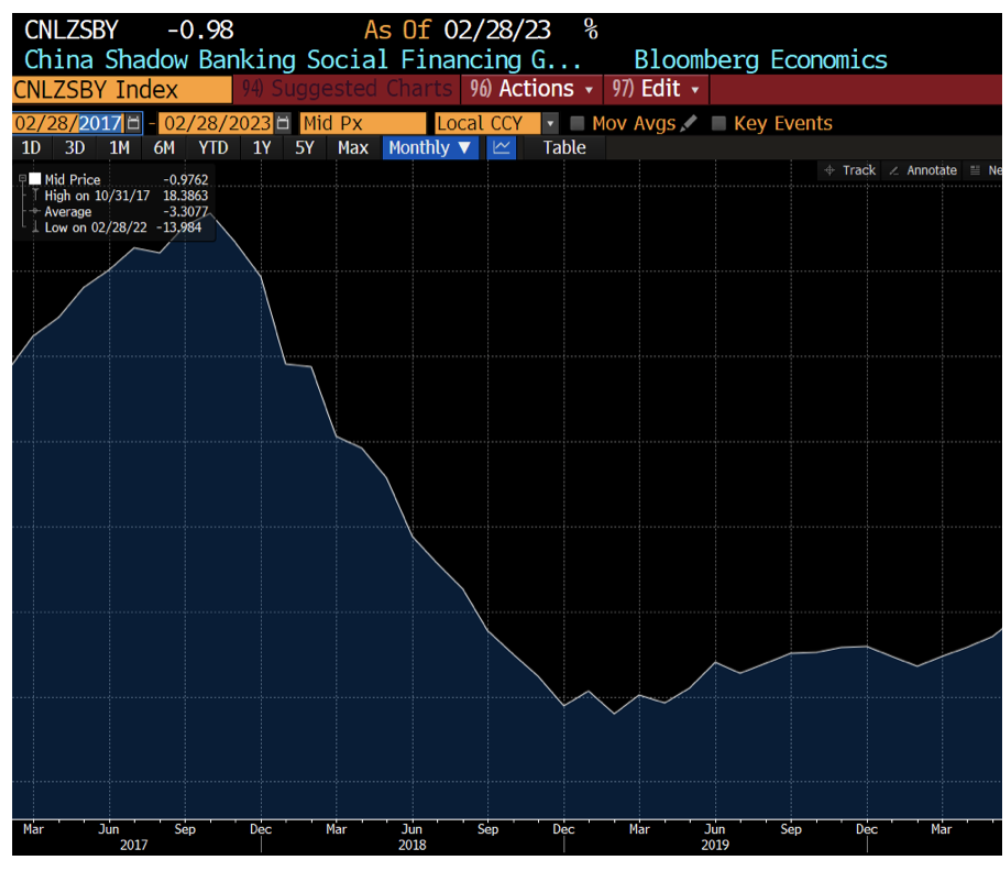

China: Lurking in the shadows

Report by

Ollari Consulting

Despite strong credit supply, demand has remained subdued in recent months. Christophe Ollari comments that the March figures show some improvements with firms making greater use of the government’s loan support. They also show a recovery in household demand for mortgages – another sign the property market slump is starting to ease. Christophe points to a key chart (see above), remarking that the current credit stimulus push is nowhere near the past ones. Is the government being shy?; are we seeing limits of the old model?; or perhaps a desire to avoid old mistakes? Watch the Shadow Banking data closely to assess whether Beijing is on the verge of going back into its past exuberance.

Bolivia: A quagmire

The government is making desperate moves to try and avoid either a depreciation of the exchange rate or the imposition of stricter capital and currency controls. A battery of measures including the selling of SDRs, an attempt to exchange gold for liquid reserves and the offer of preferential FX to exporters are part of the government’s strategy to reinforce liquid reserves. Marcos Buscaglia thinks all these measures will only provide a brief respite as Bolivia’s fundamentals remain flawed: declining gas exports and hence a lower trade balance, an overvalued real exchange rate and a wide budget gap. Eventually, the country will have to resort to either stricter capital and currency controls or a depreciation of the official FX.

All great in India, except for this

The India growth trade is going well. Demand and output are strong, and both corporate earnings and equity prices continue to outperform broad EM. Moreover, inflation pressures are receding, and lower fuel and commodity prices have helped rein in external deficits as well. “What’s not to like?”, asks Jonathan Anderson. However, there is one big surprise, as the latest flow lending numbers have simply collapsed. These numbers are volatile and the reason for the tanking of the credit cycle is not yet clear, so Jonathan retains his views on growth and equity prospects but advises investors to watch closely.

Turkey: Could Erdogan lose?

Turkey’s President Recep Tayyip Erdogan is one of the great survivors of modern politics, but Niall Ferguson points out that in the next month he will face the most difficult election of his career. Nearly all polls suggest that the opposition coalition has the votes to oust him from the presidency—despite his control of the media and his repression of opponents through the legal system. There remains a chance that he pulls off a surprise win, that he suppresses the vote sufficiently to retain power, or that he wins the support of the military and security services to steal the election openly. However, Niall expects Erdogan to lose the election, in which case he will probably leave power.

Emerging Market Selector

David Ranson’s Emerging Market Selector report summarises the outlook for EMs on a country specific basis, using market signals of economic growth, inflation, relative valuation and currency “surprise”. It incorporates the results of new research on the combined forecasting power of corporate quality spreads and gold prices. In David’s latest report, Egypt and Pakistan are most strongly in favour, whereas the Czech Republic, Jordan and Mexico now move to most strongly out of favour.

Commodities

Oil after the cut

The oil market faces two countervailing forces. Demand indicators are bearish, with disappointing recent results in the US, Europe and China, and a slow recovery ahead. Yet a coming supply-side shortfall in the second half of the year looks set to overwhelm even a muted recovery in demand, and Niall Ferguson thinks OPEC+ is willing to make further cuts to ensure price stability, especially if we see prices pushed below $75. He is cautiously bullish.

Lithium: A trade off

Lithium prices surged to record levels but have now rolled over; investors face a trade off between strong cash generation near-term versus risks of holding (or acquiring) shares that are falling. Higher lithium prices near-term does mean the sector looks “cheap” with a PE of 7.7x and EV/EBITDA 5.6x in 2024 in David Radclyffe’s forecasts, but he is not bullish near-term. Greater upside may be available with juniors that successfully develop projects, but David expects many investors to minimise risks and stay with large cap players. Preferred stocks are SQM and IGO, offering value and production growth.

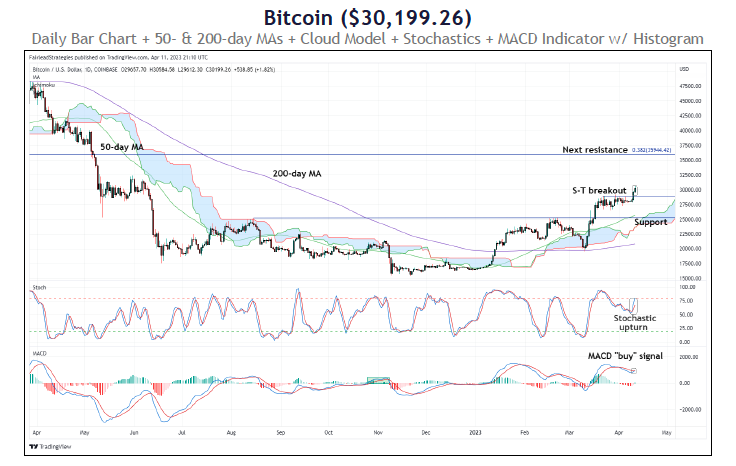

Bitcoin: Short-term bullish

Report by

Fairlead Strategies

FA

Bitcoin has pushed out of a three-week consolidation pattern in a bullish short-term development. The breakout is associated with upturns in Fairlead Strategies’ short-term indicators, supporting upside follow-through with short-term momentum having been renewed. Next resistance is at a 38.2% Fibonacci retracement level, near $35.9K, which the team view as an intermediate-term upside objective assuming the breakout holds through the end of the week (i.e., Sunday). Initial support for bitcoin is ~$25.2K, defined by former resistance. With the monthly MACD still pointing lower, maintain strict attention to risk management with bitcoin long positions.

High purity manganese

In a special market update, CPM Group’s Andrew Zemek discusses the opaque and obscure High Purity Manganese market and its critical importance to the battery and energy market.

Click here to watch.