Europe

Consumer Discretionary

Another successful short idea from Alumbra Research - Husqvarna's share price declined by 36% while the company was on their Active List (Jun 23-Feb 25) having issued multiple profit warnings and cut its dividend by 67%. In their initiation report, they raised concern that excess inventories combined with intensifying competition in robotic lawnmowers may cause the company to have to slow down production and write down excess stock, thereby pressuring margins. Alumbra also raised concern that Husqvarna’s credit metrics did not meet the threshold to maintain the company’s investment grade credit rating and that this would put the dividend at risk.

Consumer Discretionary

In the past 20 years, Pierre-Olivier Essig has never seen as many red flags surrounding LVMH as he does today. In addition to terrible 4Q24 numbers, he highlights succession change, brand fatigue, low value retention, supply chain ethics, designer casting mistakes, unjustified pricing, as well as specific issues attached to almost every division. Pierre faced huge resistance from clients 12 months ago when he advised selling LVMH shares at €822, however, that proved to be the correct decision and in Oct, he then upgraded the stock to Buy after it fell through €600. With the share price having recently moved back above €700, Pierre turned bearish once again. He expects Hermes m/cap will exceed LVMH’s within the next year.

Consumer Staples

Vision’s bear thesis focused on growing competition in protein powder, potential lack of pricing power in the face of elevated input costs; weak positioning in diet and RTD category; weak margins, ROIC and FCF; and inventory growth. The share price declined 23% on Feb 26th the day of earnings and the short generated alpha of ~45% vs. Stoxx600. Vision initiated 8 new shorts in 3Q24, 10 in 4Q24 and 4 so far in 1Q25 of which 10 were US, 8 European and 4 Asian. Consistent with their goal of finding liquid, non-consensus shorts, these 22 ideas had avg. m/cap >$15bn, avg. AD$V >$65/day and avg. SI% of free float of <4%.

Financials

Management has been heavily focused on improving the bank’s operations, while also being highly shareholder-friendly, with a commitment to distribute >€9bn by way of dividends and buybacks in FY25e. UCG also has material optionality in terms of M&A and in the context of a Europe that is insecure about diminishing US defensive support and stagnant economic growth, Fighting Financials thinks European regulators will be more open to supporting pan-European corporate “champions” across sectors, including financial services. Ultimately, they see the bank as one of the higher quality, more defensive names, able to benefit from certain structural and geopolitical dynamics coming into play across the continent.

Materials

At first glance the concept of RIO needing to raise equity for just one moderate (if overpriced) acquisition seems unlikely. However, GMR’s cash flow projections shows that RIO’s short term ability to repay debt is limited. Rising operating costs, flat to reduced revenue and especially rising capex to US$11bn this year is hitting FCF. GMR forecasts the base case FCF Yield of only 1.0% in 2025 (post Arcadium payment), slightly higher at spot. Assuming iron ore at US$107/t, RIO can easily debt fund Arcadium, with year-end 2025 net debt and leases of US$9.6bn, for Net Debt/Equity of 16% and Net Debt/EBITDA of 0.4x. Equity is not needed. Traditionally RIO has always respected its stock and never issued shares unless it had to. The latest speculation may possibly suggest RIO wants a clean balance sheet ahead of a larger deal to come.

Technology

CAP's share price has shown weakness since the announcement of a below-consensus guidance for FY25, highlighting concerns about its underperformance compared to peers and the delayed recovery of the IT services industry. Its revenue mix, with significant exposure to manufacturing in Europe, limits its growth compared to offshore competitors like TCS, Infosys and Cognizant, which are benefitting from recovery in financial services. Despite AI creating high expectations, its impact on bookings remains limited, causing delays in decision-making; however, AI presents significant opportunities in IT services as it drives demand for business transformation.

North America

The Power of Perspective: The Intelligent Investor’s Framework

Omaha Insights employs a systematic and rigorous approach to restating reported financial data, examining shifts in accounting standards and incorporating economic adjustments, thereby providing clients with an accurate view of a firm's underlying economic performance. At the core of this methodology lies their unique Competitive Lifecycle framework, which underpins their ability to generate powerful, actionable insights into equity risk and anticipated returns. Beyond precise financial restatement, Omaha’s platform equips clients with a customisable “lens” through which they can tailor financial analysis to align with their specific investment philosophy and strategic objectives. This approach allows for a uniquely personal perspective on data, empowering clients to uncover information in ways that traditional analysis might miss. Click here for further details.

Healthcare, tariffs and Energy/Renewables policy

With the US Congress moving forward with its budget legislation, there are ongoing risks that healthcare providers and managed care and the renewable energy tax credits will be negatively impacted as Republicans look to offset the cost of tax extensions. Aldis Institutional's policy-focused events provide investors with timely and actionable insights into the DC landscape. This differentiated platform combines small group conversations with key stakeholders and policymakers, with real-time market commentary from Aldis' senior team. Recent and upcoming event topics include the outlook for Medicaid-levered MCOs and Hospitals, Trump tariff impacts on healthcare and other sectors and potential changes to Inflation Reduction Act tax preferences for renewable energy.

Communications

RUM has been a beneficiary from massive election advertising spending, however, with the US election season over and rising pushback on content moderation, Eric Fernandez expects its business to suffer. He also thinks branded partnership opportunities and Rumble Cloud are overhyped. At its last earnings release, the company missed on the sales line and up and down the income statement. Prospects for breakeven are going to be pushed further out. Declining performance metrics, cash burn and potential dilution will weigh on the stock. RUM has always been expensive, but the investment by Tether goosed the price and it is now priced beyond perfection at 45x 2026 sales, making it an ideal time to short the stock.

Consumer Discretionary

Corto anticipates further declines as FTDR’s share price crashes post earnings - despite a Q4 revenue beat, most upside came from the 2-10 Home Buyers Warranty acquisition, with organic growth at just 3% (management guided for long-term organic growth in the HSD range, which seems like a stretch absent a sharp improvement in the housing market). Excluding A/C replacement revenue, core revenue declined in Q4, casting doubt on the company’s 2025 organic growth target. FTDR added 170k service plans, but without 2-10 HBW, service plans declined by 3%, continuing a downward trend since 2021. Membership trends also remain weak given the company's increased spending on sales and marketing.

Consumer Discretionary

New CFO Cath Smith has destroyed a total of (192%) alpha at seven different public companies since 2005. Her below-average ManagementTrack Rating of 3.0 is a downgrade to outgoing Rachel Ruggeri's MTR of 4.3 and will lower SBUX's C-Suite Rating despite CEO Brian Niccol's 8.1 MTR. Smith is classified as a: 1) "Capital Returner" Capital Allocator: 59% of career capital allocated towards Dividends and Buybacks. 2) High F.L.A.G. Risk Concern with a "Bad Compliance Record". 3) Inconsistent Guidance Forecaster: beats 35% of guidance given, misses 17%, in-line 48%. 4) Less Evasive on earnings call Q&A: during her Nordstrom tenure, JWN was ~27% evasive vs. SBUX's C-Suite ~33% evasive over the past five years.

Consumer Discretionary

VFC has not one brand problem, but three, which Brian McGough thinks can only be fixed by a quality CEO with a massive capital deployment programme. In VFC’s case, that would cost $1bn+ in incremental capital annually. But here, the company is also facing a crippling balance sheet problem and is responding by cutting costs out of the model, which is likely to cause the undoing of its portfolio. The only way out is a heavily dilutive equity deal of $2bn+. Without one VFC will almost certainly be backed into a corner to sell another brand (likely to be Timberland). Brian wouldn’t go long this stock over $10/share. Without an equity deal, a zero is not off the table.

Financials

2Xideas publishes deep-dive research on compounding stocks that have the potential to double within 5-7 years. Their latest report focuses on ICE, which has the following key opportunities to drive continued growth and operating leverage: 1) To win share of institutional client workflows as fully automated trading proliferates. 2) Drive growth across its energy franchise with products such as Environmental Futures or Dutch TTF Natural Gas contracts, while continuing to innovate around new products such as carbon allowance credits. 3) Drive a digital‑to‑analog shift in the mortgage origination process, consolidating the mortgage value chain and building marketable mortgage trading and data products in the process. In aggregate, 2Xideas forecasts a 5.3% revenue CAGR and 11.5% adjusted EPS CAGR through 2030E on an NTM P/E of 20x.

Healthcare Real Estate outlook

Real Estate

Kolytics' report analyses US and European healthcare real estate, examining demand drivers, supply imbalances, valuations and company-specific comparisons. In their report, they highlight how aging populations and rising primary care needs support long-term growth in Senior Housing and Skilled Nursing but caution that supply pressures and shifting sentiment could threaten their favourability. Once-popular sectors have already declined, while today’s “heroes” trade at lofty valuations, requiring sustained high growth to remain attractive - leaving them equally vulnerable.

Technology

INOD reported better than expected Q4 results demonstrating how demand for data training services is not waning. Furthermore, management has set 2025 revenue to grow by at least 40%. This is much higher than Hamed Khorsand was forecasting. He believes the investment in hiring more people should see the group being awarded more projects. With INOD now poised to exceed $300m in revenue in 2026, Hamed raises his TP from $45 to $74. The share price has increased by more than 300% since he initiated coverage with a Buy rating in May last year.

Technology

SPR’s latest channel checks indicate that large deals are finally progressing after previous delays as enterprises were still evaluating their alternatives and negotiating with Broadcom. However, some channels criticise NTNX for its rigid pricing strategy, suggesting the firm should adopt a more aggressive sales approach like Pure Storage. As expected the Dell / NTNX partnership continues to grow and SPR also believes NTNX is making progress on enhancing its Acropolis Hypervisor (ACH), that some estimated previously had ~80% of the functionality of VMware ESX. Enhancements to ACH will make it easier for NTNX to replace VMware, especially in complex operating environments.

Technology

In addition to the last two quarters benefitting from a lower tax rate, BTN’s earnings quality review identifies several other factors worth noting: 1) Concerning movements in receivables and contract assets. 2) Non-GAAP income far exceeds FCF. 3) Allowance for bad debts has fallen to under 3% of receivables from as high as 8% despite higher international sales (this added 12 cps to 2Q25 earnings that beat by only 8 cps). 4) Warranty accruals have fallen from 6.6 days of sale to 2.5 days since 2021. Returning the accrual to 5 days would be a 52-cps headwind over several quarters. 5) Unsustainably low depreciation from using older equipment. 6) An unusual auditor change.

Asia

India Equities: Prices drop, eyes pop

There has been a steep decline in the Indian equity market. The BSE Sensex and Nifty are both down 6.6% in CY 2025. However, the smaller companies, represented by the BSE Midcap and BSE Small cap Index, have dropped significantly by 16.6% and 21% in CY 2025, respectively. Some of the reasons attributed for this decline are selling by FIIs, a depreciating currency and the high valuation of stocks. However, with this correction, there has been a substantial increase in insider buying in Indian stocks, especially in mid and small-cap companies. Historically, such insider buying has signalled an inherent value that has not been captured in its stock price at that point or an approaching positive shift in the business cycle.

China’s recent high-profile meeting with private entrepreneurs signalled Beijing’s strategic priorities, highlighting firms advancing state goals while sidelining others. Key invitees included Alibaba, Tencent and Huawei, while Baidu, ByteDance and JD.com were absent. This distinction suggests Beijing’s support for companies driving innovation in AI, advanced manufacturing and strategic industries like EVs and semiconductors. Xi Jinping reinforced the Party’s control, urging businesses to serve national interests and promote "Common Prosperity". Firms like DeepSeek, Alibaba and BYD align with these objectives. Conversely, Baidu and other omitted firms may face tolerance but lack government backing.

Another strong month for EM Telcos

Communications

The EM Telco industry has been transformed, with ROIC rising and real revenue growth for the better managed companies in good markets. This has resulted in a strong performance from New Street’s top picks, which are now up 15% on average YTD. IHS Towers and Airtel Africa have been the stand-out performers, up 25% and 24%, respectively. New Street’s report includes a run through of the key news items that investors in this space should be aware of. When viewed in aggregate they think competition, regulation and execution are coming together at the moment to drive good returns for investors.

Financials

Premium promises, discounted truths - PB's Non-GAAP figures are a mystery, while analysts at Iii also question the reliability of its audited numbers. Key themes from Iii’s report include: 1) Has the company violated IRDAI guidelines? 2) Number meddling allegations. 3) Illusionary improvement in profitability. 4) The curious case of Paisabazaar income. 5) Insurance business - the story booster. 6) Accounting policies out of sync. 7) Excessive issuance of ESOPs / co-founders have sold large amounts of stock post-IPO. With no evident signs of sustainable profit-making, the future looks bleak.

Developed Markets

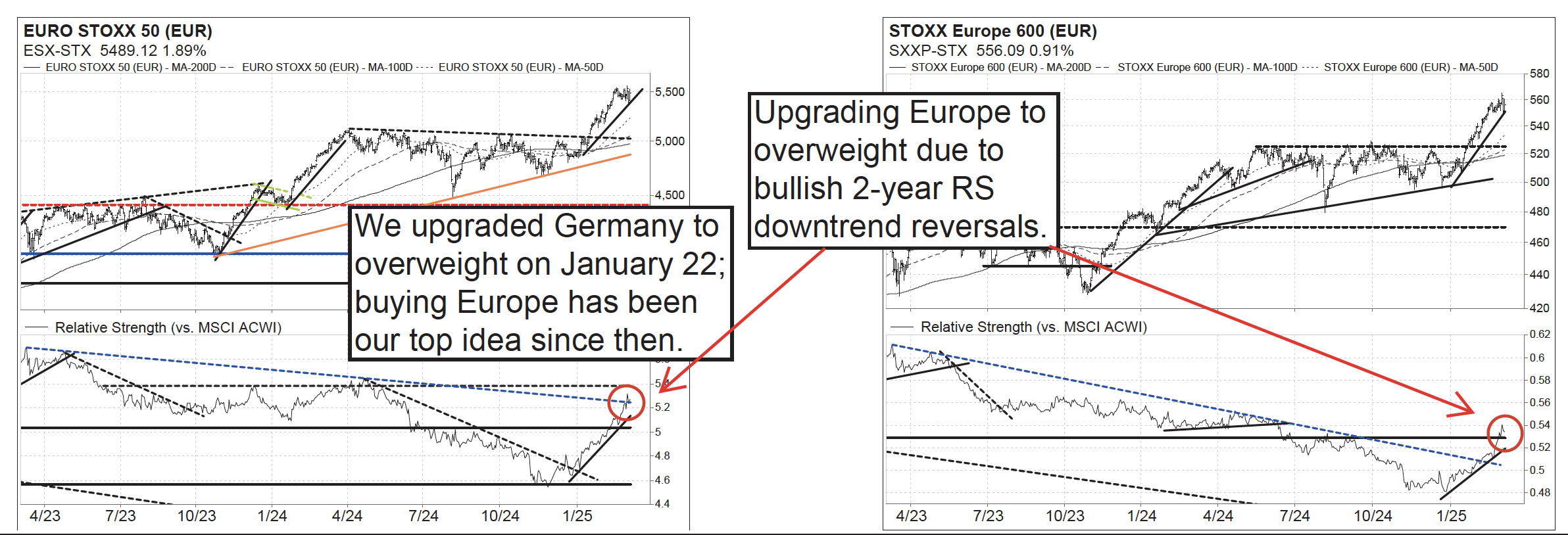

Europe: Fattening up

Last week the Vermilion team discussed how both ACWI-US and the S&P 500 displayed false breakouts, and to look for near-term pullbacks to range supports at $116 on ACWI-US and 5770-5850 or 5600-5670 on the S&P 500 in the coming weeks, where they would be buyers. Both levels are close. It is possible ACWI-US finds support here at the 200-day MA as it has already provided two ideal buy opportunities during this 2+ year bull. In Europe, the team has been preparing for a breakout since January, their favourite recent buy idea. They are now upgrading the broad Europe region (EURO STOXX 50, STOXX Europe 600) to overweight due to continued outperformance and participation from other countries. In terms of global equities (MSCI ACWI), the team’s intermediate-term outlook remains bullish as long as ACWI-US is above $116. The team continues to remain overweight the US and Germany.

Germany: An emboldened defence

As is characteristic of its post-war history, Germany’s leaders took a very long time to move. But when they do, they move radically. The recent decision clarifies that Berlin now means Zeitenwende for real and that the geopolitical situation has fundamentally changed, with Europe having to take responsibility for its own security in the medium term. The fiscal howitzer Merz intorduced will benefit all of Europe in economic terms, as not only German, but all European defence companies will profit. With Merz, Germany will have a leader who sees German and European strength as complementary. The consequences for markets, macro, and geopolitics should not be underestimated. Niall Ferguson remains long defence and sees a growing case for European infrastructure and green tech.

Netherlands: Inflation edges up

Based on the fast estimate, Dutch inflation was 3.8% YoY in February. In January, inflation was 3.3%. On a sequential basis, consumer prices rose 1.1% in February. Based in the European Harmonised Consumer Price Index (HICP), the fast estimate of inflation in the Netherlands was 3.5% in February vs 3.0% in January. The published data show that the energy & fuels category tempered inflation. Food, beverages & tobacco as well as services are still the main ‘inflation boosters’. In both categories, the trend in still up, which does not bode well in Henk Slotboom’s view. It is likely to keep wage inflation high, whereas especially food inflation will continue to weigh on consumers sentiment. Henk therefore reiterates his neutral stance on companies with a high exposure to consumer spending in the Netherlands.

Navigating a multi-polar fragmented world

Craig Ferguson’s core macro/AA view says a 40yr disinflation cycle ended in 2020 and that a new multi-decade inflationary cycle began. This has seen cash rates rise, global growth slow, rates get cut and inflation fall. At the start of 2025 Craig points out that we are now near the end of the first up (2020/22) and down (2023-24) cycle, so a new cycle may be starting. Craig’s takeaway from his detailed analysis of US/Trump geopolitical & economic policy is to expect stagflation forces to unfold and impact AA portfolios during 2025-28… For now, Craig says we need to face up to the notion that markets are priced for perfection in an uncertain and fragile geopolitical, economic and military world. The new order may last decades, and investors need to position their asset allocations for this important change.

US: The upcoming correction

Gerard Minack points out that US markets are starting to reassess downside dangers. He says that they are right to do so: valuation of risk assets started the year at precarious levels given the obvious economic and political uncertainties. Equity investors are now trimming positions, both long and short. Gerard sees a reasonable prospect of a full-blown correction. Rate markets are pricing a vanilla demand shock. What may instead unfold is an adverse supply-side shock that keeps inflation sticky and limits the scope for Fed easing. Equities are not behaving as most expected. The US is underperforming the rest of the world; the Mag 7 are underperforming the SPX493; growth is underperforming value; and the world’s most hated markets – China, the UK, and Europe – are leading returns (Exhibit 1). This smells of position squaring. It is not (yet) close to a correction: the S&P500 is just 3% from its all-time high.

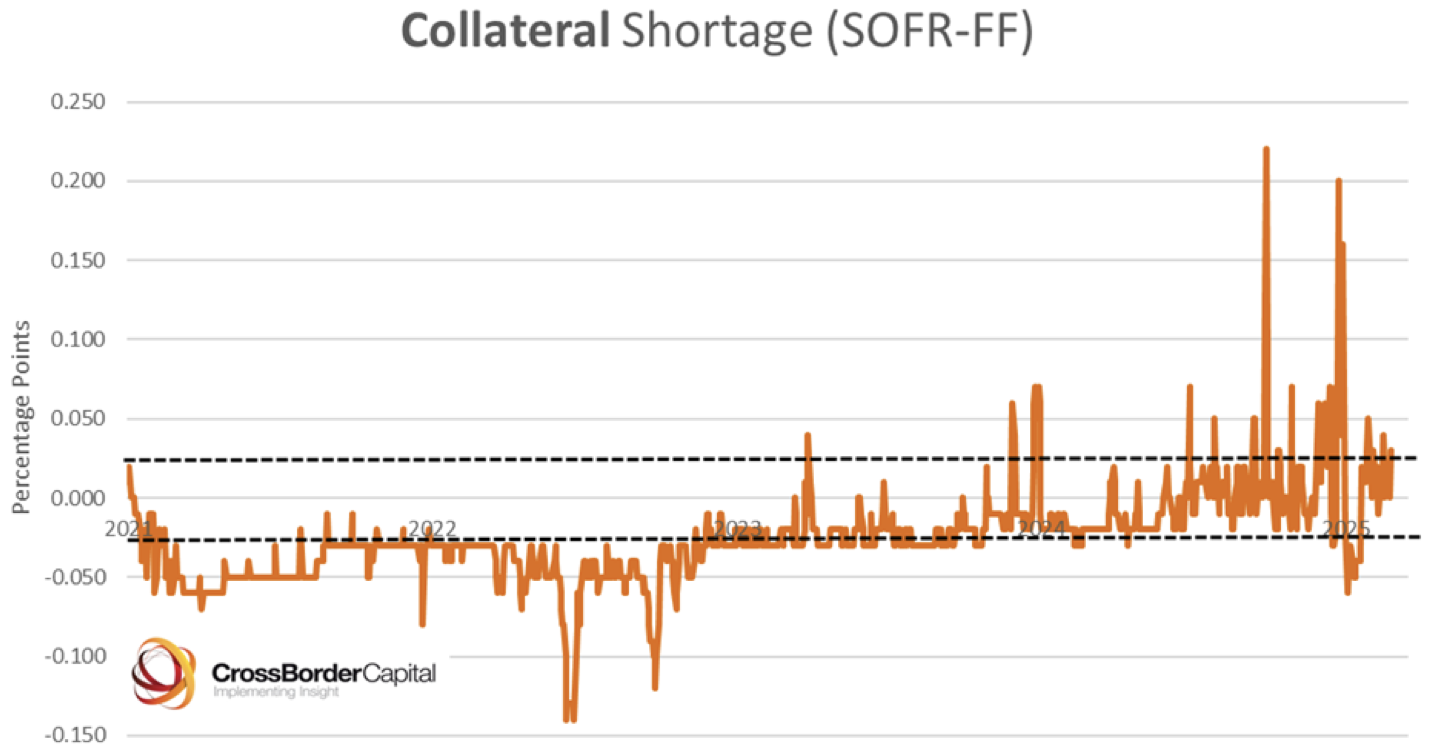

The return of American QE…please!

Michael Howell remarks that QE needs to come back in some form, potentially with a less provocative name. Not only are US money markets tightening and liquidity-sensitive assets, like Bitcoin, selling off, but the US economy is faltering as last year’s ‘secretive’ stimulus falls away. Admittedly, the Fed seems curiously reluctant to move, but unless they do markets will slam into a wall around mid-year when US banks’ reserves fall below the danger line; Michael estimates that the fast-approaching danger point will fall sometime around the second half of July 2025. As the time comes nearer, markets and investors will do well to realise that the capacity of capital matters far more than the cost of capital.

US: Understanding Trump

It is too often that people are shocked at the actions of Trump. Where investors, reporters and analysts consistently fail is in not making the effort to truly understand the objectives of the decision makers whose actions will affect the outcomes they are attempting to predict. When they don’t know or understand the values that inform the decision makers objectives, the only option is to fill the void in the algorithm with their own. Whether you like him or not, Trump is one of the most incredibly consistent leaders the world has known, unafraid to say what he thinks and does what he says he’ll do. Forget ideology; focus on Trump’s words and his desires to bolster capitalism, with his policies directly favouring him and his friends, including the heinous strategic crypto reserve. Far from the uncertainty lamented by all, if investors keep those very simple guiding principles in mind, this should be a moment of supreme clarity.

Resilience and the USA

Ed Yardeni continues to bet on the resilience of the American economy. Yes, the Atlanta Fed’s GDPNow model lowered its Q1 GDP forecast significantly on Friday. The volatile model swung in response to January’s surge in imported goods ahead of Trump’s tariffs. In addition, consumer spending was depressed by a colder-than-usual January, but consumer spending and the model are bound to rebound in February. Ed and his team explain why they believe pessimism about the economic outlook is unwarranted. As the uncertainty introduced by Trump 2.0’s flurry of aggressive actions lures the bears out of their caves, the team provides counterarguments to their most common growls.

Japan: Throwback to 1987?

Japanese demand pressure increased even as the economy shrank late last year, and supply side potential remains moribund. The wage/price spiral should therefore continue unless global events lead to a deeper slowdown in demand trends / sharp rise in the JPY. Over the long-term, Andrew Hunt continues to believe that Japan will inflate its way out from under the public debt burden and that the JPYUSD is headed for Y200, but currencies are a relative game and he fears that markets could soon see a “repatriation rally” in the JPY that sees it gap higher in a counter trend move as it did in Q4/1987 and Q4/1998. Any upward move in the JPY would scupper the BoJ’s tightening plans. Could JGBs be viewed as a safe haven for returning funds? In real terms, equity prices are elevated – will they be eroded by inflation as they were in the 1970s, or by asset price deflation? Andrew expects more of the former than the latter.

Emerging Markets

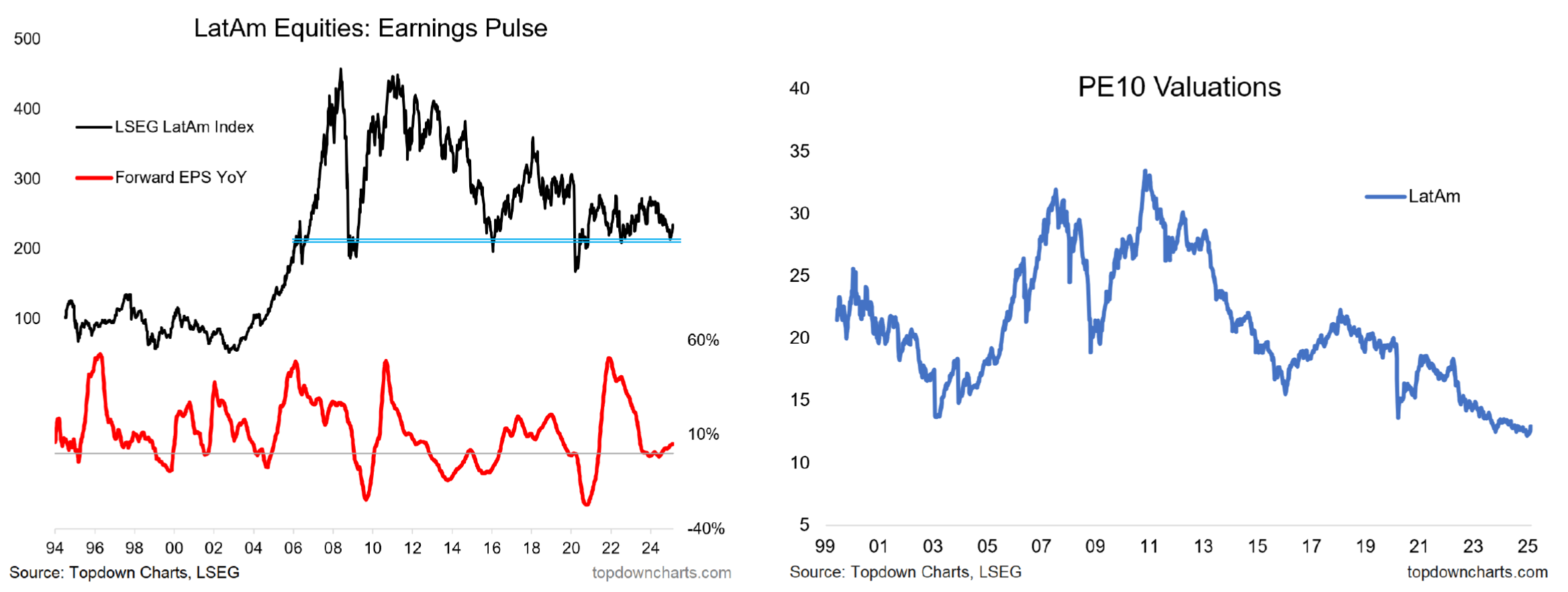

LatAm: Low… for now

Latin American equities (Brazil, Mexico, Colombia, Chile, Peru) have been ticking higher recently off a major long-term support line, with forward earnings also moving higher from previous stagnation (bullish cyclical sign). Valuations are cheap, with the average PE10 near record lows. Meanwhile, positioning is light as EM ETF investors are running near-record low allocations. FX also looks cheap and the equal-weighted LatAM index is rallying off a key support level, which helps the case for unhedged USD access to LatAm equities, which will be the case for most. Callum Thomas is bullish LatAm equities.

Algeria: Standing at the edge

Jonathan Anderson notes that Algeria took a long time to recover from the 2015 oil shock, finally managing to rebalance the economy when fuel prices soared in 2021-22 - but now with crude oil back at US$70/barrel Algeria is facing a gradual derating once again, and Jonathan would be very concerned if oil prices declined significantly further. There are few tradeable instruments in Algeria in the absence of a meaningful local equity market and internationally traded bonds. He says that the biggest question mark here is the Algerian dinar, which is exposed to renewed downside risks from oil prices, especially now that FX reserves are insufficient to provide support.

China: Bearish for commodities, supportive for equities

With the National People’s Congress having just opened, Qiushi – the Party’s ideological journal – has been the main voice in the domestic media setting the tone. Public intellectuals and policy advisors have been relatively quiet. However, William Hess notes that as per normal process, local governments held their own NPCs ahead of the central one, and aggregated policy targets sent some interesting signals. Although average local headline growth targets (and related fiscal targets) were dialled back, average growth targets for FAI and retail sales came in at 5.4% YoY and 5.7% YoY respectively. If these targets are achieved, it would be bullish for domestic asset prices. Given the low base and pending expansion of funding for durable goods swap programs, retail sales growth in this ballpark looks achievable. William still sees the overall backdrop as bearish commodities in the short-term, and more supportive of equities (after a potential post-NPC correction).

South Africa: Risks to GDP growth forecast are skewed to the downside

Real GDP expanded by 0.6% qoq in Q4 2024, in line with Tian Cater’s expectations, bringing full-year growth to a modest 0.6% YoY… Looking ahead, his outlook for 2025 remains cautiously optimistic. He forecasts real GDP growth at 1.9% YoY, revised down from 2.1% YoY. The lowering of the forecast however reflects weaker underlying momentum in the economy. Despite the anticipated improvement, risks remain skewed to the downside. Tian’s projections do not yet incorporate the potential loss of Agoa in April, which, if realised, could shave 0.2pp off our 2025 growth estimate. Additionally, global risks - including increasing trade fragmentation (cough, Trump) and weaker external demand - pose further threats, potentially reversing the anticipated recovery in exports.

Turkey: Paving the way for cuts

Report by

Burumcekci Research & Consulting

In February, the CPI increased by 2.27%, falling short of the median expectation of a 3.0% increase… Excluding seasonal products, the CPI recorded a monthly increase of 3.0%, marking a decline compared to the previous month. The annual CPI dropped from 42.12% in the previous month to 39.05%. The year-on-year decrease in inflation was influenced by both food and non-food prices. According to Haluk Burumcekci, if the current moderate trend in exchange rates continues and there is no additional shock in wages, managed prices, and commodity prices, inflation could finish the year at around 29%. In the Central Bank’s Inflation Report, the reversal of the managed-guided price increases that led to a forecast revision and the fact that this resulted in a February performance below expectations appears to have paved the way for continuing with a 250 basis point cut in interest rates at the March meeting.

Commodities

Tariffs shake the leaves of Canadian forest producers

Tariff Tuesday has arrived with Canadian forest products firms facing extinction-level impacts. Tariffs will be pushed through to US buyers in some cases, but chaos will ensue regardless. Additionally, all Canadian timber/fibre-based products could be subject to incremental tariffs (Section 232 investigation). China has announced a ban on US log imports. It was a busy week in North American lumber markets as buyers, with generally lean inventories, weighed the threat of tariffs against tepid demand. Prices for S-P-F 2x4s finished the week up an impressive $30 to $518 (first time above $500 since the autumn of 2022). Canadian producers were hit with a double-whammy this week—President Trump’s 25% tariff came into effect on Tuesday and, on Monday, preliminary AR6 anti-dumping duty rates were released. Passing on both tariffs and higher duties come August will be a challenge.

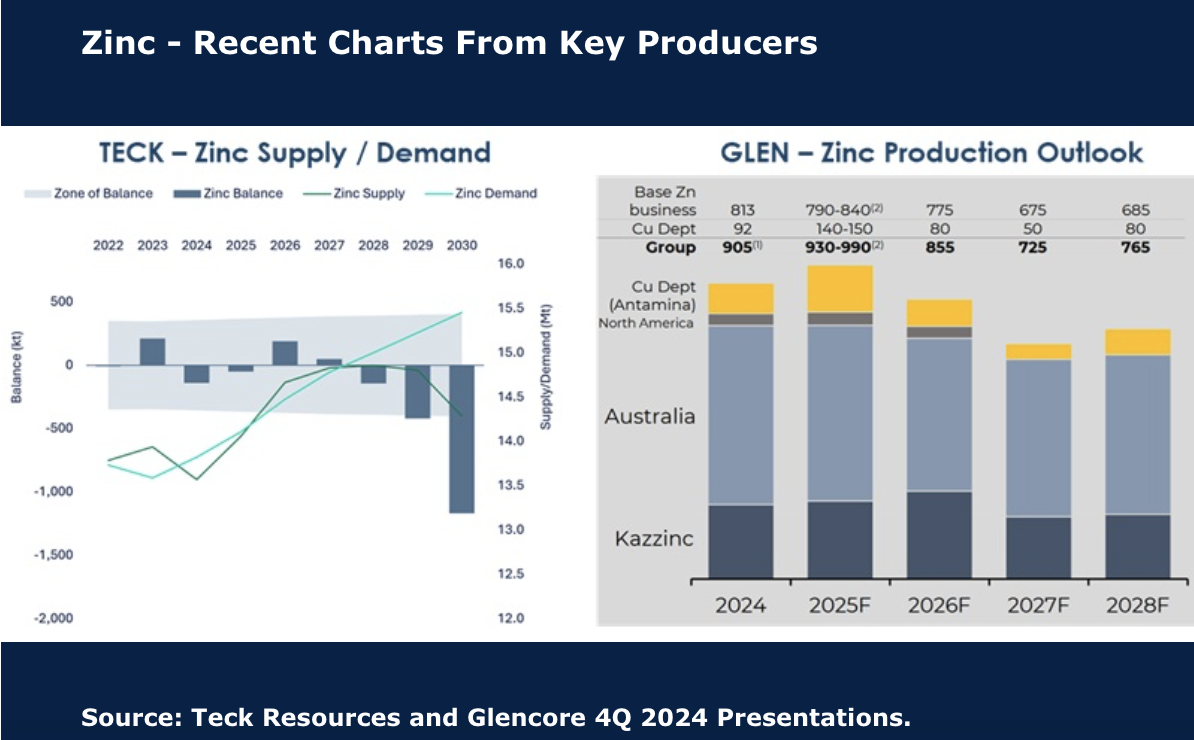

Zinc: Lagging in 2025

As Zinc production falls 2.8% YoY, the modest deficit appears to be accelerating towards the end of the year, as indicated by two of the largest players in the industry (see chart). Ailing production is in part due to the maturing of existing operations, although headwinds are expected to be offset in part by full year of production restarts, with Ozernoye the key one to watch. Whilst the zinc price is lacklustre, the fundamentals look ok. Inventories are moving in the right direction and are already less than 1 week of global supply, which to the team appears tight. Another positive is also expected to come from lower benchmark Treatment Charges (TCs) given a shortage of concentrate in the market. 2025 and 2026 will really be about the tussle of additional supply offset by closing supply.

The silver crisis and the true value of gold

In his latest video, Jeffrey Christian looks at some myths that continue to gain traction in gold and silver market commentary. He looks at the US dollar’s decline and provides hard data showing that global investors are actually increasing their holdings of US Treasuries. Contrary to popular narratives, the dollar is not collapsing; it is up significantly from previous lows. Jeff also looks at the misunderstood concept of fiat currency. There is a belief that gold is somehow exempt from the forces that drive currencies, but gold’s price, just like the dollar, is determined by market forces. The discussion moves to the so-called "silver squeeze" that never materialised, including a look at futures contracts, Comex inventory levels, and why expectations of a silver shortage continue to be misguided. The video ends with a market update, discussing recent movements in gold, silver, platinum, and palladium, and the broader economic and geopolitical factors influencing them.

Click here to watch.